Kernel regression

Kernel regression is a non-parametric technique in statistics to estimate the conditional expectation of a random variable. The objective is to find a non-linear relation between a pair of random variables X and Y.

In any nonparametric regression, the conditional expectation of a variable relative to a variable may be written:

where is an unknown function.

Nadaraya–Watson kernel regression

Nadaraya and Watson, both in 1964, proposed to estimate as a locally weighted average, using a kernel as a weighting function.[1][2][3] The Nadaraya–Watson estimator is:

where is a kernel with a bandwidth . The denominator is a weighting term with sum 1.

Derivation

Using the kernel density estimation for the joint distribution f(x,y) and f(x) with a kernel K,

,

,

we get

which is the Nadaraya–Watson estimator.

Priestley–Chao kernel estimator

Gasser–Müller kernel estimator

![\widehat {m}_{{GM}}(x)=h^{{-1}}\sum _{{i=1}}^{n}\left[\int _{{s_{{i-1}}}}^{{s_{i}}}K\left({\frac {x-u}{h}}\right)du\right]y_{i}](../I/m/ef9b8c48ff817ab6f5fe04583774c79a9209f6d6.svg)

where

Example

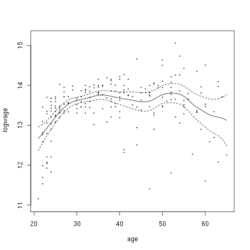

This example is based upon Canadian cross-section wage data consisting of a random sample taken from the 1971 Canadian Census Public Use Tapes for male individuals having common education (grade 13). There are 205 observations in total.

The figure to the right shows the estimated regression function using a second order Gaussian kernel along with asymptotic variability bounds

Script for example

The following commands of the R programming language use the npreg() function to deliver optimal smoothing and to create the figure given above. These commands can be entered at the command prompt via cut and paste.

install.packages("np")

library(np) # non parametric library

data(cps71)

attach(cps71)

m <- npreg(logwage~age)

plot(m,plot.errors.method="asymptotic",

plot.errors.style="band",

ylim=c(11,15.2))

points(age,logwage,cex=.25)

Related

According to David Salsburg, the algorithms used in kernel regression were independently developed and used in fuzzy systems: "Coming up with almost exactly the same computer algorithm, fuzzy systems and kernel density-based regressions appear to have been developed completely independently of one another."[4]

Statistical implementation

- MATLAB A free MATLAB toolbox with implementation of kernel regression, kernel density estimation, kernel estimation of hazard function and many others is available on these pages (this toolbox is a part of the book [5]).

- Stata kernreg2

- R: the function

npregof the np package can perform kernel regression.[6][7] - Python: the package kernel_regression as an extension of sklearn

- GNU Octave mathematical program package:

See also

References

- ↑ Nadaraya, E. A. (1964). "On Estimating Regression". Theory of Probability and its Applications. 9 (1): 141–2. doi:10.1137/1109020.

- ↑ Watson, G. S. (1964). "Smooth regression analysis". Sankhyā: The Indian Journal of Statistics, Series A. 26 (4): 359–372. JSTOR 25049340.

- ↑ Bierens, Herman J. (1994). "The Nadaraya–Watson kernel regression function estimator". Topics in Advanced Econometrics. New York: Cambridge University Press. pp. 212–247. ISBN 0-521-41900-X.

- ↑ Salsburg, D. (2002). The Lady Tasting Tea: How Statistics Revolutionized Science in the Twentieth Century. W.H. Freeman. pp. 290–91. ISBN 0-8050-7134-2.

- ↑ Horová, I.; Koláček, J.; Zelinka, J. (2012). Kernel Smoothing in MATLAB: Theory and Practice of Kernel Smoothing. Singapore: World Scientific Publishing. ISBN 978-981-4405-48-5.

- ↑ np: Nonparametric kernel smoothing methods for mixed data types

- ↑ Kloke, John; McKean, Joseph W. (2014). Nonparametric Statistical Methods Using R. CRC Press. pp. 98–106. ISBN 978-1-4398-7343-4.

Further reading

- Henderson, Daniel J.; Parmeter, Christopher F. (2015). Applied Nonparametric Econometrics. Cambridge University Press. ISBN 978-1-107-01025-3.

- Li, Qi; Racine, Jeffrey S. (2007). Nonparametric Econometrics: Theory and Practice. Princeton University Press. ISBN 0-691-12161-3.

- Pagan, A.; Ullah, A. (1999). Nonparametric Econometrics. Cambridge University Press. ISBN 0-521-35564-8.

- Simonoff, Jeffrey S. (1996). Smoothing Methods in Statistics. Springer. ISBN 0-387-94716-7.

External links

- Scale-adaptive kernel regression (with Matlab software).

- Tutorial of Kernel regression using spreadsheet (with Microsoft Excel).

- An online kernel regression demonstration Requires .NET 3.0 or later.

- Kernel regression with automatic bandwidth selection (with Python)