Capital gains tax

A capital gains tax (CGT) is a tax on capital gains, the profit realized on the sale of a non-inventory asset that was greater than the amount realized on the sale. The most common capital gains are realized from the sale of stocks, bonds, precious metals and property. Not all countries implement a capital gains tax and most have different rates of taxation for individuals and corporations.

For equities, an example of a popular and liquid asset, national and state legislation often has a large array of fiscal obligations that must be respected regarding capital gains. Taxes are charged by the state over the transactions, dividends and capital gains on the stock market. However, these fiscal obligations may vary from jurisdiction to jurisdiction.

Argentina

There is no specific capital gains tax in Argentina; however, there is a 9% to 35% tax for fiscal residents on their world revenues, including capital gains.

Australia

Australia collects capital gains tax only upon realized capital gains, except for certain provisions relating to deferred-interest debt such as zero-coupon bonds. The tax is not separate in its own right, but forms part of the income-tax system. The proceeds of an asset sold less its "cost base" (the original cost plus addition for cost price increases over time) are the capital gain. Discounts and other concessions apply to certain taxpayers in varying circumstances. From 21 September 1999, after a report by Alan Reynolds, the 50% capital gains tax discount has been in place for individuals and for some trusts that acquired the asset after that time and that have held the asset for more than 12 months, however the tax is levied without any adjustment to the cost base for inflation. The amount left after applying the discount is added to the assessable income of the taxpayer for that financial year.

For individuals, the most significant exemption is the family home. The sale of personal residential property is normally exempt from capital gains tax, except for gains realized during any period in which the property was not being used as an individual's personal residence (for example, while leased to other tenants) or portions attributable to business use. Capital gains or losses as a general rule can be disregarded for CGT purposes when assets were acquired before 20 September 1985 (pre-CGT).

Austria

Austria taxes capital gains at 25% (on checking account and "Sparbuch" interest) or 27.5% (all other types of capital gains). There is an exception for capital gains from the sale of shares of foreign entities (with opaque taxation) if the participation exceeds 10% and shares are held for over one year (so-called "Schachtelprivileg"). [1]

Barbados

There is no capital gains tax charged in Barbados.

Belgium

Under the participation exemption, capital gains realised by a Belgian resident company on shares in a Belgian or foreign company are fully exempt from corporate income tax, provided that the dividends on the shares qualify for the participation exemption. For purposes of the participation exemption for capital gains the minimum participation test is not required. Unrealised capital gains on shares that are recognised in the financial statements (which recognition is not mandatory) are taxable. But a roll-over relief is granted if, and as long as, the gain is booked in a separate reserve account on the balance sheet and is not used for distribution or allocation of any kind.

As a counterpart to the new exemption of realised capital gains, capital losses on shares, both realised and unrealised, are no longer tax deductible. However, the loss incurred in connection with the liquidation of a subsidiary company remains deductible up to the amount of the paid-up share capital.

Other capital gains are taxed at the ordinary rate. If the total amount of sales is used for the purchase of depreciable fixed assets within 3 years, the taxation of the capital gains will be spread over the depreciable period of these assets.[2]

Belize

There are no capital gains taxes for residents or non-residents in Belize.

Brazil

Capital gain taxes are only paid on realized gains. At the current stage, taxes are 15% for transactions longer than one day old and 20% for day trading, both transactions are due payable at the following month after selling or closing the position. Dividends are tax free, since the issuer company has already paid to RECEITA FEDERAL(the Brazilian IRS). Derivatives (futures and options) follow the same rules for tax purposes as company stocks. When selling less than R$20.000 (Brazilian Reais) within a month (and not operating in day trading), the financial operation is considered tax-free. Also, non-residents have no tax on capital gains.[3]

Bulgaria

The Corporate tax rate is 10%. The personal tax rate is flat at 10%. There is no capital gains tax on equity instruments traded on the BSE.

Canada

Currently, only 50% of realized capital gains are taxable in Canada at an individual's tax rate. Some exceptions apply, such as selling one's primary residence which may be exempt from taxation.[4] Capital gains made by investments in a Tax-Free Savings Account (TFSA) are not taxed.

For example, if your capital gains (profit) is $100, you are taxed on $50 at your marginal tax rate. That is, if you were in the top tax bracket, you would be taxed at approximately 43%, in Ontario. A formula for this example using the top tax bracket would be as follows:

(Capital gain x 50.00%) x marginal tax rate = capital gain tax

($100 x 50.00%) x 43% = $50 x 43% = $21.50

In this example your capital gains tax on $100 is $21.50, leaving you with $78.50.

As of the 2013 budget, interest can no longer be claimed a capital gain. The formula is the same for capital losses and these can be carried forward indefinitely to offset future years' capital gains; capital losses not used in the current year can also be carried back to the previous three tax years to offset capital gains tax paid in those years.

For corporations as for individuals, 50% of realized capital gains are taxable. The net taxable capital gains (which can be calculated as 50% of total capital gains minus 50% of total capital losses) are subject to income tax at normal corporate tax rates. If more than 50% of a small business's income is derived from specified investment business activities (which include income from capital gains) they are not permitted to claim the small business deduction.

Capital gains earned on income in a Registered Retirement Savings Plan are not taxed at the time the gain is realized (i.e. when the holder sells a stock that has appreciated inside of their RRSP) but they are taxed when the funds are withdrawn from the registered plan (usually after converting to a registered income fund.) These gains are then taxed at the individual's full marginal rate.

Capital gains earned on income in a TFSA are not taxed at the time the gain is realized. Any money withdrawn from a TFSA, including capital gains, are also not taxed.

Unrealized capital gains are not taxed.

Cayman Islands

There are no capital gains taxes charged on any transaction in the Cayman Islands. However, a Cayman Islands entity may be subject to taxation on capital gains made in other jurisdictions.

China

The applicable tax rate for capital gains in China depends upon the nature of the taxpayer (i.e. whether the taxpayer is a person or company) and whether the taxpayer is resident or non-resident for tax purposes. It should however be noted that, unlike common law tax systems, Chinese income tax legislation does not provide a distinction between income and capital. What commonly referred by taxpayers and practitioners as capital gain tax is actually within the income tax framework, rather than a separate regime.

Tax-resident enterprises will be taxed at 25% in accordance with the Enterprise Income Tax Law. Non-resident enterprises will be taxed at 10% on capital gains in accordance with the Implementing Regulations to the Enterprise Income Tax Law. In practice, where a resident of a treaty partner alienates assets situated in China as part of its ordinary course of business the gains so derived will likely be assessed as if it is a capital gain, rather than business profit. This is somewhat contradictory with the basic principles of double taxation treaty.

The only tax circular specifically addressing the PRC income tax treatment of income derived by QFIIs from the holding and trading of Chinese securities is Guo Shui Han (2009) No.47 ("Circular 47") issued by the State Administration of Taxation ("SAT") on 23 January 2009. The circular addresses the withholding tax treatment of dividends and interest received by QFIIs from PRC resident companies, however, circular 47 is silent on the treatment of capital gains derived by QFIIs on the trading of A-shares. It is generally accepted that Circular 47 is intentionally silent on capital gains and possible indication that SAT is considering but still undecided on whether to grant tax exemption or other concessionary treatment to capital gains derived by QFIIs. Nevertheless, it is noted that there have been cases where QFIIs withdraw capital from China after paying 10% withholding tax on gains derived through share trading over years on a transaction-by-transaction basis. This uncertainty has caused significant problems for those investment managers investing in A-Shares. Guo Shui Han (2009) No. 698 ("Circular 698") was issued on 10 December 2009 addressing the PRC corporate income tax treatment on the transfer of PRC equity interest by non-PRC tax resident enterprises directly or indirectly, however has not resolved the uncertain tax position with regards A-Shares. With respect to Circular 698 itself, there are views that it is not consistent with the Enterprise Income Tax Law as well as double taxation treaties signed by the Chinese government. The validity of the Circular is controversial, especially in light of recent developments in the international arena, such as the TPG case in Australia and Vodafone case in India.

Croatia

The capital gains tax in Croatia equals 12%. It was introduced in 2015.

Cyprus

As determined by the Cyprus Capital Gains Tax Law, Capital gains tax in Cyprus arising from the sale or disposition of immovable property in Cyprus or the disposal of shares of companies which own immovable property in Cyprus and not listed in a recognised stock exchange. These gains are not added to other income but are taxed separately. Payment of immovable property tax is paid by both individuals and companies on property owned in Cyprus.

Capital gains tax does not apply to profits from the sale of overseas real estate by non-residents, offshore entities, or residents who were not resident when they purchased the asset. Gains accruing from disposal of immovable property held outside Cyprus and shares in companies, the property whereof consists of immovable property held outside Cyprus, will be exempted from capital gains tax. Individuals may, subject to certain conditions, may claim certain deductions from the applicable taxable gain.[5]

Czech Republic

Capital gains in the Czech Republic are taxed as income for companies and individuals. The Czech income tax rate for an individual's income in 2010 is a flat 15% rate. Corporate tax in 2010 is 19%. Capital gains from the sale of shares by a company owning 10% or more is entitled to participation exemption under certain terms. For an individual, gain from the sale of a primary private dwelling, held for at least 2 years, is tax exempt. Or, when not used as a main residence, if held for more than 5 years.

Denmark

Share dividends and realized capital gains on shares are charged 27% to individuals of gains up to DKK 48,300 (2013-level, adjusted annually), and at 42% of gains above that.[6] Carryforward of realized losses on shares is allowed.

Individuals' interest income from bank deposits and bonds, realized gains on property and other capital gains are taxed up to 59%, however, several exemptions occur, such as on selling one's principal private residence or on gains on selling bonds. Interest paid on loans is deductible, although in case the net capital income is negative, only approx. 33% tax credit applies.

Companies are taxed at 25%. Share dividends are taxed at 28%.

Ecuador

Corporate taxation:

Residence for tax purposes is based on the place of incorporation.

Resident entities are taxed on worldwide income. Nonresidents are subject to tax only on Ecuador-source income.

Capital gains are treated as ordinary income and taxed at the normal corporate rate.

The standard rate is 22%, with a reduced rate of 15% applying where corporate profits are reinvested for the purchase of machinery or equipment and/or the acquisition of new technology. Companies engaged in the exploration or exploitation of hydrocarbon also are subject to the standard corporate tax rate.

Personal taxation:

Resident individuals are taxed on their worldwide income; nonresidents are taxed only on Ecuadorian-source income.

An individual is deemed to be resident if he/she is in Ecuador for more than 6 months in a year.

Capital gains are treated as ordinary income and taxed at the normal rate.

Rates are progressive from 0% to 35%.

Egypt

There was no capital gains tax. After the Egyptian Revolution there is a proposal for a 10% capital gains tax. This proposal came to life on 29 May 2014. Egypt exempt bonus shares from a new 10 percent capital gains tax on profits made on the stock market as the country's Finance Minister Hany Dimian said on 30 May 2014, and distributions of bonus shares will be exempt from the taxes, and the new tax will not be retroactive. [7]

Estonia

There is no separate capital gains tax in Estonia. For residents of Estonia all capital gains are taxed the same as regular income, the rate of which currently stands at 20%. Resident natural persons that have investment account can realise capital gains on some classes of assets tax free until withdrawal of funds from the investment account. For resident legal persons (includes partnerships) no tax is payable for realising capital gain (or receiving any other type of income), but only on payment of dividends, payments from capital (exceeding contributions to capital) and payments not related to business. The income tax rate for resident legal persons is 20% (payment of 80 units of dividends triggers 20 units of tax due).

Finland

The capital gains tax in Finland is 30% on realized capital income and 34% if the realized capital income is over 30,000 euros.[8] The capital gains tax in 2011 was 28% on realized capital income.[9] Carryforward of realized losses is allowed for five years. However, capital gains from the sale of residential homes is tax-free after two years of residence, with certain limitations.[10]

France

For residents, capital gains on the sale of financial instruments (shares, bonds, etc..) are taxed at the marginal tax rate (up to 45%), plus 15.5% of social contributions (i.e.: up to 60.5%). A deduction of 20 to 40% on the gross capital gain can be applied if the instrument has been held for at least 2 years.

If shares are held in a special account (called a PEA), the gain is subject only to social security taxes provided that the PEA is held for at least five years. The maximum amount that can be deposited in the PEA is €152,000.

The gain realized on the sale of a principal residence is not taxable. A gain realized on the sale of other real estate held at least 30 years, however, is not taxable, although this will become subject to 15.5% social security taxes as of 2012. (There is a sliding scale for non principal residence property owned for between 22 and 30 years.)

Non-residents are generally taxable on capital gains realized on French real estate and on some French financial instruments, subject to any applicable double tax treaty. Social security taxes, however, are not usually payable by non-residents. A French tax representative will be mandatory if you are non-resident and you sell a property for an amount over 150.000 euros or you own the real estate for more than 15 years.

Germany

In January 2009, Germany introduced a very strict capital gains tax (called Abgeltungsteuer in German) for shares, funds, certificates, bank interest rates etc. Capital gains tax only applies to financial instruments (shares, bonds etc.) that have been bought after 31 December 2008. Instruments bought before this date are exempt from capital gains tax (assuming that they have been held for at least 12 months), even if they are sold in 2009 or later, barring a change of law. Certificates are treated specially, and only qualify for tax exemption if they have been bought before 15 March 2007.

Real estate continues to be exempt from capital gains tax if it has been held for more than ten years. The German capital gains tax is 25% plus Solidarity surcharge (add-on tax initially introduced to finance the 5 eastern states of Germany – Mecklenburg-Western Pomerania, Saxony, Saxony-Anhalt, Thuringia and Brandenburg – and the cost of the reunification, but later kept in order to finance all kinds of public funded projects in all Germany), plus Kirchensteuer (church tax, voluntarily), resulting in an effective tax rate of about 28-29%. Deductions of expenses such as custodian fees, travel to annual shareholder meetings, legal and tax advice, interest paid on loans to buy shares, etc., are no longer permitted starting in 2009.

There is an allowance (Freistellungsauftrag) on capital gains income in Germany of €801 per person per year of which you do not have to be taxed, if appropriate forms are completed.

Hong Kong

In general Hong Kong has no capital gains tax. However, employees who receive shares or options as part of their remuneration are taxed at the normal Hong Kong income tax rate on the value of the shares or options at the end of any vesting period less any amount that the individual paid for the grant.

If part of the vesting period is spent outside Hong Kong then the tax payable in Hong Kong is pro-rated based on the proportion of time spent working in Hong Kong.[11] Hong Kong has very few double tax agreements and hence there is little relief available for double taxation. Therefore, it is possible (depending on the country of origin) for employees moving to Hong Kong to pay full income tax on vested shares in both their country of origin and in Hong Kong. Similarly, an employee leaving Hong Kong can incur double taxation on the unrealized capital gains of their vested shares.

The Hong Kong taxation of capital gains on employee shares or options that are subject to a vesting period, is at odds with the treatment of unrestricted shares or options which are free of capital gains tax.

For those who do trading professionally (buying and selling securities frequently to obtain an income for living) as "traders", this will be considered income subject to personal income tax rates.

Hungary

Since 1 January 2016 there is one flat tax rate (15%) on capital income. This includes: selling stocks, bonds, mutual funds shares and also interests from bank deposits. Since January 2010, Hungarian citizens can open special "long-term" accounts. The tax rate on capital gains from securities held in such an account is 10% after a 3-year holding period, and 0% after the account's maximum 5 years period is expired.

Iceland

From 1 January 2011 the capital gains tax in Iceland is 20%. It was 18% prior to that (for a full year, in 2010), which in turn was a result of a progressive raises in the preceding couple years.

- 2008

- 10%

- 2009 (until 30 June)

- 10%

- 2009 (from 1 July)

- 15%

- 2010

- 18%

- 2011

- 20%

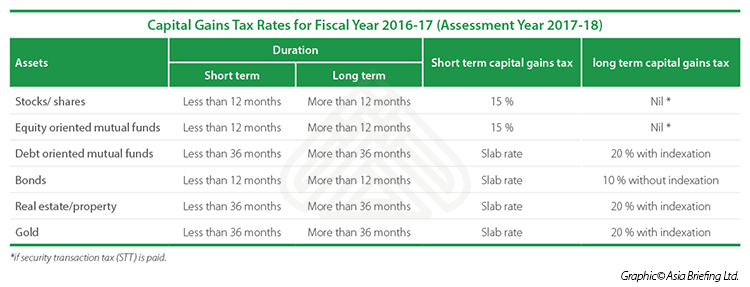

India

As of 2008, equities are considered long term capital if the holding period is one year or more. Long term capital gains from equities are not taxed as per section 10 (38) if shares are sold through recognized stock exchange and Securities Transaction Tax(STT) is paid on the sale.[12] STT in India is currently between 0.017% and 0.1% of total amount received on sale of securities through a recognized Indian stock exchange like the NSE or BSE. However short term capital gain from equities held for less than one year, is sold through recognised stock exchange and STT paid should not be considered and it is taxable at a flat rate of 15% u/s 111A and other surcharges, educational cess are imposed.[13] (w.e.f. 1 April 2009.[14])

Many other capital investments (house, buildings, real estate, bank deposits) are considered long term if the holding period is 3 or more years and are taxed @ 20% u/s 112.[15]

Capital Gains Tax Rates for Fiscal Year 2016-17 (Assessment Year 2017-18) [16]

| Assets | Duration (Short Term) | Duration (Long Term) | Short Term Capital Gains Tax | Long Term Capital Gains Tax |

|---|---|---|---|---|

| Stocks/shares | Less than 12 months | More than 12 months | 15% | Nil * |

| Equity oriented mutual funds | Less than 12 months | More than 12 months | 15% | Nil * |

| Debt oriented mutual funds | Less than 36 months | More than 36 months | Slab rate | 20% with indexation |

| Bonds | Less than 12 months | More than 12 months | Slab rate | 10% without indexation |

| Real estate/property | Less than 36 months | More than 36 months | Slab rate | 20% with indexation |

| Gold | Less than 36 months | More than 36 months | Slab rate | 20% with indexation |

Ireland, Republic of

Since 5 December 2012, there is a 33% tax on capital gains,[17] with several exclusions and deductions (e.g. agricultural land, primary residence, transfers between spouses). Gains made where the asset was originally purchased before 2003 attract indexation relief (the cost of the asset can be multiplied by a published factor to reflect inflation). Costs of purchase and sale are deductible, and every person has an exempt band of €1,270 per year.

The tax rate is 23% on certain investment policies, and rises to 40% on certain offshore gains when they are not declared in time.

Tax on capital gains arising in the first eleven months of the year must be paid by 15 December, and tax on capital gains arising in the last month of the year must be paid by the following 31 January.

Isle of Man

There is no capital gains tax.

Israel

Capital gains tax in Israel is set to 25% on the real gains made in non inflation indexed bonds, (Or 20% for a substantial shareholder) 25% on any other capital gains. (Or 30% for a substantial shareholder)[18]

Italy

Capital gains tax of corporate income tax 27.5% (IRES) on gains derived from disposals of participations and extraordinary capital gains. For individuals (IRPEF), capital gains shall incur a 26% tax.

Jamaica

There are no capital gains taxes in Jamaica.[19]

Japan

In Japan, there were two options for paying tax on capital gains from the sale of listed stocks. The first, Withholding Tax (源泉課税), taxed all proceeds (regardless of profit or loss) at 1.05%. The second method, declaring proceeds as "taxable income" (申告所得), required individuals to declare 26% of proceeds on their income tax statement. Many traders in Japan used both systems, declaring profits on the Withholding Tax system and losses as taxable income, minimizing the amount of income tax paid.

In 2003, Japan scrapped the system above in favor of a flat 20% tax on gains, though the rate was temporarily halved at 10% and after being postponed a few times the return to the normal rate of 20% is now set for 2014. Losses can be carried forward for 3 years. Starting in 2009, losses can alternatively be deducted from dividend income declared as "Separate Income" since the tax rate on both categories is equal (i.e., 20% temporarily halved to 10%). Aggregating profits and dividends to reach a single figure taxed at the same rate is fairly innovative.

Kenya

Capital gains taxes were abolished in Kenya in 1985 in order to spur growth in the securities and property market. The Kenyan Parliament passed a motion in August 2014 to reintroduce capital gains tax in January 2015[20] and "is expected to increase the cost of land transaction as investors pass on the cost to buyers. The tax will also affect those investing in shares and debt in the capital markets."[21] The capital gains tax came into effect on 1 January 2015 with 5% as the general applicable tax rate.[22]

Latvia

As of 1 January 2013 the capital gains made on the disposal of shares are exempt from the corporate income tax. If loss is incurred upon sale, it will not be deductible. To apply exemption, there are no restrictions on minimal holding period or shareholding. The exemption, however, does not apply on gain from sale of shares in entities located in the black-listed tax haven countries. The latter gains are subject to regular corporate income tax rate at 15%. [23]

Similarly, gains on disposal of securities quoted on the regulated markets of the EU or EEA countries and investment certificates in EU and EEA open-end investment funds are exempt from taxation in Latvia.

Gains on the disposal of other investments (like real estate properties) are taxed at regular corporate income tax rate of 15%.

The inbound dividends are not taxed in the hands of Latvian company (except, the dividends received from the low-tax jurisdiction). The outbound dividends are no subject to any taxes, except the dividends payable to the low-tax jurisdiction (15%).

In the hands of individuals the capital gains are taxed at 15%, the dividends – 10%.

Lithuania

Capital gains tax from the disposal of securities and from sale of real estate is 15%. Gains from the disposal of securities are exempt if they are acquired more than 366 days before their sale and the individual owns not more than 10% of securities for three years preceding the tax year during which the securities are sold. Gains from sale of real estate are exempt if the property is owned for more than 3 years before sale. These tax exemptions will cease to be valid on 1 January 2014 for annual gains of over 10,000 LTL.

Malaysia

There is no capital gains tax for equities in Malaysia. Malaysia used to have a capital gains tax on real estate but the tax was repealed in April 2007. However, a real property gains tax (RPGT) introduced in 2010 now applies to property sold less than six years from its purchase. Property disposed off less than three years after purchase will incur RGPT of 30% while those sold in its four and fifth year after will incur 20% and 15% RPGT, respectively. As for non-citizens, RPGT is imposed at 30% on the gains from properties disposed within the holding period of up to sixth year. And for disposal made in sixth and subsequent years, 5% RPGT is imposed for non-citizens, while companies and foreign property buyers are taxed at 5%.[24]

Malaysia has imposed capital gain tax on share options and share purchase plan received by employee starting year 2007.

For who does trading professionally (buying and selling securities frequently to obtain an income for living) as "traders", this will be considered income subject to personal income tax rates.

Mexico

There is no current Capital Gains Tax for profits in the stock market, it will be introduced in 2014 at 10% rate in Mexico.

Moldova

Under the Moldovan Tax Code a capital gain is defined as the difference between the acquisition and the disposition price of the capital asset. Only this difference (i.e. the gain) is taxable. The applicable rate is half (1/2) of the income tax rate, which for individuals is 18% and for companies was 15% (but in 2008 is 0%). Therefore, in 2008 the capital gain tax rate is 9% for individuals and 0% for companies.

Not all types of assets are "capital assets". Capital assets include: real estate; shares; stakes in limited liability companies etc.

Netherlands

Capital gains generally are exempt from tax. However, exceptions apply to the following assets: • Capital gains realised on the disposal of business assets (including real estate) and on the disposal of other assets that qualify as income from independently performed activities • Capital gains on liquidation of a company • Capital gains derived from the sale of a substantial interest in a company (that is, 5% of the issued share capital)[25]

Taxable income under Box 2 category includes dividends and capital gains from a substantial shareholding. (inkomsten uit aanmerkelijk belang) (i.e. a shareholding of at least 5%) Income that falls into the Box 2 category is taxed at a flat rate of 25%.[26]

Box 3: taxable income from savings and investments (viz. real estate) However a "theoretical capital yield" of 4% is taxed at a rate of 30% (so 1.2%) but only if the savings plus stocks of a person exceed a certain threshold (around 20.000 euros a person).[27]

In general an individual will not have to pay tax on capital gains. So if the main residence is sold or shares are sold the profit is not taxable. This is different if the transaction(s) exceed(s) normal asset management. In that case the capital gain is treated as income from other activities or even business income.

Relevant are: the number of transactions -> the more transactions the sooner it is assumed that activities exceed normal asset management specific knowledge of the individual -> if the individual is a professional trader, the personal transactions will be seen as taxable income sooner than if the individual doesn‘t have specific knowledge or experience. work which is invested in the asset -> if maintenance of a property is taken care of by an external party the activitities may be seen as normal asset management, if the owner does all the maintenance himself and even the renovations the tax authorities will argue that this is no longer normal asset management.

So it depends on the actual facts and circumstances how the capital gain is treated. Even judges do not always decide the same. [28]

New Zealand

New Zealand has no capital gains tax, however income tax may be charged on profits from the sale of personal property and land that was acquired for the purposes of resale.[29] This tax is widely avoided and not usually enforced, perhaps due to the difficulty in proving intent at the time of purchase. However, there have been a few cases of the IRD enforcing the law; in 2004 the government gathered $106.6 million checking on property sales from Queenstown, Wanaka and some areas of Auckland.[30]

New Zealand capital gains tax applies to foreign debt and equity investments.

In a speech delivered on 3 June 2009, then New Zealand Treasury Secretary John Whitehead called for a capital gains tax to be included in reforms to New Zealand's taxation system.[31] The introduction of a capital gains tax was proposed by the Labour Party as an election campaign strategy in the 2011 and 2014 general elections.[32][33]

On 17 May 2015, the governing National Party announced it would tighten rules for taxing profits on the sale of property. From 1 October 2015, any person selling a residential property within two years of purchase would be taxed on the profits at their marginal income tax rate. The seller's main home would be exempt, as well as properties inherited from deceased estates or transferred as part of a relationship settlement. To help enforcement, all buyers would need to supply their IRD number at settlement.[34][35]

Norway

The individual capital gains tax in Norway is 27%. In most cases, there is no capital gains tax on profits from sale of your principal home. This tax was introduced in 2006 through a reform that eliminated the "RISK-system", which intended to avoid the double taxation of capital. The new shareholder model, introduced in 2006, aims to reduce the difference in taxation of capital and labor by taxing dividends beyond a certain level as ordinary income. This means that focus was moved from capital to individuals and their level of income. This system also introduced a deductible allowance equal to the share's acquisition value times the average rate for Treasury bills with a 3-month period adjusted for tax. Shielding interest shall secure financial neutrality in that it returns the taxpayer what he or she alternatively would have achieved in a safe, passive capital placement exempt from additional taxation. The main purpose of the allowance is to prevent adverse shifts in investment and corporate financing structure as a result of the dividend tax. According to the papers explaining the new policy, a dividend tax without such shielding could push up the pressures on the rate of return on equity investments and lead Norwegian investors from equities to bonds, property etc.

Philippines

There is a 6% Capital Gains Tax and a 1.5% Documentary Stamps on the disposal of real estate in the Philippines. While the Capital Gain Tax is imposed on the gains presumed to have been realized by the seller from the sale, exchange, or other disposition of capital assets located in the Philippines, including other forms of conditional sale, the Documentary Stamp Tax is imposed on documents, instruments, loan agreements and papers evidencing the acceptance, assignment, sale or transfer of an obligation, rights, or property incident thereto. These two taxes are imposed on the actual price the property has been sold, or on its current Market Value, or on its Zonal Value whichever is higher. Zonal valuation in the Philippines is set by its tax collecting agency, the Bureau of Internal Revenue. Most often, real estate transactions in the Philippines are being sealed higher than their corresponding Market and Zonal values. As a standard process, the Capital Gain Tax is paid for by the seller, while the Documentary Stamp is paid for by the buyer. However, either of the two parties may pay both taxes depending on the agreement they entered into.

Tax Rates:[36]

For real property

- 6%, higher of fair market value (zonal or assessed value) and selling price

For Shares of Stocks Not Traded in the Stock Exchange

- Not over P100,000 - 5%

- Any amount in excess of P100,000 - 10%

Poland

Since 2004 there is one flat tax rate (19%) on capital income. It includes: selling stocks, bonds, mutual funds shares and also interests from bank deposits.

Portugal

There is a capital gains tax on sale of home and property. Any capital gain (mais-valia) arising is taxable as income. For residents this is on a sliding scale from 12 to 40%. However, for residents the taxable gain is reduced by 50%. Proven costs that have increased the value during the last five years can be deducted. For non-residents, the capital gain is taxed at a uniform rate of 25%. The capital gain which arises on the sale of own homes or residences, which are the elected main residence of the taxpayer or his family, is tax free if the total profit on sale is reinvested in the acquisition of another home, own residence or building plot in Portugal.

In 1986 and 1987 Portuguese corporations changed their capital structure by increasing the weight of equity capital. This was particularly notorious on quoted companies. In these two years, the government set up a large number of tax incentives to promote equity capital and to encourage the quotation on the Lisbon Stock Exchange. Until 2010, for stock held for more than twelve months the capital gain was exempt. The capital gain of stock held for shorter periods of time was taxable on 10%.

From 2010 onwards, for residents, all capital gain of stock above €500 is taxable on 20%. Investment funds, banks and corporations are exempted of capital gain tax over stock.

As of 2013, it is 28%.

Romania

In Romania there is a 16% flat tax plus 5.5% health insurance from capital gains. Next year the health insurance will increase to 8.9%. It also applies for real estate transactions but only if the property is sold less than three years from the date it was acquired.[37]

Russia

There is no separate tax on capital gains; rather, gains or gross receipt from sale of assets are absorbed into income tax base. Taxation of individual and corporate taxpayers is distinctly different:

- Capital gains of individual taxpayers are tax free if the taxpayer owned the asset for at least three years. If not, gains on sales of real estate and securities are absorbed into their personal income tax base and taxed at 13% (residents) and 30% (non-residents). A tax resident is any individual residing in the Russian Federation for more than 183 days in the past year.

- Capital gains of resident corporate taxpayers operating under general tax framework are taxed as ordinary business profits at the common rate of 20%, regardless of the ownership period. Small businesses operating under simplified tax framework pay tax not on capital gains, but on gross receipts at 6% or 15%.

- Dividends that may be included into gains on disposal of securities are taxed at source at 13% (residents) and 15% (non-residents) for either corporate or individual taxpayers.

Serbia

Capital gains are subject to a 15% tax for residents and 20% for nonresidents (based on the tax assessment).[38]

Sierra Leone

There is no capital gains tax in Sierra Leone.

Singapore

There is no capital gains tax in Singapore. For professional traders and who trade frequently, the profit is considered a sourced income in Singapore and subject to tax.

Slovakia

Individuals pay 19% or 25% capital gains tax. In addition, as a world rarity, they are also required to pay 14% health insurance from capital gains.

South Africa

For legal persons in South Africa, 80% of their net profit will attract CGT and for natural persons 40%. This portion of the net gain will be taxed at their marginal tax rate. As an effective tax rate this means a maximum effective rate of 16.4% (41% maximum marginal tax rate) for individuals is payable, and for corporate taxpayers a maximum of 22.4%. The annual individual and special trust exemption is R40 000.

South Korea

For individuals holding less than 3% of listed company, there is only 0.3% trade tax for sales of shares. Exchange traded funds are exempt from any trade tax. For larger than 3% shareholders of listed companies or for sales of shares in any unlisted company, capital gains tax in South Korea is 11% for tax residents for sales of shares in small- and medium-sized companies. Rates of 22% and 33% apply in certain other situations.[39] Those who have been resident in Korea for less than five years are exempt from capital gains tax on foreign assets.[40]

Spain

Spain's capital gains tax from 1 January 2016

Individuals: All capital gains taxed at maximum 23%

Companies: Capital gains taxed like any other income gain, at maximum 25%

Sri Lanka

Currently there is no capital gains tax in Sri Lanka.

Sweden

The capital gains tax in Sweden is up to 30% on realized capital income, depending on the depot type. Traditionally, the capital gains tax in Sweden has been 30%.

Switzerland

There is no capital gains tax in Switzerland for natural persons on trades of securities.

An exception are persons considered to be "professional traders", which are treated as self-employed persons for tax purposes: capital gains are taxed as company income, taxed at corporate rates, and additionally social contributions (AHV, currently at 10.25% rate) must be paid on the income. However such a status is rather infrequent, the decision is made on a case by case basis by the tax authorities. A set of safe heaven criteria were formulated in 2012 which guarantee a negative status:[41]

- holding each security for at least 6 months,

- low trading volume: sum of buying prices and sale proceeds is less than 500% of capital at the beginning of the year,

- realized capital gains make up less than 50% of income during the tax year,

- no use of foreign capital, or the interest paid on it is less than the dividend income,

- derivatives (especially options) are used solely to safeguard own portfolio risk.

For companies, capital gains are taxed as ordinary income at corporate rates.

Real estate

Capitals gains tax is levied on the sale of real estate property in all cantons. Taxation rules vary significantly by canton.[42]

For natural persons, the tax generally follows a separate progression from income taxes, diminishes with number of years held, and often can be postponed in cases like inheritance or for buying a replacement home. The tax is levied by canton or municipality only, there is no tax at the federal level. However, natural persons involved in real estate trading in a professional manner, may get treated as self-employed and taxed at higher rates similarly to a company and, additionally, social contributions would then need to be paid.[43]

For companies, capital gains are taxed as ordinary income at the federal level, and at the cantonal and municipal level, depending on the canton, either as ordinary income or at a special lower tax progression, like for natural persons.

Taiwan

No tax is collected from individual investors whose annual transactions are below T$1 billion ($33 million). Transactions above T$1 billion will be charged with a 0.1 percent tax.

Thailand

There is no separate capital gains tax in Thailand. If capital gains arise outside of Thailand it is not taxable. All earned income in Thailand from capital gains is taxed the same as regular income. However, if individual earns capital gain from security in the Stock Exchange of Thailand, it is exempted from personal income tax.

Turkey

Capital gains tax rate on share certificates for residents is 0% as of 2013 for two years of holding period.[44]

United Kingdom

History

Channon observes that one of the primary drivers to the introduction of CGT in the UK was the rapid growth in property values post World War II. This led to property developers deliberately leaving office blocks empty so that a rental income could not be established and greater capital gains made.[45] The capital gains tax system was therefore introduced by chancellor James Callaghan in 1965[46]

Basics

Individuals who are residents or ordinarily residents in the United Kingdom (and trustees of various trusts) are subject to an 18% capital gains tax.

For people paying more than the basic rate of income tax, this increased to 28% from 23 June 2010.

There are exceptions such as for principal private residences, holdings in ISAs or gilts. Certain other gains are allowed to be rolled over upon re-investment. Investments in some start up enterprises are also exempt from CGT. Entrepreneurs' relief allows a lower rate of CGT (10%) to be paid by people who have been involved for a year with a trading company and have a 5% or more shareholding.

Shares in companies with trading properties are eligible for entrepreneurs' relief, but not investment properties.[47]

Every individual has an annual capital gains tax allowance: gains below the allowance are exempt from tax, and capital losses can be set against capital gains in other holdings before taxation. All individuals are exempt from tax up to a specified amount of capital gains per year. For the 2015/16 tax year this "annual exemption" is £11,100.[48]

Corporate notes

Companies are subject to corporation tax on their "chargeable gains" (the amounts of which are calculated along the lines of capital gains tax in the United Kingdom). Companies cannot claim taper relief, but can claim an indexation allowance to offset the effect of inflation. A corporate substantial shareholdings exemption was introduced on 1 April 2002 for holdings of 10% or more of the shares in another company (30% or more for shares held by a life assurance company's long-term insurance fund). This is effectively a form of UK participation exemption. Almost all of the corporation tax raised on chargeable gains is paid by life assurance companies taxed on the I minus E basis.

The rules governing the taxation of capital gains in the United Kingdom for individuals and companies are contained in the Taxation of Chargeable Gains Act 1992.

Background to changes to 18% rate

In the Chancellor's October 2007 Autumn Statement, draft proposals were announced that would change the applicable rates of CGT as of 6 April 2008. Under these proposals, an individual's annual exemption will continue but taper relief will cease and a single rate of capital gains tax at 18% will be applied to chargeable gains. This new single rate would replace the individual's marginal (Income Tax) rate of tax for CGT purposes. The changes were introduced, at least in part, because the UK government felt that private equity firms were making excessive profits by benefiting from overly generous taper relief on business assets.

The changes were criticised by a number of groups including the Federation of Small Businesses, who claimed that the new rules would increase the CGT liability of small businesses and discourage entrepreneurship in the UK.[49] At the time of the proposals there was concern that the changes would lead to a bulk selling of assets just before the start of the 2008–09 tax year to benefit from existing taper relief. Capital Gains Tax rose to 28% on 23 June 2010 at 00:00.

Historical

Individuals paid capital gains tax at their highest marginal rate of income tax (0%, 10%, 20% or 40% in the tax year 2007/8) but from 6 April 1998 were able to claim a taper relief which reduces the amount of a gain that is subject to capital gains tax (reducing the effective rate of tax), depending on whether the asset is a "business asset" or a "non-business asset" and the length of the period of ownership. Taper relief provided up to a 75% reduction (leaving 25% taxable) in taxable gains for business assets, and 40% (leaving 60% taxable), for non-business assets, for an individual.[50] Taper relief replaces indexation allowance for individuals, which can still be claimed for assets held prior to 6 April 1998 from the date of purchase until that date, but was itself abolished on 5 April 2008.

United States

In the United States, with certain exceptions, individuals and corporations pay income tax on the net total of all their capital gains. Short-term capital gains are taxed at a higher rate: the ordinary income tax rate. The tax rate for individuals on "long-term capital gains", which are gains on assets that have been held for over one year before being sold, is lower than the ordinary income tax rate, and in some tax brackets there is no tax due on such gains.

The tax rate on long-term gains was reduced in 1997 via the Taxpayer Relief Act of 1997 from 28% to 20% and again in 2003, via the Jobs and Growth Tax Relief Reconciliation Act of 2003, from 20% to 15% for individuals whose highest tax bracket is 15% or more, or from 10% to 5% for individuals in the lowest two income tax brackets (whose highest tax bracket is less than 15%). (See progressive tax.) The reduced 15% tax rate on eligible dividends and capital gains, previously scheduled to expire in 2008, was extended through 2010 as a result of the Tax Increase Prevention and Reconciliation Act signed into law by President Bush on 17 May 2006, which also reduced the 5% rate to 0%.[51] Toward the end of 2010, President Obama signed a law extending the reduced rate on eligible dividends until the end of 2012.

The law allows for individuals to defer capital gains taxes with tax planning strategies such as the structured sale (ensured installment sale), charitable trust (CRT), installment sale, private annuity trust, and a 1031 exchange. The United States, unlike almost all other countries, taxes its citizens (with some exceptions [52]) on their worldwide income no matter where in the world they reside. U.S. citizens therefore find it difficult to take advantage of personal tax havens. Although there are some offshore bank accounts that advertise as tax havens, U.S. law requires reporting of income from those accounts, and willful failure to do so constitutes tax evasion.

Deferring or reducing capital gains tax

Taxpayers may defer capital gains taxes by simply deferring the sale of the asset. In addition, depending on the specifics of national tax law, taxpayers may be able to defer, reduce, or avoid capital gains taxes using the following strategies:

- A nation may tax at a lower rate the gains on investments in favored industries or sectors, such as small business.

- There may be accounts with tax-favored status. The most advantageous let gains accumulate in the account without taxes; taxes are paid only when the taxpayer withdraws funds from the account.

- Selling an asset at a loss may create a "tax loss" that can be applied to offset gains realized in the future, and avoid or reduce taxes on those gains. Tax losses are a business asset, but the business must avoid "sham" transactions, such as selling to oneself or a subsidiary for no legitimate purpose other than to create a tax loss.

- Tax may be waived if the asset is given to a charity.

- Tax may be deferred if the taxpayer sells the asset but receives payment from the buyer over a period of years. However, the taxpayer bears the risk of a default by the buyer during that period. A structured sale or purchase of an annuity may be ways to defer taxes.

- In certain transactions, the basis (original cost) of the asset is changed. In the U.S., the basis for an inherited asset becomes its value at the time of the inheritance.

- Tax may be deferred if the seller of an asset puts the funds into the purchase of a "like-kind" asset. In the U.S., this is called a 1031 exchange and is now generally available only for business-related real estate and tangible property.

References

- ↑ https://www.bmf.gv.at/steuern/Besteuerung-inl-sowie-im-Inland-bez-Kapitalertraege.html

- ↑ "Invest in Belgium". economie.fgov.be. Archived from the original on 28 March 2008.

- ↑ "Securities and Exchange Commission of Brazil". CVM – Comissão de Valores Mobiliários (Brazilian SEC). Archived from the original on 10 April 2010.

- ↑ "CRA". cra-arc.gc.ca.

- ↑ "Various tax rates in Cyprus and information; Capital Gains in Cyprus". Investment-Gateway.eu. Retrieved 4 August 2013.

- ↑ "SKAT: Satser og belřbsgrćnser 2010+2011". Skat.dk. Archived from the original on 18 March 2012. Retrieved 9 February 2012.

- ↑ https://af.reuters.com/article/egyptNews/idAFL6N0OG28120140530

- ↑ "Tax Guide, Individuals 2015". vero.fi. 10 March 2014. Retrieved 22 April 2015.

- ↑ VERO Taxation of Stock Options Archived 14 May 2011 at the Wayback Machine.

- ↑ "VERO". vero.fi. Archived from the original on 3 August 2009.

- ↑ "How Share Awards and Share Options are Taxed". GovHK. Retrieved 9 February 2012.

- ↑ Capital Gain Tax on Share Trading

- ↑

- ↑ "ftn97section105.htm". Law.incometaxindia.gov.in. 4 January 2009. Archived from the original on 29 January 2012. Retrieved 9 February 2012.

- ↑ Indian Gov Capital Gains Tax Calculator Archived 16 April 2014 at the Wayback Machine.

- ↑ Rastogi, Vasundhara (June 6, 2017). "Capital Gains Tax in India: An Explainer". http://www.india-briefing.com. Retrieved June 13, 2017. External link in

|website=(help) - ↑ "Capital Gains Tax". Citizensinformation.ie. Retrieved 4 August 2013.

- ↑ Your taxes: Tax rates for 2014

- ↑ http://www.pwc.com/jm/en/business-in-jamaica/tax-system.jhtml

- ↑ "Capital Gains Tax: The Good, The Bad and The Ugly". http://abacus.co.ke/. Abacus. Retrieved 11 September 2014. External link in

|website=(help) - ↑ "Tax measures to boost growth but prices of goods will go up". Nation.co.ke.

- ↑ "Global Tax Alert: Kenya reintroduces capital gains tax - EYG no. CM4776". http://www.ey.com. Ernst & Young. 7 October 2014. Retrieved 12 January 2015. External link in

|website=(help) - ↑ http://taxwise.lv/useful-information/general-tax-facts-and-rates-in-latvia/

- ↑ ""Budget 2014 Highlights". 25 October 2013". Theedgemalaysia.com. 25 October 2013. Archived from the original on 26 October 2013. Retrieved 1 November 2013.

- ↑ "Archived copy" (PDF). Archived from the original (PDF) on 14 August 2015. Retrieved 1 May 2015.

- ↑ http://www.globalpropertyguide.com/Europe/Netherlands/Taxes-and-Costs

- ↑ https://www.tssolutions.nl/frequently-asked-questions/Dutch-tax.html

- ↑ http://www.expatax.nl/kb/article/tax-for-capital-gains-is-it-applicable-in-the-netherlands-and-if-so-in-which-situations-209.html#.VUNYBmSqiko

- ↑ "Buying and Selling Residential Property" (PDF). New Zealand Inland Revenue. Archived from the original (PDF) on 3 June 2013. Retrieved 4 August 2013.

- ↑ "Capital Gains Tax – Is this needed in New Zealand". National.org.nz. 22 March 2007

- ↑ Fallow, Brian (4 June 2009). "Treasury pushes for capital gains tax". The New Zealand Herald. Retrieved 23 September 2011.

- ↑ Adam Bennett (14 July 2011). "Labour unveils 'bold' tax plan". The New Zealand Herald. Retrieved 16 June 2012.

- ↑ "Own Our Future". New Zealand Labour Party. 14 July 2011.

- ↑ "Tighter rules on residential property investors and overseas buyers". Fairfax New Zealand. 17 May 2015. Retrieved 17 May 2015.

- ↑ Brockett, Matthew (17 May 2015). "New property tax and tighter rules for foreigners in New Zealand". Sydney Morning Herald. Retrieved 17 May 2015.

- ↑ http://www.bir.gov.ph/index.php/tax-information/capital-gains-tax.html

- ↑ Afaceri, Stiri. "Noul impozit pe tranzactiile imobiliare". Retrieved 13 July 2012.

- ↑ http://www.e-racuni.com

- ↑ "Summary of Korean Corporate and Individual Income Taxes 2007" (PDF). Samil Price Waterhouse Coopers. 2007. Retrieved 4 August 2013.

- ↑ "Korea : Publications : 2009 Korean Tax Summaries". Price Waterhouse Coopers. Retrieved 9 February 2012.

- ↑ https://www.estv.admin.ch/dam/estv/de/dokumente/bundessteuer/kreisschreiben/2004/1-036-D-2012.pdf.download.pdf/1-036-D-2012-d.pdf

- ↑ https://www.estv.admin.ch/dam/estv/de/dokumente/allgemein/Dokumentation/Publikationen/dossier_steuerinformationen/d/Die-Besteuerung-der-Grundstueckgewinne.pdf.download.pdf/Die-Besteuerung-der-Grundstueckgewinne_2015_d.pdf

- ↑ http://www.wengervieli.ch/getattachment/2b57d10e-d7ad-4255-af98-a68bf240561c/Steuerfreier-Kapitalgewinn.aspx

- ↑ "Basbakanlik.gov.tr". rega.basbakanlik.gov.tr.

- ↑ Channon, Derek F (1978). The Service Industries. London: The MacMillan Press Ltd. ISBN 0841950326.

- ↑ "Telegraph: Capital Gains Tax: a brief history". The Daily Telegraph. Retrieved 8 January 2014.

- ↑ "Residential property tax planning". MAH, Chartered Accountants. Retrieved 2013-11-08.

- ↑ "Capital Gains Tax allowances". gov.uk. Retrieved 6 April 2015.

- ↑ Jean Eaglesham and John Willman (23 January 2008). "Final showdown on CGT reforms". Financial Times. Retrieved 23 January 2008.

- ↑ "An Introduction to Capital Gains Tax" (PDF). HM Revenue and Customs. p. 94. Retrieved 22 April 2008.

- ↑ Public Law No. 109-222.

- ↑ An example of an exception is the exemption from U.S. federal income tax for a limited amount of foreign earned income of a citizen or resident of the United States who is living abroad, under26 U.S.C. § 911.

{kind=link}

Further reading

- Black, Stephen (2011). "A Capital Gains Anomaly: Commissioner v. Banks and the Proceeds from Lawsuits". St. Mary's Law Journal. 43: 113. SSRN 1858776

.

.

External links

- The Labyrinth of Capital Gains Tax Policy: A Guide for the Perplexed (1999), Brookings Institution