Tithe

A tithe (/ˈtaɪð/; from Old English: teogoþa "tenth") is a one-tenth part of something, paid as a contribution to a religious organization or compulsory tax to government.[1] Today, tithes are normally voluntary and paid in cash, cheques, or stocks, whereas historically tithes were required and paid in kind, such as agricultural products. Several European countries operate a formal process linked to the tax system allowing some churches to assess tithes.

Traditional Jewish law and practice has included various forms of tithing since ancient times. Orthodox Jews commonly practice ma'aser kesafim (tithing 10% of their income to charity). In modern Israel, Jews continue to follow the laws of agricultural tithing, e.g., ma'aser rishon, terumat ma'aser, and ma'aser sheni. In Christianity, some interpretations of Biblical teachings conclude that although tithing was practiced extensively in the Old Testament, it was never practiced or taught within the first-century Church. Instead, the New Testament scriptures are seen as teaching the concept of "freewill offerings" as a means of supporting the church: 1 Corinthians 16:2, 2 Corinthians 9:7. Also, some of the earliest groups sold everything they had and held the proceeds in common to be used for the furtherance of the Gospel: Acts 2:44-47, Acts 4:34-35. Further, Acts 5:1-20 contains the account of a man and wife (Ananias and Sapphira) who were living in one of these groups. They sold a piece of property and donated only part of the selling price to the church but claimed to have given the whole amount and immediately fell down and died when confronted by the apostle Peter over their dishonesty.

Tithes were mentioned at the Council of Tours in 567 and the Synod of Mâcon in 585.

Ancient Near East

None of the extant laws of the Ancient Near East deal with tithing, although other secondary documents show that it was a widespread practice in the Ancient Near East.[2] William W. Hallo (1996[3]) recognises comparisons for Israel with its ancient Near Eastern environment, however, as regards tithes, comparisons with other ancient Near Eastern evidence is ambiguous,[4] and Ancient Near Eastern literature provides scant evidence for the practice of tithing and the collection of tithes.[5]

The esretu — "ešretū" the Ugarit and Babylonian one-tenth tax

Listed below are some specific instances of the Mesopotamian tithe, taken from The Assyrian Dictionary of the Oriental Institute of the University of Chicago, Vol. 4 "E" pag.369,:[6]

- [Referring to a ten per cent tax levied on garments by the local ruler:] "the palace has taken eight garments as your tithe (on 85 garments)"

- "...eleven garments as tithe (on 112 garments)"

- "...(the sun-god) Shamash demands the tithe..."

- "four minas of silver, the tithe of [the gods] Bel, Nabu, and Nergal..."

- "...he has paid, in addition to the tithe for Ninurta, the tax of the gardiner"

- "...the tithe of the chief accountant, he has delivered it to [the sun-god] Shamash"

- "...why do you not pay the tithe to the Lady-of-Uruk?"

- "...(a man) owes barley and dates as balance of the tithe of the **years three and four"

- "...the tithe of the king on barley of the town..."

- "...with regard to the elders of the city whom (the king) has **summoned to (pay) tithe..."

- "...the collector of the tithe of the country Sumundar..."

- "...(the official Ebabbar in Sippar) who is in charge of the tithe..."

Hebrew Bible

Hebrew is a Semitic language, related to Akkadian, the lingua franca of that time.[7]

Patriarchs

In Genesis 14:18-20, Abraham, after rescuing Lot, met with Melchizedek. After Melchizedek's blessing, Abraham gave him a tenth of everything he has obtained from battle:

"Then Melchizedek king of Salem brought out bread and wine. He was priest of God Most High, and he blessed Abram, saying, “Blessed be Abram by God Most High, Creator of heaven and earth. And praise be to God Most High, who delivered your enemies into your hand.” Then Abram gave him a tenth of everything.”— Genesis 14:18-20

In Genesis 28:12-22, Jacob, after his visionary dream of Jacob's Ladder and receiving a blessing from God, promises God a tenth:

"Then Jacob awoke from his sleep and said, “Surely the Lord is in this place, and I did not know it.” And he was afraid and said, “How awesome is this place! This is none other than the house of God, and this is the gate of heaven.”So early in the morning Jacob took the stone that he had put under his head and set it up for a pillar and poured oil on the top of it. He called the name of that place Bethel, but the name of the city was Luz at the first. Then Jacob made a vow, saying, “If God will be with me and will keep me in this way that I go, and will give me bread to eat and clothing to wear, so that I come again to my father's house in peace, then the Lord shall be my God, and this stone, which I have set up for a pillar, shall be God's house. And of all that you give me I will give a full tenth to you.”

— Genesis 28:12-22

Mosaic law

The tithe is specifically mentioned in the Books of Leviticus, Numbers and Deuteronomy. The tithe system was organized in a three-year cycle, corresponding to the Shemittah-cycle. These tithes were in reality more like taxes for the people of Israel and were mandatory, not optional giving. This tithe was distributed locally "within thy gates" (Deuteronomy 14:28) to support the Levites and assist the poor.

Every year, Bikkurim, Terumah, Ma'aser Rishon and Terumat Ma'aser were separated from the grain, wine and oil (Deuteronomy 14:22). (As regards other fruit and produce, the Biblical requirement to tithe is a source of debate.) The first tithe is giving of one tenth of agricultural produce (after the giving of the standard terumah) to the Levite (or Aaronic priests). Historically, during the First Temple period, the first tithe was given to the Levites. Approximately at the beginning of the Second Temple construction, Ezra and his Beth din implemented its giving to the kohanim.[8][9]

Unlike other offerings which were restricted to consumption within the tabernacle, the second tithe could be consumed anywhere . On years one, two, four and five of the Shemittah-cycle, God commanded the Children of Israel to take a second tithe that was to be brought to the place of the Temple (Deuteronomy 14:23). The owner of the produce was to separate and bring 1/10 of his finished produce to the Old City of Jerusalem after separating Terumah and the first tithe, but if the family lived too far from Jerusalem, the tithe could be redeemed upon coins (Deuteronomy 14:24-25). Then, the Bible required the owner of the redeemed coins to spend the tithe "to buy whatever you like: cattle, sheep, wine or other fermented drink, or anything you wish" (Deuteronomy 14:26). Implicit in the commandment was an obligation to spend the coins on items meant for human consumption.

In years three and six of the Shemittah-cycle the Israelites set aside the (second) tithe instead as the poor tithe, and it was given to the strangers, orphans, and widows.

The Levites, also known as the Tribe of Levi, were descendants of Levi. They were assistants to the Aaronic priests (who were the children of Aaron and, therefore, a subset of the Tribe of Levi) and did not own or inherit a territorial patrimony (Numbers 18:21-28). Their function in society was that of temple functionaries, teachers and trusted civil servants who supervised the weights and scales and witnessed agreements. The goods donated from the other Israeli tribes were their source of sustenance. They received from "all Israel" a tithe of food or livestock for support, and in turn would set aside a tenth portion of that tithe (known as the Terumat hamaaser) for the Aaronic priests.

An additional tithe mentioned in the Book of Leviticus (27:32-33) is the cattle tithe, which is to be sacrificed as a korban at the Temple in Jerusalem.

United Kingdom of Israel

LMLK seals may represent the oldest archaeological evidence of tithing. About 10 percent of the storage jars manufactured during Hezekiah's reign (circa 700 BC) were stamped (Grena, 2004, pp. 376–8). See 2 Chronicles 29–31 for a record of this early worship reformation.

The Book of Nehemiah also talks about the collection of tithes to Leviim and distribution of Terumah to the priests: Nehemiah 13:5. People were actually appointed to collect mandatory tithes and place them in specially designated chambers which eventually came to be known as storehouses: Nehemiah 12:44.

Minor Prophets

The Book of Malachi has one of the most quoted Biblical verses about tithing:

"Will man rob God? Yet you are robbing me. But you say, ‘How have we robbed you?’ In your tithes and contributions. You are cursed with a curse, for you are robbing me, the whole nation of you. Bring the full tithe into the storehouse, that there may be food in my house. And thereby put me to the test, says the Lord of hosts, if I will not open the windows of heaven for you and pour down for you a blessing until there is no more need. I will rebuke the devourer for you, so that it will not destroy the fruits of your soil, and your vine in the field shall not fail to bear, says the Lord of hosts. Then all nations will call you blessed, for you will be a land of delight, says the Lord of hosts."

Deuterocanonical

The deuterocanonical Book of Tobit provides an example of all three classes of tithes practiced during the Babylonian captivity:

"I would often go by myself to Jerusalem on religious holidays, as the Law commanded for every Israelite for all time. I would hurry off to Jerusalem and take with me the early produce of my crops, a tenth of my flocks, and the first portion of the wool cut from my sheep. I would present these things at the altar to the priests, the descendants of Aaron. I would give the first tenth of my grain, wine, olive oil, pomegranates, figs, and other fruit to the Levites who served in Jerusalem. For six out of seven years, I also brought the cash equivalent of the second tenth of these crops to Jerusalem where I would spend it every year. I gave this to orphans and widows, and to Gentiles who had joined Israel. In the third year, when I brought and gave it to them, we would eat together according to the instruction recorded in Moses’ Law, as Deborah my grandmother had taught me..."

Judaism

Orthodox Jews continue to follow the laws of Terumah and Ma'aser as well as the custom of tithing 10% of one's earnings to charity (ma'aser kesafim). Due to doubts concerning the status of persons claiming to be Kohanim or Levi'im arising after severe Roman/Christian persecutions and exile, the Hebrew Bible tithe of 10% for the Levites, and "tithe of the tithe" (Numbers 18:26) of 10% of 10% (1%) for the priests are dealt with in accordance with Jewish Law. The Mishnah and Talmud contain analysis of the first tithe, second tithe and poor tithe.[10]

Animals are not tithed in the present era when the Temple is not standing.[11]

Christianity

Many Christians support their churches and pastors with monetary contributions of one sort or another. Frequently these monetary contributions are called tithes - whether or not they actually represent ten percent of anything. Some claim that as tithing was an ingrained Jewish custom by the time of Jesus, but no specific command to tithe appears in the New Testament.[12]

For Catholics, the payment of tithes was adopted from the Old Law, and early writers[13] speak of it as a divine ordinance and as an obligation of conscience,[14] rather than any direct command by Jesus Christ.

Some Protestants cite Jesus' words in Matthew 23:23 in support of tithing while others see it as a denunciation of false piety.

Away with you, you pettifogging Pharisee lawyers! You give to God a tenth of herbs, like mint, dill, and cumin, but the important duties of the Law — judgement, mercy, honesty — you have neglected. Yet these you ought to have performed, without neglecting the others.

and its parallel Luke 11:42

Woe to you, Pharisees! You tithe mint and rue and every edible herb but disregard justice and the love of God. These were rather the things one should practice, without neglecting the others.

Another mention of tithing in the New Testament appears in Hebrews 7:1–10. This refers back to the tithe Abram paid to Melchizedek - whether as generosity or as a letter-of-the-law tenth is not mentioned.

New Testament discussion promotes giving and does not mention tithing. 2 Corinthians 9:7 talks about giving cheerfully, 2 Corinthians 8:12 encourages giving what you can afford, 1 Corinthians 16:1–2 discusses giving weekly (although this is a saved amount for Jerusalem), 1 Timothy 5:17–18 exhorts supporting the financial needs of Christian workers, Acts 11:29 promotes feeding the hungry wherever they may be and James 1:27 states that pure religion is to help widows and orphans.

Church of the Nazarene

The Church of the Nazarene teaches to pay a tithe, although not necessarily the one-tenth under Old Testament law. People pay according to their ability.[15]

Orthodox Christianity

Tithing in medieval Eastern Christianity did not spread so widely as in the West. A Constitution of the Emperors Leo I (reigned 457-474) and Anthemius (reigned 467-472) apparently expected believers to make voluntary payments and forbade compulsion.[16]

The Church of Jesus Christ of Latter-day Saints

The Church of Jesus Christ of Latter-day Saints (LDS Church) bases its tithing on the following additional scriptures:[17]

And this shall be the beginning of the tithing of my people. And after that, those who have thus been tithed shall pay one-tenth of all their interest annually; and this shall be a standing law unto them forever, for my holy priesthood, saith the Lord.

And it was this same Melchizedek to whom Abraham paid tithes; yea, even our father Abraham paid tithes of one-tenth part of all he possessed.

Tithing is currently defined by the church as payment to the church of one-tenth of one's annual income. Many LDS leaders have made statements in support of tithing.[18] Every Latter-day Saint receives an opportunity once a year to meet with their bishop about their tithing settlement. The payment of tithes is mandatory for members to receive the priesthood or obtain admission to temples.

None of the funds collected from tithing is paid to church officials. The Church of Jesus Christ of Latter-day Saints is a Lay Ministry.[19] The money that is given is used to build and maintain church buildings as well as to further the work of the church.[20] Brigham Young University, a practically all-LDS school, also receives "a significant portion" of its maintenance and operational costs from LDS tithes.

Islam

Zakāt (Arabic: زكاة [zækæːh]) or "alms giving", one of the Five Pillars of Islam, is the giving of a small percentage of one's assets to charity. It serves principally as the welfare contribution to poor and deprived Muslims, although others may have a rightful share. It is the duty of an Islamic state not just to collect zakat but to distribute it fairly as well.

Zakat is payable on three kinds of assets: wealth, production, and animals. The more well-known zakat on wealth is 2.5% of accumulated wealth, beyond one's personal needs. Production (agricultural, industrial, renting, etc.), is subject to a 10% or 5% zakat (also known as Ushur (عُشر), or "one-tenth"), using the rule that if both labor and capital are involved, 5% rate is applied, if only one of the two are used for production, then the rate is 10%. For any earnings, that require neither labor nor capital, like finding underground treasure, the rate is 20%. The rules for zakat on animal holdings are specified by the type of animal group and tend to be fairly detailed.[21]

Muslims fulfill this religious obligation by giving a fixed percentage of their surplus wealth. Zakat has been paired with such a high sense of righteousness that it is often placed on the same level of importance as performing the five-daily repetitive ritualised prayer (salat).[22] Muslims see this process also as a way of purifying themselves from their greed and selfishness and also safeguarding future business.[22] In addition, Zakat purifies the person who receives it because it saves him from the humiliation of begging and prevents him from envying the rich.[23] Because it holds such a high level of importance the "punishment" for not paying when able is very severe. In the 2nd edition of the Encyclopaedia of Islam it states, "...the prayers of those who do not pay zakat will not be accepted".[22] This is because without Zakat a tremendous hardship is placed on the poor which otherwise would not be there. Besides the fear of their prayers not getting heard, those who are able should be practicing this third pillar of Islam because the Quran states that this is what believers should do.[24]

Non-Muslims (able-bodied adult males of military age) living in an Islamic state are required to pay Jizya, this exempts them from military service and they do not pay Zakat.

Sikhism

Daswandh (Punjabi: ਦਸਵੰਧ), sometimes spelled Dasvandh, is the one tenth part (or 10%) of one's income that should be donated in the name of the God, according to Sikh principles.[25][26]

Church collection of religious offerings and taxes

England and Wales

The right to receive tithes was granted to the English churches by King Ethelwulf in 855. The Saladin tithe was a royal tax, but assessed using ecclesiastical boundaries, in 1188. The legal validity of the tithe system was affirmed under the Statute of Westminster of 1285. The Dissolution of the Monasteries led to the transfer of many rights to tithe to secular landowners and the Crown – and tithes could be extinguished until 1577 under an Act of the 37th year of Henry VIII's reign.[27] Adam Smith criticized the system in The Wealth of Nations (1776), arguing that a fixed rent would encourage peasants to farm more efficiently.

See below for a fuller description and history, until the reforms of the 19th century, written by Sir William Blackstone and edited by other learned lawyers of the period.

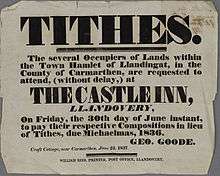

The system gradually ended with the Tithe Commutation Act 1836, whose long-lasting Tithe Commission replaced them with a commutation payment, land award and/or rentcharges to those paying the commutation payment and took the opportunity to map out (apportion) residual chancel liability where the rectory had been appropriated during the medieval period by a religious house or college. Its records give a snapshot of land ownership in most parishes, the Tithe Files, are a socio-economic history resource. The rolled-up payment of several years' tithe would be divided between the tithe-owners as at the date of their extinction.[28]

This commutation reduced problems to the ultimate payers by effectively folding tithes in with rents however, it could cause transitional money supply problems by raising the transaction demand for money. Later the decline of large landowners led tenants to become freeholders and again have to pay directly; this also led to renewed objections of principle by non-Anglicans. It also kept intact a system of chancel repair liability affecting the minority of parishes where the rectory had been lay-appropriated. The precise land affected in such places hinged on the content of documents such as the content of deeds of merger and apportionment maps.[28]

Tithe redemption

Rentcharges in lieu of abolished tithe paid by landowners were converted by a public outlay of money under the Tithe Act 1936 into annuities paid to the state through the Tithe Redemption Commission. Such payments were transferred in 1960 to the Board of Inland Revenue, and those remaining were terminated by the Finance Act 1977.

The Tithe Act 1951 established the compulsory redemption of English tithes by landowners where the annual amounts payable were less than £1 so abolishing the bureaucracy and costs of collecting small sums of money.

Receipted 1955 redemption notice for property in East Dundry, just south of Bristol

Receipted 1955 redemption notice for property in East Dundry, just south of Bristol Registered letter cover

Registered letter cover Relevant tithe map

Relevant tithe map

France

In France, the tithes—called "la dîme"—were a land tax. Originally a voluntary tax, the "dîme" became mandatory in 1585. In principle, unlike the taille, the "dîme" was levied on both noble and non-noble lands. The dîme was divided into a number of types, including the "grosses dîmes" (grains, wine, hay), "menues" or "vertes dîmes" (vegetables, poultry), "dîmes de charnage" (veal, lamb, pork). Although the term "dîme" comes from the Latin decima [pars] ("one tenth", with the same origin as that of the U.S. coin, the dime), the "dîme" rarely reached this percentage and (on the whole) it was closer to 1/13th of the agricultural production.

The "dîme" was originally meant to support the local parish, but by the 16th century many "dîmes" went directly to distant abbeys, monasteries, and bishops, leaving the local parish impoverished, and this contributed to general resentment. In the Middle Ages, some monasteries also offered the "dîme" in homage to local lords in exchange for their protection (see Feudalism) (these are called "dîmes inféodées"), but this practice was forbidden by the Lateran Council of 1179.

All religious taxes were constitutionally abolished in 1790, in the wake of the French revolution.

Greece

There has never been a separate church tax or mandatory tithe on Greek citizens. The state pays the salaries of the clergy of the established Church of Greece, in return for use of real estate, mainly forestry, owned by the church. The remainder of church income comes from voluntary, tax-deductible donations from the faithful. These are handled by each diocese independently.

Ireland

From the English Reformation in the 16th century, most Irish people chose to remain Roman Catholic and had by now to pay tithes valued at about 10% of an area's agricultural produce, to maintain and fund the established state church, the Anglican Church of Ireland, to which only a small minority of the population converted. Irish Presbyterians and other minorities like the Quakers and Jews were in the same situation.

The collection of tithes was violently resisted in the period 1831-36, known as the Tithe War. Thereafter, tithes were reduced and added to rents with the passing of the Tithe Commutation Act in 1836. With the disestablishment of the Church of Ireland by the Irish Church Act 1869, tithes were abolished.

United States

While the federal government has never collected a church tax or mandatory tithe on its citizens, states collected a tithe into the early 19th century. Today, such a tax is prohibited by the First Amendment (specifically the Establishment Clause) to the US Constitution. The United States and its governmental subdivisions also exempt most churches from payment of income tax (under Section 501(c)(3) of the Internal Revenue Code and similar state statutes, which also allows donors to claim the donations as an income tax itemized deduction). Also, churches may be permitted exemption from other state and local taxes such as sales and property taxes, either in whole or in part. Clergy, such as ministers and members of religious orders (who have taken a vow of poverty) are exempt from federal income tax on income from ministerial services. Income from non-ministerial services are taxable and churches are required to withhold Federal and state income tax from this non-exempt income. They are also required to withhold employee's share of Social Security and Medicare taxes under FICA, and pay the employer's share for the non-exempt income.[29]

Spain and Latin America

Both the tithe (diezmo), a levy of 10% on all agricultural production, and "first fruits" (primicias), an additional harvest levy, were collected in Spain throughout the medieval and early modern periods for the support of local Catholic parishes.

The tithe crossed the Atlantic with the Spanish Empire; however, the Indians who made up the vast majority of the population in colonial Spanish America were exempted from paying tithes on native crops such as corn and potatoes that they raised for their own subsistence. After some debate, Indians in colonial Spanish America were forced to pay tithes on their production of European agricultural products, including wheat, silk, cows, pigs, and sheep.

The tithe was abolished in several Latin American countries, including Mexico, soon after independence from Spain (which started in 1810). The tithe was abolished in Spain itself in 1841, and in Argentina in 1826.

Governmental collection of religious offerings and taxes

Austria

In Austria a colloquially called church tax (Kirchensteuer, officially called Kirchenbeitrag, i.e. church contribution) has to be paid by members of the Catholic and Protestant Church. It is levied by the churches themselves and not by the government. The obligation to pay church tax can just be evaded by an official declaration to cease church membership. The tax is calculated on the basis of personal income. It amounts to about 1.1% (Catholic church) and 1.5% (Protestant church).

Denmark

All members of the Church of Denmark pay a church tax, which varies between municipalities.[30] The tax is generally around 1% of the taxable income.

Finland

Members of state churches pay a church tax of between 1% and 2% of income, depending on the municipality. In addition, 2.55% of corporate taxes are distributed to the state churches. Church taxes are integrated into the common national taxation system.[31]

Germany

Germany levies a church tax, on all persons declaring themselves to be Christians, of roughly 8–9% of their income tax, which is effectively (very much depending on the social and financial situation) typically between 0.2% and 1.5% of the total income. The proceeds are shared amongst Catholic, Lutheran, and other Protestant Churches.[32]

The church tax (Kirchensteuer) actually traces its roots back as far as the Reichsdeputationshauptschluss of 1803. It was reaffirmed in the Concordat of 1933 between Nazi Germany and the Catholic Church. Today its legal basis is article 140 of the Grundgesetz (the German "constitution") in connection with article 137 of the Weimar constitution. These laws originally merely allowed the churches themselves to tax their members, but in Nazi Germany, collection of church taxes was transferred to the German government. As a result, both the German government and the employer are notified of the religious affiliation of every taxpayer. This system is still in effect today. Mandatory disclosure of religious affiliation to government agencies or employers constituted a violation of the original European data protection directives but is now permitted after the German government obtained an exemption.[32]

Church tax (Kirchensteuer) is compulsory in Germany for those confessing members of a particular religious group. It is deducted at the PAYE level. The duty to pay this tax theoretically starts on the day one is christened. Anyone who wants to stop paying it has to declare in writing, at their local court of law (Amtsgericht) or registry office, that they are leaving the Church. They are then crossed off the Church registers and can no longer receive the sacraments, confession and certain services; Roman Catholic church may deny such as person a burial plot.[32] In addition to the government, the taxpayer also must notify his employer of his religious affiliation (or lack thereof) in order to ensure proper tax withholding.[33]

This opt-out is also used by members of "free churches" (e.g. Baptists) (non-affiliated to the scheme) to stop paying the church tax, from which the free churches do not benefit, in order to support their own church directly.

Italy

Originally the Italian government of Benito Mussolini, under the Lateran treaties of 1929 with the Holy See, paid a monthly salary to Catholic clergymen. This salary was called the congrua. The eight per thousand law was created as a result of an agreement, in 1984, between the Italian Republic and the Holy See.

Under this law Italian taxpayers are able to vote how to partition the 0.8% ('eight per thousand') of the total income tax IRPEF levied by Italy among some specific religious confessions or, alternatively, to a social assistance program run by the Italian State. This declaration is made on the IRPEF form. This vote is not compulsory; the whole amount levied by the IRPEF tax is distributed in proportion to explicit declarations.

The last official statement of Italian Ministry of Finance made in respect of the year 2000 singles out seven beneficiaries: the Italian State, the Catholic Church, the Waldenses, the Jewish Communities, the Lutherans, the Seventh-day Adventist Church and the Assemblies of God in Italy.

The tax was divided up as follows:

- 87.17% Catholic Church

- 10.35% Italian State

- 1.21% Waldenses

- 0.46% Jewish Communities

- 0.32% Lutherans

- 0.28% Adventists of the Seventh Day

- 0.21% Assemblies of God in Italy

In 2000, the Catholic Church raised almost a billion euros, while the Italian State received about €100 million euros.

Scotland

In Scotland teinds were the tenths of certain produce of the land appropriated to the maintenance of the Church and clergy. At the Reformation most of the Church property was acquired by the Crown, nobles and landowners. In 1567 the Privy Council of Scotland provided that a third of the revenues of lands should be applied to paying the clergy of the reformed Church of Scotland. In 1925 the system was recast by statute[34] and provision was made for the standardisation of stipends at a fixed value in money. The Court of Session acted as the Teind Court. Teinds were finally abolished by section 56 of the Abolition of Feudal Tenure etc. (Scotland) Act 2000.

Sweden

Until the year 2000, Sweden had a mandatory church tax, to be paid if one did belong to the Church of Sweden, which had been funneling about $500 million annually to the church. Because of change in legislation, the tax was withdrawn in the year 2000. However, the Swedish government has agreed to continue collecting from individual taxpayers the annual payment that has always gone to the church. But now the tax will be an optional checkoff box on the tax return. The government will allocate the money collected to Catholic, Muslim, Jewish and other faiths as well as the Lutherans, with each taxpayer directing where his or her taxes should go.

Switzerland

There is no official state church in Switzerland; however, all the 26 cantons (states) financially support at least one of the three traditional denominations--Roman Catholic, Old Catholic, or Protestant—with funds collected through taxation. Each canton has its own regulations regarding the relationship between church and state. In some cantons, the church tax (up to 2.3%) is voluntary but in others an individual who chooses not to contribute to church tax may formally have to leave the church. In some cantons private companies are unable to avoid payment of the church tax.

Tithes and tithe law in England before reform

Excerpts from Sir William Blackstone, Commentaries on the Laws of England:

Definition and classification and those liable to pay tithes

. . . tithes; which are defined to be the tenth part of the increase, yearly arising and renewing from the profits of lands, the stock upon lands, and the personal industry of the inhabitants:

- the first species being usually called predial,[35] as of corn, grass, hops, and wood;

- the second mixed, as of wool, milk, pigs, &c, consisting of natural products, but nurtured and preserved in part by the care of man; and of these the tenth must be paid in gross:

- the third personal, as of manual occupations, trades, fisheries, and the like ; and of these only the tenth part of the clear gains and profits is due.

...

in general, tithes are to be paid for every thing that yields an annual increase, as corn, hay, fruit, cattle, poultry, and the like; but not for any thing that is of the substance of the earth, or is not of annual increase, as stone, lime, chalk, and the like; nor for creatures that are of a wild nature, or ferae naturae, as deer, hawks, &c, whose increase, so as to profit the owner, is not annual, but casual.[36]:24

History

We cannot precisely ascertain the time when tithes were first introduced into this country. Possibly they were contemporary with the planting of Christianity among the Saxons, by Augustin the monk, about the end of the fifth century. But the first mention of them, which I have met with in any written English law, is in a constitutional decree, made in a synod held A.D. 786, wherein the payment of tithes in general is strongly enjoined. This canon, or decree, which at first bound not the laity, was effectually confirmed by two kingdoms of the heptarchy, in their parliamentary conventions of estates, respectively consisting of the kings of Mercia and Northumberland, the bishops, dukes, senators, and people. Which was a few years later than the time that Charlemagne established the payment of them in France, and made that famous division of them into four parts ; one to maintain the edifice of the church, the second to support the poor, the third the bishop, and the fourth the parochial clergy.[36]:25

Beneficiaries

And upon their first introduction (as hath formerly been observed), though every man was obliged to pay tithes in general, yet he might give them to what priests he pleased; which were called arbitrary consecrations of tithes: or he might pay them into the hands of the bishop, who distributed among his diocesan clergy the revenues of the church, which were then in common. But, when dioceses were divided into parishes, the tithes of each parish were allotted to its own particular minister; first by common consent, or the appointment of lords of manors, and afterwards by the written law of the land.[36]:26 ... it is now universally held, that tithes are due, of common right, to the parson of the parish, unless there be a special exemption. This parson of the parish, we have formerly seen, may be either the actual incumbent, or else the appropriator of the benefice: appropriations being a method of endowing monasteries, which seems to have been devised by the regular clergy, by way of substitution to arbitrary consecrations of tithes.[36]:28

Exemptions

We observed that tithes are due to the parson of common right, unless by special exemption: let us therefore see, thirdly, who may be exempted from the payment of tithes ... either in part or totally, first, by a real composition; or secondly, by custom or prescription.First, a real composition is when an agreement is made between the owner of the lands, and the parson or vicar, with the consent of the ordinary and the patron, that such lands shall for the future be discharged from payment of tithes, by reason of some land or other real recompence given to the parson, in lieu and satisfaction thereof. ...

Secondly, a discharge by custom or prescription, is where time out of mind such persons or such lands have been, either partially or totally, discharged from the payment of tithes. And this immemorial usage is binding upon all parties, as it is in its nature an evidence of universal consent and acquiescence; and with reason supposes a real composition to have been formerly made. This custom or prescription is either de modo decimandi, or de non decimando.

A modus decimandi, commonly called by the simple name of a modus only, is where there is by custom a particular manner of tithing allowed, different from the general law of taking tithes in kind, which are the actual tenth part of the annual increase. This is sometimes a pecuniary compensation, as twopence an acre for the tithe of land : sometimes it is a compensation in work and labour, as that the parson shall have only the twelfth cock of hay, and not the tenth, in consideration of the owner's making it for him: sometimes, in lieu of a large quantity of crude or imperfect tithe, the parson shall have a less quantity, when arrived to greater maturity, as a couple of fowls in lieu of tithe eggs ; and the like. Any means, in short, whereby the general law of tithing is altered, and a new method of taking them is introduced, is called a modus decimandi, or special manner of tithing.[36]:28–29 ...

A prescription de non decimando is a claim to be entirely discharged of tithes, and to pay no compensation in lieu of them. Thus the king by his prerogative is discharged from all tithes. So a vicar shall pay no tithes to the rector, nor the rector to the vicar, for ecclesia decimas non folvit ecclesiae. But these personal to both the king and the clergy ; for their tenant or lessee shall pay tithes of the same land, though in their own occupation it is not tithable. And, generally speaking, it is an established rule, that in lay hands, modus de non decimando non valet. But spiritual persons or corporations, as monasteries, abbots, bishops, and the like, were always capable of having their lands totally discharged of tithes, by various ways: as

- By real composition :

- By the pope's bull of exemption :

- By unity of possession ; as when the rectory of a parish, and lands in the same parish, both belonged to a religious house, those lands were discharged of tithes by this unity of possession :

- By prescription ; having never been liable to tithes, by being always in spiritual hands :

- By virtue of their order; as the knights templars, cistercians, and others, whose lands were privileged by the pope with a discharge of tithes. Though, upon the dissolution of abbeys by Henry VIII, most of these exemptions from tithes would have fallen with them, and the lands become tithable again; had they not been supported and upheld by the statute 31 Hen. VIII. c.13. which enacts, that all persons who should come to the possession of the lands of any abbey then dissolved, should hold them free and discharged of tithes, in as large and ample a manner as the abbeys themselves formerly held them. And from this original have sprung all the lands, which, being in lay hands, do at present claim to be tithe-free: for, if a man can shew his lands to have been such abbey lands, and also immemorially discharged of tithes by any of the means before-mentioned, this is now a good prescription de non decimando. But he must shew both these requisites ; for abbey lands, without a special ground of discharge, are not discharged of course ; neither will any prescription de non decimando avail in total discharge of tithes, unless it relates to such abbeylands.[36]:31–32

The Tithe Barn, Abbotsbury, Dorset (scene of the sheep-shearing in Thomas Hardy's Far from the Madding Crowd)

The Tithe Barn, Abbotsbury, Dorset (scene of the sheep-shearing in Thomas Hardy's Far from the Madding Crowd) Tithe Barn at Bradford on Avon, West Wiltshire

Tithe Barn at Bradford on Avon, West Wiltshire Interior of the medieval tithe barn at Pilton, Somerset

Interior of the medieval tithe barn at Pilton, Somerset Coggeshall near Braintree Essex, the timber has been dated to between 1130 and 1270

Coggeshall near Braintree Essex, the timber has been dated to between 1130 and 1270

See also

- Church of the Tithes in Kiev

- Council on the Disposition of the Tithes

- Peter's Pence

- Status of religious freedom by country

- Tithe: A Modern Faerie Tale novel by Holly Black

- Tithing

- Tithing (country subdivision)

- Zakat the Islamic concept of tithing and alms

Notes

- ↑ David F. Burg (2004). A World History of Tax Rebellions. pp. viii.

- ↑ D. L. Baker, Tight fists or open hands?: wealth and poverty in Old Testament law (2009) Page 239. "This was provided by means of a tithe of agricultural produce. a. Tithes in the Ancient Near East None of the extant laws deal with tithing, though other documents show that it was a widespread practice in the ancient Near East."

- ↑ WW Hallo, Origins: The Ancient Near Eastern Background of Some Modern Western Institutions (Studies in the History and Culture of the Ancient Near East VI; Leiden/New York/Köln)

- ↑ Menahem Herman Tithe as gift: the institution in the Pentateuch and in light of ... 1992 Page 127 "Hallo recognizes comparisons for Israel with its ancient Near Eastern environment. However, in the instance of the tithe, comparisons with other ancient Near Eastern evidence has already been shown to be ambiguous, given the lack of ..."

- ↑ Bertil Albrektson, Remembering all the way--: a collection of Old Testament studies (1981) Page 116. "THE TITHES IN THE OLD TESTAMENT BY H. JAGERSMA Brussels I. Introduction "In the Old Testament as well as in other Ancient Near Eastern literature, we find only scant evidence for the practice of tithing and the collection of tithes."

- ↑ https://OI.UCHICAGO.EDU/SITES/OI.UCHICAGO.EDU/FILES/UPLOADS/SHARED/DOCS/CAD_E.PDF

- ↑ Joshua A. Berman Created Equal: How the Bible Broke With Ancient Political Thought 2008 Page 92 "Cognates of the Hebrew word for tithe, ma'a ̆ser, likewise connote activities of taxation elsewhere in the ancient Near East. In Ugarit, the ma's ̆aru or mas ̆ertu was a payment consisting of a tenth of products of the field and on ..."

- ↑ The Talmud Adin Steinsaltz 1992 "Yet if a priest has first tithe in his possession, he need not give it to a Levite. Ezra penalized the Levites of his generation because they did not return to Eretz Israel with him, and he decreed that first tithe should be given to ..."

- ↑ Restoration: Old Testament, Jewish, and Christian perspectives p329 James M. Scott - 2001 "One says that the Levites were punished because they did not come up to the Land of Israel during Ezra's days. The other says that the first tithe was given to the priests, so that they would have food when they were in a state of ..."

- ↑ See Singer, Isidore; et al., eds. (1901–1906). "MA'ASEROT". Jewish Encyclopedia. New York: Funk & Wagnalls Company.

- ↑ Maimonides. "Mishneh Torah, Sefer Korbanot: Bechorot, Perek 6, Halacha 2".

- ↑ "blueletterbible.org Strong's G586". Blue Letter Bible.

- ↑ Plowden, Francis (1806). The Principles and Law of Tithing. p. 7.

- ↑ "CATHOLIC ENCYCLOPEDIA: Tithes".

- ↑ "The Tithing Tradition" (PDF). The Church of the Nazarene. Retrieved 23 September 2016.

- ↑ Сильвестрова, Е. В. (2012-03-24). "ДЕСЯТИНА" [Tithe]. In Gundyayev, Vladimir Mikhailovich. Православная энциклопедия [Orthodox encyclopedia] (in Russian). 14 (Electronic version ed.). Церковно-научный центр «Православная Энциклопедия». pp. 450–452. Retrieved 2015-01-23.

На Востоке Д[есятина] не получила такого распространения, как на Западе. Известна, в частности, конституция императоров Льва и Антемия, в которой священнослужителям запрещалось принуждать верующих к выплатам в пользу Церкви под угрозой различных прещений. Хотя в конституции не употребляется термин decima, речь идет о начатках и, по всей видимости, о выплатах, аналогичных Д., к-рые, по мнению императоров, верующие должны совершать добровольно, без всякого принуждения [...].

- ↑ "Lesson 44: Malachi Teaches about Tithes and Offerings", Primary 6: Old Testament, LDS Church, 1996, pp. 196–201

- ↑ "Gospel Topics - What the Church Teaches about Tithing". lds.org.

- ↑ Russell M. Nelson. "Combatting Spiritual Drift—Our Global Pandemic". lds.org.

- ↑ The Church of Jesus Christ of Latter-Day Saints. "FAQ - Mormon.org". mormon.org.

- ↑ The book Meezan, by Javed Ahmed Ghamidi, published by Al-Mawrid, 2002, Lahore, Pakistan

- 1 2 3 Zysow, A. Zakāt (2009), P. Bearman; Th. Bianquis; C.E. Bosworth; E. van Donzel; W.P. Heinrichs, eds., Encyclopaedia of Islam (Second ed.), Brill. Available from Brill Online (subscription).

- ↑ Robinson, Neal. Islam; A Concise Introduction. Richmond; Curzon Press. 1999

- ↑ Chapter 2 verse 155, "be sure we shall test you with something of fear and hunger, some loss on goods, lives, and fruits. But give glad tidings to those who patiently persevere."

- ↑ "Daswandh". www.encyclopedia.com. Retrieved 20 January 2012.

- ↑ "Daswandh - Gateway to Sikhism". www.allaboutsikhs.com. Retrieved 20 January 2012.

- ↑ "Middlesex: London City without the Walls: St Botolph without Aldgate, parish". The National Archives Collection IR 18/5462.

- 1 2 How to look for records of Tithes - The History of Tithes The National Archives

- ↑ Publication 517, Social Security and Other Information for Members of the Clergy and Religious Workers (2015), Internal Revenue Service, U.S. Dep't of the Treasury. Retrieved 2016-09-23

- ↑ "Chapter 7 - The Evangelical-Lutheran Church of Denmark". Folketinget. 2013-08-23. Retrieved 2017-03-30.

- ↑ "Verot ja muut tulot". EVL.fi (in Finnish). Suomen evankelisluterilainen kirkko. Retrieved 17 May 2013.

- 1 2 3 "Excommunication for German Catholics who refuse church tax". The Times. September 21, 2012.

- ↑ "BBC News German Catholics lose church rights for unpaid tax 2012-09-24". BBC News.

- ↑ Church of Scotland (Property and Endowments) Act 1925, Part I.

- ↑ from praedium, a farm

- 1 2 3 4 5 6 Blackstone, William (1766). Commentaries on the Laws of England vol II. Oxford: Clarendon Press.

References

- Albright, W. F. and Mann, C. S. Matthew, The Anchor Bible, Vol. 26. Garden City, New York, 1971.

- The Assyrian Dictionary of the Oriental Institute of the University of Chicago, Vol. 4 "E." Chicago, 1958.

- Fitzmyer, Joseph A. The Gospel According to Luke, X-XXIV, The Anchor Bible, Vol. 28A. New York, 1985.

- Grena, G.M. (2004). LMLK--A Mystery Belonging to the King vol. 1. Redondo Beach, California: 4000 Years of Writing History. ISBN 0-9748786-0-X.

- Speiser, E. A. Genesis, The Anchor Bible, Vol.1. Garden City, New York, 1964.

- Kelly, Russell Earl, "Should the Church Teach Tithing? A Theologian's Conclusions about a Taboo Doctrine," IUniverse, 2001.

- Matthew E. Narramore, "Tithing: Low-Realm, Obsolete & Defunct" - April 2004 - (ISBN 0-9745587-02)

- Croteau, David A. "You Mean I Don't Have to Tithe?: A Deconstruction of Tithing and a Reconstruction of Post-Tithe Giving" (McMaster Theological Studies)

Further reading

- Gower, Granville William Gresham Leveson- (1883). Tithes : a paper read at the Diocesan Conference at Rochester. Rochester: Rochester Diocese.

External links

| Look up tithe in Wiktionary, the free dictionary. |

| Wikimedia Commons has media related to Tithe. |

- Theologian Russell Kelly on tithing

- Tithing at DMOZ

- Q & A On Tithing By Russ Kelly

- Articles By New Testament Scholar Dr. David Croteau

- The Tithe Debate - Arguments For and Against Christian Tithing Today

- A brief history of tithes in England at the Wayback Machine (archive index)

- Do Christian Tithe?