Private equity secondary market

| Financial market participants |

|---|

|

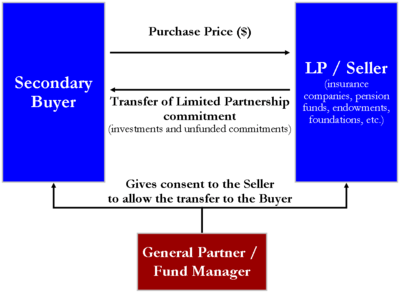

In finance, the private equity secondary market (also often called private equity secondaries or secondaries) refers to the buying and selling of pre-existing investor commitments to private equity and other alternative investment funds. Given the absence of established trading markets for these interests, the transfer of interests in private equity funds as well as hedge funds can be more complex and labor-intensive.[1]

Sellers of private equity investments sell not only the investments in the fund but also their remaining unfunded commitments to the funds. By its nature, the private equity asset class is illiquid, intended to be a long-term investment for buy-and-hold investors, including "pension funds, endowments and wealthy families selling off their private equity funds before the pools have sold off all their assets."[2] For the vast majority of private equity investments, there is no listed public market; however, there is a robust and maturing secondary market available for sellers of private equity assets.

Buyers seek to acquire private equity interests in the secondary market for multiple reasons. For example, the duration of the investment may be much shorter than an investment in the private equity fund initially. Likewise, the buyer may be able to acquire these interests at an attractive price. Finally, the buyer can evaluate the fund's holdings before deciding to purchase an interest in the fund. Conversely, sellers may seek to sell interest for various reasons, including the need to raise capital, the desire to avoid future capital calls, the need to reduce an over-allocation to the asset class or for regulatory reasons.[3]

Driven by strong demand for private equity exposure over the past decade, a significant amount of capital has been committed to secondary market funds from investors looking to increase and diversify their private equity exposure.

Secondary market participants

The private equity secondary market features dozens of dedicated firms and institutional investors that engage in the purchase and sale of private equity interests. Recent estimates by advisory firm Evercore gauged the overall secondary market’s size for 2013 to be around $26 billion,[4] with approximately $45 billion of dry powder available at the end of 2013 and a further $30 billion expected to be raised in 2014.[5] Such large volumes have been fueled by an increasing number of players over the years, which ultimately led to what today has become a highly competitive and fragmented market. Leading secondary investment firms with current dedicated secondary capital in excess of circa $3 billion include: AlpInvest Partners, Ardian (formerly AXA Private Equity), Capital Dynamics, Coller Capital, HarbourVest Partners, Lexington Partners, Pantheon Ventures, Partners Group and Neuberger Berman.[6]

Other secondary firms with circa $1–3 billion of current dedicated capital to secondaries include Adams Street Partners, Greenpark Capital, Hamilton Lane, Industry Ventures, Landmark Partners, LGT Capital Partners, Newbury Partners, Permal Capital Management, Pomona Capital, Saints Capital, W Capital Partners and Willowridge Partners.[6][7]

Additionally, major investment banking firms including Credit Suisse, Deutsche Bank, Goldman Sachs, JPMorgan Chase, Morgan Stanley have active secondary investment programs.[7] Other institutional investors typically have appetites for secondary interests. More and more primary investors, whether private equity funds-of-funds or other institutional investors, also allocate some of their primary program to secondaries.

Within the secondary arena, certain smaller specialized firms, including Delta-v Capital, Founders Circle Capital, Industry Ventures, Lake Street Capital, Nova Capital Management, Saints Capital, Sobera Capital, Verdane Capital, Vision Capital, W Capital and Azini Capital, focus on purchasing portfolios of direct investments in operating companies, referred to as secondary directs. Other niches within the secondary market include purchases of interests in fund-of-funds and secondary funds (Montauk Triguard), purchases of interests in real estate funds (Landmark Partners, Madison Harbor Capital and Strategic Partners Fund Solutions)[8] and smaller transactions (Headlands Capital and Auldbrass Partners).

As the private equity secondary market matures, non-traditional secondary strategies are emerging. One such strategy is preferred capital, where both Limited Partners and General Partners can raise additional capital at net asset value whilst preserving ownership of their portfolio and its future upside.

While intermediation in the secondary market is still not as pervasive as in corporate mergers and acquisitions, leading advisors to secondary market sellers include investments banks (e.g., Evercore, Greenhill Cogent (fka Cogent Partners),[9] Credit Suisse, Houlihan Lokey, Lazard, UBS), dedicated boutique firms (e.g. Tullett Prebon Alternative Investments, Cebile Capital LLP[10] and Setter Capital Inc), electronic exchanges (e.g., SecondMarket), social network (e.g., SecondaryLink), as well as established fund placement agents (e.g., Campbell Lutyens, Park Hill Group[11] and Triago). Since 2008, there have been a growing number of new entrants into the secondary transaction space, hoping to capitalize on what is perceived to be a growing market opportunity.

Other independent advisory firms such as LP Analyst[12] have also sprung up to provide private equity investors with third-party analysis supporting secondary buy-side and sell-side transactions assessments.

Types of secondary transactions

Secondary transactions can be generally split into two basic categories:

Sale of fund interests

A common secondary transaction, this category includes the sale of an investor's interest in a private equity fund or portfolio of interests in various funds through the transfer of the investor's limited partnership or LLC Member ownership interest in the fund(s). Nearly all types of private equity funds (e.g., including buyout, growth equity, venture capital, mezzanine, distressed, and real estate) can be sold in the secondary market. The transfer of the fund interest typically will allow the investor to receive some liquidity for the funded investments as well as a release from any remaining unfunded obligations to the fund. In addition to traditional cash sales, sales of fund interests are consummated through a number of structured transactions:[13]

- ==== Structured joint ventures ====

— Includes a wide variety of negotiated transactions between the buyer and seller that typically is customized to the specific needs of the buyer and seller. Typically, the buyer and seller agree on an economic arrangement that is more complex than a simple transfer of 100% ownership of the fund interest.[13]

- ==== Securitization ====

— An investor contributes its fund interests into a new vehicle (a collateralized fund obligation vehicle) which in turn issues notes and generates partial liquidity for the seller. Typically, the investor will also sell a portion of the equity in the leveraged vehicle. Also referred to as a collateralized fund obligation vehicle.[13]

- ==== Stapled transactions ====

— (commonly referred to as "stapled secondaries") Occurs when a private equity firm (the GP) is raising a new fund. A secondary buyer purchases an interest in an existing fund from a current investor and makes a new commitment to the new fund being raised by the GP.[13] These transactions are often initiated by private equity firms during the fundraising process.[14] They had become less and less frequent during 2008 and 2009 as the appetite for primary investments shrunk. Since 2009, a limited number of spinout transactions have been completed involving captive teams within financial institutions.[15][16][17]

Sale of direct interests

- ==== Secondary directs or synthetic secondaries ====

– This category is the sale of portfolios of direct investments in operating companies, rather than limited partnership interests in investment funds. These portfolios historically have originated from either corporate development programs or large financial institutions. Typically, this category can be subdivided as follows:

- ==== Secondary direct ====

— The sale of a captive portfolio of direct investments to a secondary buyer that will either manage the investments themselves or arrange for a new manager for the investments.[13] One of the most notable examples of a corporate seller engaging into a direct portfolios sale is the two consecutive sales of direct portfolios from AEA Technology to Coller Capital and Vision Capital in 2005 and 2006 respectively.

- ==== Synthetic secondary or spinout ====

— Under a synthetic secondary transaction, secondary investors acquire an interest in a new limited partnership that is formed specifically to hold a portfolio of direct investments.[13] Typically the manager of the new fund had historically managed the assets as a captive portfolio. The most notable example of this type of transaction is the spinout of MidOcean Partners from Deutsche Bank in 2003.

- ==== Tail-end ====

— This category typically refers to the sale of the remaining assets in a private equity fund that is approaching, or has exceeded, its anticipated life.[13] A tail-end transaction allows the manager of the fund to achieve liquidity for the fund's investors.

- ==== Structured secondary ====

– This category typically refers to the structured sale of a portfolio of private equity fund interests whereby the seller keeps some or all of the fund interests on its balance sheet but the buyer agrees to fund all future capital calls of the seller's portfolio in exchange for a preferred return secured against future distributions of the seller's portfolio. These type of secondary transactions have become increasingly explored since mid-2008 and throughout 2009 as many sellers did not want to take a loss through a straight sale of their portfolio at a steep discount but instead were ready to abandon some of the future upside in exchange for a bridge of the uncalled capital commitments.

History

| History of private equity and venture capital |

|---|

| Early history |

| (Origins of modern private equity) |

| The 1980s |

| (Leveraged buyout boom) |

| The 1990s |

| (Leveraged buyout and the venture capital bubble) |

| The 2000s |

| (Dot-com bubble to the credit crunch) |

Early history

The Venture Capital Fund of America (today VCFA Group), founded in 1982 by Dayton Carr, was likely the first investment firm[18] to begin purchasing private equity interests in existing venture capital, leveraged buyout and mezzanine funds, as well as direct secondary interests in private companies. Early pioneers in the secondary market include Jeremy Coller, the founder of UK-based Coller Capital, Arnaud Isnard, who worked with Carr at VCFA and would later form ARCIS, a secondary firm based in France[19] as well as Stanley Alfeld, founder of Landmark Partners.[20]

In the years immediately following the dot-com crash, many investors sought an early exit from their outstanding commitments to the private equity asset class, particularly venture capital.[21] As a result, the nascent secondary market became an increasingly active sector within private equity in these years.[22][23] Secondary transaction volume increased from historical levels of 2% or 3% of private equity commitments to 5% of the addressable market.[24][25][26] Many of the largest financial institutions (e.g., Deutsche Bank, Abbey National, UBS AG) sold portfolios of direct investments and “pay-to-play” funds portfolios that were typically used as a means to gain entry to lucrative leveraged finance and mergers and acquisitions assignments but had created hundreds of millions of dollars of losses.

2004 to 2007

The surge in activity in the secondary market, between 2004 and 2007, prompted new entrants to the market. It was during this time that the market evolved from what had previously been a relatively small niche into a functioning and important area of the private equity industry. Prior to 2004, the market was still characterized by limited liquidity and distressed prices with private equity funds trading at significant discounts to fair value.[27] Beginning in 2004 and extending through 2007, the secondary market transformed into a more efficient market in which assets for the first time traded at or above their estimated fair values and liquidity increased dramatically. During these years, the secondary market transitioned from a niche sub-category in which the majority of sellers were distressed to an active market with ample supply of assets and numerous market participants.[28] By 2006, active portfolio management had become far more common in the increasingly developed secondary market, and an increasing number of investors had begun to pursue secondary sales to rebalance their private equity portfolios. The continued evolution of the private equity secondary market reflected the maturation and evolution of the larger private equity industry.

2008 and the credit crisis

The secondary market for private equity interests has entered a new phase in 2008 with the onset and acceleration of the credit crunch. Pricing in the market fell steadily throughout 2008 as the supply of interests began to greatly outstrip demand and the outlook for leveraged buyout and other private equity investments worsened. Financial institutions, including Citigroup and ABN AMRO as well as affiliates of AIG and Macquarie were prominent sellers.

With the crash in global markets from in the fall of 2008, more sellers entered the market including publicly traded private equity vehicles, endowments, foundations and pension funds. Many sellers were facing significant overcommittments to their private equity programs and in certain cases significant unfunded commitments to new private equity funds were prompting liquidity concerns.[29] With the dramatic increase in the number of distressed sellers entering the market at the same time, the pricing level in the secondary market dropped rapidly. In these transactions, sellers were willing to accept major discounts to current valuations (typically in reference to the previous quarterly net asset value published by the underlying private equity fund manager) as they faced the prospect of further asset write-downs in their existing portfolios or as they had to achieve liquidity under a limited amount of time.

At the same time, the outlook for buyers became more uncertain and a number of prominent secondary players were slow to purchase assets. In certain cases, buyers that had agreed to secondary purchases began to exercise material adverse change (MAC) clauses in their contracts to walk away from deals that they had agreed to only weeks before.[30]

Private equity fund managers published their December 2008 valuations with substantial write-downs to reflect the falling value of the underlying companies. As a result, the discount to Net Asset Value offered by buyers to sellers of such assets was reduced. However, activity in the secondary market fell dramatically from 2008 levels as market participants continued to struggle to agree on price. Reflecting the gains in the public equity markets since the end of the first quarter, the dynamics in the secondary market continued to evolve. Certain buyers that had been reluctant to invest earlier in the year began to return and non-traditional investors were more active, particularly for unfunded commitments, than they had been in previous years.

2010 to 2011 - Post Financial Crisis

Since mid-2010, the secondary market has seen increased levels of activity resulting from improved pricing conditions. Through the middle of 2011, the level of activity has continued to remain at elevated levels as sellers have entered the market with large portfolios, the most attractive funds being transacted at around NAV. As the European sovereign debt crisis hit the financial markets during summer 2011, the Private equity secondary market subsequently saw a decrease both in supply and demand for portfolios of interests in private equity funds, leading to reduced pricing levels compared to pre-summer 2011. However, the volumes on the secondary market were not expected to decrease in 2012 compared to 2011, a record year[31]) as, in addition to the banks under pressure from the BASEL III regulations, other institutional investors, including pension funds, Insurances and even Sovereign wealth fund continued to utilize the Private equity secondary market to divest assets.[32]

In terms of fundraising, secondary investment firms have been the beneficiaries of the gradually improving private equity fundraising market conditions. From 2010 through 2013, each of the large secondary fund managers have raised successor investments funds, sometimes exceeding their fundraising targets.[33][34][35][36]

2012

2012 saw a record level of activity on the secondary market peaking at around $26bn of transaction completed. Lloyds Banking Group plc sold a $1.9bn portfolio of Private Equity funds to Coller Capital.[37] New York City Employees Retirement System sold a $975 million portfolio of private equity fund interests.[38] State of Wisconsin Investment Board sells a $1 billion portfolio of large buyout fund interests[38] Swedish Länsförsäkringar sold a €1.5bn PE portfolio.[39]

2013

In February, NorthStar Realty Finance spent $390 million buying a 51 percent stake in a portfolio of 45 real estate fund interests previously owned by financial services organization TIAA-CREF. Growth in the secondary market continued trending upward in 2013 reaching its highest level yet, with an estimated total transaction volume of $36bn per the Setter Capital Volume Report 2013, as follows: private equity $28 billion, real estate secondaries $5.1 billion, hedge fund side pockets $1.6 billion, infrastructure funding $0.7 billion and timber fund deals at $0.2 billion.[40] Average discount to net asset value decreased from 35% in 2009 to 7% in 2013.[2]

2014

Growth in the secondary market continued trending upward in 2014 reaching its highest level yet, with an estimated total transaction volume of $49.3bn per the Setter Capital Volume Report 2014, as follows: private equity $37.9 billion, real estate secondaries $6.8 billion, hedge fund side pockets $2.5 billion, infrastructure funding $1.9 billion and timber fund deals at $0.2 billion.[41] According to Setter Capital Inc, there were a total of 1270 transactions in 2014, with an average size of approximately $37.7 million. Although the number of transactions was roughly the same as in 2013, the average deal size increased 34.6% year over year, reflecting the fact that more multi-hundred million / billion+ dollar transactions were completed in 2014. Indeed, the breadth and number of buyers continues to increase with total volume and activity of small and medium buyers becoming more significant. Large buyers accounted for 59.8% of the market’s total volume in 2014, while mid-sized buyers accounted for roughly 34.9% of total volume and small buyers represented roughly 5.3%. Also driving the expansion of the secondary market is the number of buyers expanding their scope of interest into areas in which they were previously inactive. Approximately 31.4% of buyers broadened their secondary focus in 2014 to include buying other alternative investment types (e.g. infrastructure, real estate, portfolios of direct, etc.) – an increase of 1.4% from 2013.[42]

Milestones

The following is a timeline of some of the most notable secondary transactions and other milestones:

2011

- Coller Capital acquires Crédit Agricole Private Equity (CAPE) and the large majority of the funds CAPE manages.[43]

- AXA Private Equity completes a series of large portfolio purchases including $1.7 billion of private equity fund assets from Citigroup[44] and $740 million of fund assets from Barclays.[45]

- Auldbrass Partners founded as a spinout from Citigroup

- CalPERS sells an $800 million portfolio of private equity funds to AlpInvest Partners.[46]

2010

- Lloyds Banking Group plc sells a portfolio comprising 33 funds interests, primarily European mid-market funds, for a value of $730m to Lexington Partners.[47] In a separate transaction Lloyds sells a £480 million portfolio to Coller Capital through a joint venture.[48]

- Citigroup sells a $1 billion portfolio of funds interests and co-investments to Lexington Partners. As part of the deal, StepStone Group will take over management of a portfolio of funds-of-funds and buyout co-investments previously run by Citi Private Equity .[49]

- Bank of America sells a portfolio comprising 60 funds interests for a value of $1.9 billion to AXA Private Equity.[50]

2009

- 3i sells its European venture capital portfolio comprising interests in 30 companies for $220m to DFJ Esprit, a venture capital fund backed by two global private equity investors - HarbourVest Partners and Coller Capital.[51]

- APEN (fka AIG Private Equity) refinances its private equity fund portfolio through a $225m structured secondary transaction led by Fortress Investment Group.[52][53]

2008

- ABN AMRO sells a portfolio of private equity interests in 32 European companies managed by AAC Capital Partners to a consortium comprising Goldman Sachs, AlpInvest Partners, and CPP for $1.5 billion.[54][55]

- Macquarie Capital Alliance, in June 2008, announced a takeover offer from a consortium of private equity secondary firms including AlpInvest Partners, HarbourVest Partners, Pantheon Ventures, Partners Group, Paul Capital, Portfolio Advisors, and Procific (a subsidiary of the Abu Dhabi Investment Authority) in one of the first public to private transactions of a publicly traded private equity company completed by secondary market investors.[56][57]

- 17Capital founded - a pioneer of preferred capital, a non-traditional secondary strategy.

2007

- California Public Employees' Retirement System (CalPERS) agrees to the sale of $2.1 billion portfolio of legacy private equity funds at the end of 2007, after a process that had lasted more than a year.[58] The buying group included Oak Hill Investment Management, Conversus Capital, Lexington Partners, HarbourVest, Coller Capital, and Pantheon Ventures.[59][60]

- Coller Capital completes $4.8 billion fundraising and Lexington Partners completes $3.8 billion fundraising for their newest funds, the largest and second largest funds raised to date in the secondary market[61][62]

- Ohio Bureau of Workers' Compensation sells a $400 million portfolio of private equity fund interests to Pomona Capital[63][64]

- MetLife sells a $400 million portfolio of private equity fund interests to CSFB Strategic Partners[65]

- Bank of America completes the spin-out of BA Venture Partners to form Scale Venture Partners, which was funded by an undisclosed consortium of secondary investors

2006

- Goldman Sachs Vintage Funds purchases a $1.4 billion private equity portfolio (fund and direct interests) from Mellon Financial Corporation, following the announcement of Mellon's merger with Bank of New York[66]

- American Capital Strategies sells a $1 billion portfolio of investments to a consortium of secondary buyers including HarbourVest Partners, Lexington Partners and Partners Group[67][68][69]

- Bank of America completes the spin-out of BA Capital Europe to form Argan Capital, which was funded by an undisclosed consortium of secondary investors

- JPMorgan Chase completes the sale of a $900 million interest in JPMP Global Fund to a consortium of secondary investors

- Temasek Holdings completes $810 million securitization of a portfolio of 46 private equity funds[70]

- The Equitable Life Assurance Society completes the £435 million sale of a portfolio of 10 real estate secondaries to Liquid Realty Partners[71]

2005

- Dresdner Bank sells a $1.4 billion private equity funds portfolio to AIG

- Lexington Partners and AlpInvest Partners acquired a portfolio of private equity fund interests from Dayton Power & Light, an Ohio-based electric utility[72][73][74]

- Merrill Lynch completes the sale of a 20 fund portfolio of private equity funds to Lexington Partners[75]

2004

- Bank One sells a $1 billion portfolio of private equity fund interests to Landmark Partners

- The State of Connecticut Retirement and Trust completes the sale of a portfolio of private equity funds interests to Coller Capital, representing one of the first secondary market sales by a US pension fund

- Abbey National plc completes the sale of £748m ($1.33 billion) of LP interests in 41 private equity funds and 16 interests private European companies, to Coller Capital[76]

- Swiss Life sold more than 40 fund and direct investments to Pantheon Ventures[77]

2003

- HarbourVest acquires a $1.3 billion of private equity fund interests in over 50 funds from UBS AG through a joint venture transaction[78]

- Deutsche Bank sells a $2 billion investment portfolio to a consortium of secondary investors, led by NIB Capital (today AlpInvest), that would become MidOcean Partners[79]

2002

- W Capital, first fund developed to purchase direct company positions on a secondary basis, formed[80]

2001

- Coller Capital acquires 27 companies owned by Lucent Technologies, kick-starting the evolution of the market for "secondary direct" or "synthetic secondary" interests.[81]

2000

- Lexington Partners and Hamilton Lane acquire $500 million portfolio of private equity funds interests from Chase Capital Partners

- Coller Capital and Lexington Partners complete the purchase of over 250 direct equity investments valued at nearly $1 billion from National Westminster Bank[82]

1999

- The Crossroads Group, which was subsequently acquired by Lehman Brothers, acquired a $340 million portfolio of direct investments in large- to mid-cap companies from Electronic Data Systems (EDS)[83][84]

1998

- Coller Capital launches the first globally focused secondaries fund

1997

- Secondary volume estimated to exceed $1 billion for first time

1994

- Lexington Partners founded by former Landmark Partners professionals Brent Nicklas and Richard Lichter (currently Newbury Partners)[85]

- Coller Capital launches Europe's first secondary fund

1992

- Landmark Partners acquires $157 million of LBO fund interests from Westinghouse Credit Corporation

1991

- Paul Capital founded and acquires $85 million venture portfolio from Hillman Ventures

1989

- Coller Capital founded by Jeremy Coller

- Landmark Partners founded by Stanley Alfeld, John A. Griner III and Brent Nicklas

1988

- Pantheon Ventures launched Pantheon International Participation an early dedicated secondary fund[86]

1982

- Venture Capital Fund of America founded by Dayton Carr

See also

- Private equity

- List of private equity firms

- Venture capital

- History of private equity and venture capital

References

- Lemke, Thomas P., Lins, Gerald T., Hoenig, Kathryn L. & Rube, Patricia S., Hedge Funds and Other Private Equity Funds: Regulation and Compliance (Thomson West, 2014 ed.).

- Cannon, Vincent T. Secondary Markets in Private Equity and the Future of U.S. Capital Markets, Harvard Law School.

- All about private equity investing in Secondaries (AltAssets), Sector Analysis: Case for Sectors. (Articles from 2001-2007)

- Private Equity Secondaries Ennis Knupp

- The evolution of private equity secondary activity in the United States: liquidity for an illiquid asset (Routes to Liquidity, 2004)

- Overlooking Private Equity Partnerships Can Be Costly Mistake Secondary Market Offers Liquidity for Limited Partners (Turnaround Management Association, 2006)

Notes

- ↑ Lemke, Lins, Hoenig & Rube, Hedge Funds and Other Private Equity Funds: Regulation and Compliance, §5:28; §§13:34 - 13:38 (Thomson West, 2014 ed.).

- 1 2 Ryan, Dezember (April 24, 2014). "Bargain Bin Is Now Big Deal". WSJ. Retrieved 29 April 2014.

- ↑ Lemke, Lins, Hoenig & Rube, Hedge Funds and Other Private Equity Funds: Regulation and Compliance, §13:34 (Thomson West, 2014 ed.).

- ↑ Evercore: Distressed sellers 1% of 2013 market volume PEI Media, 14 April 2014

- ↑ Evercore: secondaries funds target $30bn PEI Media, 14 April 2014

- 1 2 The Private Equity Analyst Guide to the Secondary Market. Private Equity Analyst, 2004

- 1 2 Source: Private Equity Intelligence

- ↑ Secondary real estate market quietly ramps up. Reuters, Sep 20, 2007

- ↑ Greenhill Expands Capital Advisory Capabilities through Acquisition of Cogent Partners. Greenhill, Feb 10, 2015

- ↑

- ↑ Blackstone to Spin Off Financial Advisory Business. Blackstone, Oct 10, 2014

- ↑ Fortune Ins and outs at Cogent Partners. Fortune October 2011

- 1 2 3 4 5 6 7 The Private Equity Secondaries Market, A complete guide to its structure, operation and performance The Private Equity Secondaries Market, 2008

- ↑ "Escaping PE Purgatory Through A Secondary Sale." Buyouts, July 7, 2007

- ↑ "UK GPs: It’s spin-out time ." PrivateEquity Online, July 15, 2010

- ↑ "Lehman to spin out European mezzanine unit." Financial Times, May 10, 2010

- ↑ "Fidelity spin-out doubles in size." Financial News, February 23, 2010

- ↑ Contrarian : Second Helping (Dealmaker, 2007)

- ↑ "Secondary sales of private equity interests." AltAssets, February 18, 2002

- ↑ The Private Equity Analyst: PE Wire Archived 2008-09-10 at the Wayback Machine. (Private Equity Analyst), February 24, 2003.

- ↑ Cortese, Amy. "Business; Private Traders See Gold in Venture Capital Ruins." New York Times, April 15, 2001.

- ↑

- "Secondaries Getting Primary Attention." Buyouts, July 22, 2002

- ↑ "Secondaries Pros Discuss Market's Evolution." Secondaries Pros Discuss Market's Evolution - Cont'd. Buyouts, December 16, 2002

- ↑ Vaughn, Hope and Barrett, Ross. "Secondary Private Equity Funds: The Perfect Storm: An Opportunity in Adversity". Columbia Strategy, 2003.

- ↑ Rossa, Jennifer and White, Chad. Dow Jones Private Equity Analyst Guide to the Secondary Market (2007 Edition).

- ↑ A Secondary Market for Private Equity is Born, The Industry Standard, 28 August 2001

- ↑ "Buyouts Still Dominate Surging Secondaries Market: Some Say Market Is Overcapitalized Fund-of-Join The Game." Buyouts, May 24, 2004

- ↑ Private Equity Market Environment: Spring 2004, Probitas Partners

- ↑ Cash panic sweeping VC industry: The capital calls problem VentureBeat, November 7, 2008

- ↑ MAC uncertainty grips sellers in secondary market Private Equity Online, November 3, 2008

- ↑ Secondary market set to break records, Private Equity Online, February 1, 2012

- ↑ Singapore’s GIC Said to Offer $700 Million in Buyout-Fund Stakes, Bloomberg, January 20, 2012

- ↑ LGT Capital Partners announces final close of Crown Global Secondaries II plc. LGT Capital Partners, June 24, 2010

- ↑ Morgan Stanley beats target for $500m secondaries fund. Efinancial News, May 18, 2010

- ↑ Axa Private Equity Said to Seek More Capital for Secondary Fund. Bloomberg, February 1, 2012

- ↑ Credit Suisse Raises $2.9 Billion to Purchase Secondary Stakes, Business Week,February 14, 2012

- ↑ European Secondaries Deal of the Year, 2012 Archived 2013-09-21 at the Wayback Machine. Private Equity International, March 13, 2013

- 1 2 Running From Megafunds, Wisconsin Sells $1B Portfolio.

- ↑ Swedish Länsförsäkringar to sell €1.5bn PE portfolio. Unquote PE, August 20, 2012

- ↑ Private equity secondary deal volume totals $36 bln: survey Reuters: PE Hub, DECEMBER 23, 2013

- ↑ Secondary volume goes through the roof Reuters: PE Hub, JANUARY 22, 2015

- ↑ Setter Capital Volume Report 2014 Setter Capital, JANUARY, 2015

- ↑ . Crédit Agricole press release, December 16, 2011

- ↑ AXA Unit to Buy $1.7 Billion Portfolio From Citigroup. New York Times, June 8, 2011

- ↑ Banks seen selling Private Equity assets, but not at any price, Reuters, July 19, 2011

- ↑ AlpInvest picks up $800m in fund stakes from CalPERS. AltAssets, April 7, 2011

- ↑ "Lexington Partners To Buy $730M Private Equity Portfolio From Lloyds ." Wall Street Journal, December 15, 2010.

- ↑ "Lloyds sells private equity division to Coller Capital." The Telegraph, July 6, 2010.

- ↑ " http://www.financialpost.com/markets/news/Citi+Divest+Private+Equity+Fund+Funds+Investments+Businesses/3270599/story.html Citi to Divest Private Equity Fund of Funds and Co-Investments Businesses."Financial Post, July 13, 2010.

- ↑ "AXA buys $1.9 billion private-equity portfolio from BofA." Reuters, April 22, 2010.

- ↑ "3i agrees VC asset sale with Coller, HarbourVest consortium." PEI Asia News, September 13, 2009.

- ↑ "PE Secondaries Alert." PE Secondaries Wire , November 2, 2009.

- ↑ "APEN Press Release."APEN, October 27, 2009.

- ↑ "Goldman group snags ABN AMRO unit." Pensions&Investments, August 12, 2008.

- ↑ "Discount offered to offload ABN Amro's Secondaries". Penews.com. 2008-08-18. Retrieved 2014-07-30.

- ↑ "Macquarie Capital will spend $836m to go private". The Australian, June 17, 2008

- ↑ "Macquarie Capital soars on buyout plan Archived 2008-08-03 at the Wayback Machine.". The Sydney Morning Herald, June 16, 2008

- ↑ CalPERs private equity stakes under microscope. Reuters 'Dealzone' November 20, 2008.

- ↑ Craig, Catherine. Five buy record $3bn Calpers portfolio. Financial News, February 5, 2008.

- ↑ Tracy, Tennille. Calpers, and where private-equity funds go to die. Wall Street Journal's Deal Journal blog, November 5, 2007.

- ↑ Press Release: Coller International Partners V closes at $4.5 billion' Archived 2007-12-28 at the Wayback Machine.

- ↑ "Lexington Capital Partners VI". Lexingtonpartners.com. Retrieved 2014-07-30.

- ↑ Primack, Dan (2007-04-03). "OBWC Portfolio Sale Nears End". Pehub.com. Retrieved 2014-07-30.

- ↑ Ohio Bureau of Worker's Compensation -- Review of Secondary Advisor Selection Process

- ↑ "Secondaries join the mainstream". Financialnews-us.com. Retrieved 2014-07-30.

- ↑ "Dow Jones Financial News: Goldman picks up Mellon portfolio". Efinancialnews.com. 2007-01-04. Retrieved 2014-07-30.

- ↑ "American Capital Raises $1 Billion Equity Fund; Expands Its Asset Management Business; Will Host 9 am Conference Call". American Capital Strategies. PR Newswire. 2006-10-04.

- ↑ American Capital raises $1bn fund Archived 2009-02-06 at the Wayback Machine.. (AltAssets)

- ↑ ACS spins off stakes into $1B fund (TheDeal.com)

- ↑ Singapore’s Temasek Hits Hard Going (Asia Sentinel, 2007)

- ↑ Liquid Realty Acquires GBP 435 Million Real Estate Secondary Portfolio. Business Wire, May 3, 2006

- ↑ AlpInvest and Lexington Partners buy $1.2bn secondary portfolio from DPL (AltAssets)

- ↑ "M&A legal guru urges more diligence". Marketwatch.com. 2005-02-17. Retrieved 2014-07-30.

- ↑ DPL to sell PE stakes for $850M (TheDeal.com)

- ↑ Lexington Partners Buys Merrill Lynch Portfolio. Private Equity Analyst, April 2005 (p.10)

- ↑ Press Release: Abbey sells private equity portfolio to Coller Capital Archived 2009-01-08 at the Wayback Machine.

- ↑ Pantheon acquires Swiss Life private equity portfolio Archived 2009-02-06 at the Wayback Machine.. AltAssets, 2004

- ↑ Name A-D E-J K-P Q-Z. "HarbourVest transactions". Harbourvest.com. Retrieved 2014-07-30.

- ↑ MidOcean Embraces Independence. Financial Times, March 9, 2003

- ↑ "The evolution of private equity secondary activity in the United States: liquidity for an illiquid asset" (PDF). Retrieved 2014-07-30.

- ↑ Press Release: Lucent Technologies and Coller Capital form independent venture firm to manage Lucent's New Ventures Group portfolio

- ↑ Press Release:The Royal Bank of Scotland: asset sale

- ↑ Lehman Brothers acquired The Crossroads Group in 2005

- ↑ Cawley, Rusty "Crossroads uses EDS portfolio to launch fund." Dallas Business Journal, September 24, 1999

- ↑ "Newbury Partners Promises To Keep A Secret." Buyouts, August 20, 2007

- ↑ Pantheon Ventures: Secondary Investments. Company Website

| Basic investment types |  | ||||||

|---|---|---|---|---|---|---|---|

| History | |||||||

| Terms and concepts |

| ||||||

| Investors | |||||||

| Related financial terms | |||||||

| |||||||