DBRS

|

| |

| Industry | Credit Rating, Financial Services |

|---|---|

| Predecessor | Dominion Bond Rating Service |

| Founded | 1976 |

| Founder | Walter Schroeder |

| Headquarters |

New York, Chicago, London, DBRS Tower, 181 University Avenue, Suite 700 Toronto, Canada |

| Products | Credit Ratings, Financial Research |

| Divisions | DBRS Limited; DBRS, Inc.; and DBRS Ratings Limited |

| Website |

www |

DBRS is a credit rating agency (CRA) founded in 1976 (originally known as Dominion Bond Rating Service) in Toronto by Walter Schroeder, who sold the company to a consortium led by The Carlyle Group and Warburg Pincus in December 2014. DBRS is the largest rating agency in Canada with other offices in New York, Chicago, and London. DBRS comprises three affiliated operating companies – DBRS Limited; DBRS, Inc.; and DBRS Ratings Limited. Daniel Curry is the agency’s CEO. DBRS is the fourth largest ratings agency in the world, with about a 2.5% global market share.

DBRS is registered as a Nationally Recognized Statistical Rating Organization from the United States’ Securities and Exchange Commission (SEC), one of only 10 companies to hold the designation.[1] DBRS is also registered with the European Securities and Markets Authority (ESMA) and with the Ontario Securities Commission (OSC) in Canada.

The company is one of only four CRAs, along with larger competitors Standard & Poor’s, Moody's Investors Service, and Fitch Ratings, to receive ECAI[2] recognition from the European Central Bank (ECB). That designation indicates CRAs whose ratings can be used by the ECB to determine collateral requirements for borrowing from the ECB.[3]

History

DBRS's niche is timely credit ratings that offer insight and transparency across a broad range of financial institutions, corporate entities, government bodies, and various structured finance product groups in North America, Europe, Australasia, and South America. Based in Toronto, with offices in New York, Chicago and London, DBRS is independently owned and operated, is not affiliated with any institution or organization and does not partake in any trading or underwriting activities.

The company was founded by Walter Schroeder, who started sketching out a business plan while driving to Montreal on a family vacation. He developed the ratings agency from scratch, starting the company with less than $1,000. The company opened its first office, a tiny 1,500-square-foot office, in Toronto.[4]

Since those beginnings, DBRS has expanded to become the largest ratings agency in Canada with major operation centers in the U.S. and Europe. It first opened offices in Chicago and New York in 2003 and opened its current office in London in 2010. In 2008, the organization changed its name from Dominion Bond Rating Service to DBRS.

Today, DBRS has more than 300 employees worldwide and rates more than 1,000 different companies and single-purpose 'vehicles that issue commercial paper, term debt, and preferred shares in the global capital markets.[5]

In December 2014, DBRS was sold to a consortium led by private equity firms The Carlyle Group and Warburg Pincus.[6] The deal closed on March 4, 2015.[7][8]

Corporate and Operating Structures

DBRS Limited is the operating company in Canada. DBRS, Inc. is the operating company in the United States. DBRS Ratings Limited is the operating entity based in London and is home to the agency’s broader European operations.

DBRS Limited rates structured finance and credit, corporate finance, financial institutions and infrastructure finance in Canada. DBRS, Inc. rates structured finance and credit and U.S.-based financial institutions from its U.S. offices. DBRS Ratings Ltd. rates structured finance and credit and European-based financial institutions. Global sovereign ratings analysis is done by analysts based in both the U.S. and U.K.

Size

As of Dec. 31, 2012, DBRS rated about 50,000 total securities and about 2,500 total issuers.

In the U.S., DBRS rates banks that account for about 92% of U.S. banking assets as of Dec. 31, 2012. DBRS’s ratings in Europe cover more than 60% of the region’s banking sector.

DBRS provides rating coverage for more than 30 asset classes.

DBRS currently rates 36 sovereigns and supranational organizations. One of the agency’s goals is to rate remaining members of the 17-nation euro-zone currency bloc. DBRS currently rates 10 countries that are part of the euro zone.[9]

Rating scale

Rating Scale: Long-Term Obligations[10]

The DBRS long-term rating scale provides an opinion on the risk of default. That is, the risk that an issuer will fail to satisfy its financial obligations in accordance with the terms under which an obligations has been issued. Ratings are based on quantitative and qualitative considerations relevant to the issuer, and the relative ranking of claims. All rating categories other than AAA and D also contain subcategories “(high)” and “(low)”. The absence of either a “(high)” or “(low)” designation indicates the rating is in the middle of the category. DBRS’s scale is similar to the ones used by Standard & Poor’s and Fitch Ratings, though it uses (high) and (low) instead of “+” and “–“ symbols like S&P and Fitch use.

AAA: Highest credit quality. The capacity for the payment of financial obligations is exceptionally high and unlikely to be adversely affected by future events.

AA: Superior credit quality. The capacity for the payment of financial obligations is considered high. Credit quality differs from AAA only to a small degree. Unlikely to be significantly vulnerable to future events.

A: Good credit quality. The capacity for the payment of financial obligations is substantial, but of lesser credit quality than AA. May be vulnerable to future events, but qualifying negative factors are considered manageable.

BBB: Adequate credit quality. The capacity for the payment of financial obligations is considered acceptable. May be vulnerable to future events.

BB: Speculative, non-investment-grade credit quality. The capacity for the payment of financial obligations is uncertain. Vulnerable to future events.

B: Highly speculative credit quality. There is a high level of uncertainty as to the capacity to meet financial obligations.

CCC / CC / C: Very highly speculative credit quality. In danger of defaulting on financial obligations. There is little difference between these three categories, although CC and C ratings are normally applied to obligations that are seen as highly likely to default, or subordinated to obligations rated in the CCC to B range. Obligations in respect of which default has not technically taken place but is considered inevitable may be rated in the C category.

D: A financial obligation has not been met or it is clear that a financial obligation will not be met in the near future or a debt instrument has been subject to a distressed exchange. A downgrade to D may not immediately follow an insolvency or restructuring filing as grace periods or extenuating circumstances may exist.

Rating Scale: Commercial Paper and Short-Term Debt[11]

The DBRS short-term debt rating scale provides an opinion on the risk that an issuer will not meet its short-term financial obligations in a timely manner. Ratings are based on quantitative and qualitative considerations relevant to the issuer and the relative ranking of claims. The R-1 and R-2 rating categories are further denoted by the subcategories “(high)”, “(middle)”, and “(low)”.

R-1 (high): Highest credit quality. The capacity for the payment of short-term financial obligations as they fall due is exceptionally high. Unlikely to be adversely affected by future events.

R-1 (middle): Superior credit quality. The capacity for the payment of short-term financial obligations as they fall due is very high. Differs from R-1 (high) by a relatively modest degree. Unlikely to be significantly vulnerable to future events.

R-1 (low): Good credit quality. The capacity for the payment of short-term financial obligations as they fall due is substantial. Overall strength is not as favourable as higher rating categories. May be vulnerable to future events, but qualifying negative factors are considered manageable.

R-2 (high): Upper end of adequate credit quality. The capacity for the payment of short-term financial obligations as they fall due is acceptable. May be vulnerable to future events.

R-2 (middle): Adequate credit quality. The capacity for the payment of short-term financial obligations as they fall due is acceptable. May be vulnerable to future events or may be exposed to other factors that could reduce credit quality.

R-2 (low): Lower end of adequate credit quality. The capacity for the payment of short-term financial obligations as they fall due is acceptable. May be vulnerable to future events. A number of challenges are present that could affect the issuer’s ability to meet such obligations.

R-3: Lowest end of adequate credit quality. There is a capacity for the payment of short-term financial obligations as they fall due. May be vulnerable to future events and the certainty of meeting such obligations could be impacted by a variety of developments.

R-4: Speculative credit quality. The capacity for the payment of short-term financial obligations as they fall due is uncertain.

R-5: Highly speculative credit quality. There is a high level of uncertainty as to the capacity to meet short-term financial obligations as they fall due.

D: A financial obligation has not been met or it is clear that a financial obligation will not be met in the near future, or a debt instrument has been subject to a distressed exchange. A downgrade to D may not immediately follow an insolvency or restructuring filing as grace periods, other procedural considerations, or extenuating circumstance may exist.

Sovereign Ratings

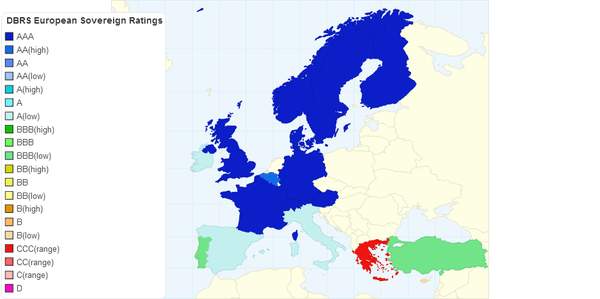

DBRS currently rates 36 sovereign and supranational ratings around the world. It currently rates 29 countries and 2 supranational (the EFSF) and ESM.[12]

|

For DBRS, a bond is considered investment grade if its credit rating is BBB(low) or higher. Bonds rated BB(high) and below are considered to be speculative grade.

|

DBRS European Sovereign Debt Ratings as of July 2, 2014  DBRS Global Sovereign Debt Ratings as of July 2, 2014 |

Regulation

In Canada, DBRS is regulated through the Canadian Securities Administrators with its principal regulator being the OSC. CRAs in Canada must become a “designated rating organization” in order for their opinions to be eligible for use under securities laws.[14]

In the U.S., DBRS is regulated by the SEC, which has proposed rules as part of the Dodd-Frank Act that will impose additional governance, transparency, conflicts of interest and performance measurement requirements on the CRA industry.

In Europe, DBRS is regulated by ESMA. Additional rules – CRA III – have been adopted in Europe focused on increasing competition, ratings transparency and independence, standardizing Sovereign ratings and adding new liability whether or not a contract is in place.[15]

See also

- A.M. Best

- Bloomberg L.P.

- Dun & Bradstreet

- Fitch Ratings

- Kroll Bond Rating Agency

- Moody's

- Morningstar, Inc.

- Nationally Recognized Statistical Rating Organizations

- Reuters

- Standard & Poor's

References

- ↑ "Credit Rating Agencies and Nationally Recognized Statistical Rating Organizations (NRSROs)". SEC. Retrieved 2013-05-31.

- ↑ "External credit assessment institution source (ECAIs)". European Central Bank. Retrieved 2013-07-01.

- ↑ Art Patnaude (August 9, 2012). "Lucky Break for Spain and Ireland with DBRS Downgrade". The Wall Street Journal.

- ↑ Grant Robertson (October 26, 2012). "Is DBRS right on Europe?". The Globe and Mail.

- ↑ "DBRS About". DBRS.

- ↑ Martin, Timothy (2014-12-18). "Credit-Rating Firm DBRS to Be Sold". Wall Street Journal. Wall Street Journal. Retrieved 7 January 2015.

- ↑ "Press Release" (PDF). Retrieved 24 May 2017.

- ↑ Alden, William. "Credit Rating Agency DBRS to Be Sold to 2 Private Equity Firms". Retrieved 24 May 2017.

- ↑ Luciana Lopez (May 24, 2013). "Exclusive: DBRS to rate all euro zone sovereigns by year-end". Reuters.

- ↑ "DBRS" (PDF). DBRS.

- ↑ "DBRS" (PDF). DBRS.

- ↑ "DBRS Sovereign and Supranational Ratings" (PDF). DBRS. Retrieved 2013-06-28.

- 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 "DBRS — Sovereign and Supranational Ratings" (PDF). Retrieved 24 May 2017.

- ↑ Sunny Freeman (September 6, 2012). "Canada to impose code of conduct on debt raters". The Globe and Mail.

- ↑ Stephen L. Bernard (October 9, 2012). "DBRS Pitches Increased Competition for Rating European Debt". The Wall Street Journal.