Variance decomposition of forecast errors

In econometrics and other applications of multivariate time series analysis, a variance decomposition or forecast error variance decomposition (FEVD) is used to aid in the interpretation of a vector autoregression (VAR) model once it has been fitted.[1] The variance decomposition indicates the amount of information each variable contributes to the other variables in the autoregression. It determines how much of the forecast error variance of each of the variables can be explained by exogenous shocks to the other variables.

Calculating the forecast error variance

For the VAR (p) of form

.

.

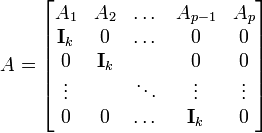

This can be changed to a VAR(1) structure by writing it in companion form (see general matrix notation of a VAR(p))

where

where

,

,  ,

,  and

and

where  ,

,  and

and  are

are  dimensional column vectors,

dimensional column vectors,  is

is  by dimensional matrix and

by dimensional matrix and  ,

,  and

and  are dimensional column vectors.

are dimensional column vectors.

The mean squared error of the h-step forecast of variable j is

![\mathbf{MSE}[y_{j,t}(h)]=\sum_{i=0}^{h-1}\sum_{k=1}^{K}(e_j'\Theta_ie_k)^2=\bigg(\sum_{i=0}^{h-1}\Theta_i\Theta_i'\bigg)_{jj}=\bigg(\sum_{i=0}^{h-1}\Phi_i\Sigma_u\Phi_i'\bigg)_{jj},](../I/m/67382e2c0806c172ae0ffc9a034aef23.png)

and where

is the jth column of

is the jth column of  and the subscript

and the subscript  refers to that element of the matrix

refers to that element of the matrix

where

where  is a lower triangular matrix obtained by a Cholesky decomposition of

is a lower triangular matrix obtained by a Cholesky decomposition of  such that

such that  , where is the covariance matrix of the errors

, where is the covariance matrix of the errors

-

where

where  so that

so that  is a by dimensional matrix.

is a by dimensional matrix.

-

The amount of forecast error variance of variable  accounted for by exogenous shocks to variable is given by

accounted for by exogenous shocks to variable is given by

![\omega_{jk,h}=\sum_{i=0}^{h-1}(e_j'\Theta_ie_k)^2/MSE[y_{j,t}(h)] .](../I/m/ac6eeacdc11b3cc5ec626d87dab90e08.png)

Notes

- ↑ Lütkepohl, H. (2007) New Introduction to Multiple Time Series Analysis, Springer. p. 63.