Theory of taxation

Several theories of taxation exist in public economics. Governments at all levels (national, regional and local) need to raise revenue from a variety of sources to finance public-sector expenditures. The details of taxation are guided by two principles: who will benefit, and who can pay.

In public-finance literature, there are two theories: the ability theory (presented by Arthur Cecil Pigou)[1] and the benefit theory (developed by Erik Lindahl).[2][3] The benefit theory has a modern version, known as the "voluntary exchange" theory.[4]

Under the benefit theory, tax levels are automatically determined, because taxpayers pay proportionately for the government benefits they receive. In other words, the individuals who benefit the most from public services pay the most taxes. In analyzing the benefit approach, two models have been discussed: the Lindahl model and the Bowen model.

Lindahl's model

Lindahl tries to solve three problems:

- Extent of state activity

- Allocation of the total expenditure among various goods and services

- Allocation of tax burden

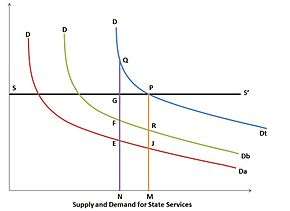

In the Lindahl model, if SS is the supply curve of state services it is assumed that production of social goods is linear and homogenous. DDa is the demand curve of taxpayer A, and DDb is the demand curve of taxpayer B. The vertical summation of the two demand curves results in the community’s total demand schedule for state services. A and B pay different proportions of the cost of the services. When ON is the amount of state services produced, A contributes NE and B contributes NF; the cost of supply is NG. Since the state is non-profit, it increases its supply to OM. At this level, A contributes MJ and B contributes MR (the total cost of supply). Equilibrium is reached at point P on a voluntary-exchange basis.

Bowen's model

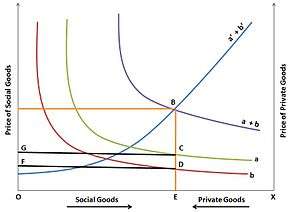

Bowen’s model has more operational significance, since it demonstrates that when social goods are produced under conditions of increasing costs, the opportunity cost of private goods is foregone. For example, if there is one social good and two taxpayers (A and B), their demand for social goods is represented by a and b; therefore, a+b is the total demand for social goods. The supply curve is shown by a'+b', indicating that goods are produced under conditions of increasing cost. The production cost of social goods is the value of foregone private goods; this means that a'+b' is also the demand curve of private goods. The intersection of the cost and demand curves at B determines how a given national income should (according to taxpayers' desires) be divided between social and private goods; hence, there should be OE social goods and EX private goods. Simultaneously, the tax shares of A and B are determined by their individual demand schedules. The total tax requirement is the area (ABEO) out of which A is willing to pay GCEO and B is willing to pay FDEO.

Advantages and limitations

The advantage of the benefit theory is the direct correlation between revenue and expenditure in a budget. It approximates market behaviour in the allocation procedures of the public sector. Although simple in its application, the benefit theory has difficulties:

- It limits the scope of government activities

- Government can neither support the poor nor take steps to stabilize the economy

- Applicable only when beneficiaries can be observed directly (impossible for most public services)

- Taxation in accord with the benefit principle would leave distribution of real incomes unchanged

Ability-to-pay approach

The ability-to-pay approach treats government revenue and expenditures separately. Taxes are based on taxpayers’ ability to pay; there is no quid pro quo. Taxes paid are seen as a sacrifice by taxpayers, which raises the issues of what the sacrifice of each taxpayer should be and how it should be measured:

- Equal sacrifice: The total loss of utility as a result of taxation should be equal for all taxpayers (the rich will be taxed more heavily than the poor)

- Equal proportional sacrifice: The proportional loss of utility as a result of taxation should be equal for all taxpayers

- Equal marginal sacrifice: The instantaneous loss of utility (as measured by the derivative of the utility function) as a result of taxation should be equal for all taxpayers. This will entail the least aggregate sacrifice (the total sacrifice will be the least)

The three types of sacrifices have been demonstrated by Richard Musgrave. In the ability-to-pay model illustrated, total utility is C and marginal utility is O. CE is total utility, and CF is the marginal utility of income. When an income-yielding tax (MG) is levied, under equal absolute sacrifice, A will pay NG and B will pay TH (TH+NG=MG). Under equal proportional sacrifice, A pays RG and B pays SH (SH+RG=MG). The shares are arranged so EW÷EI=KU÷KJ. Under equal marginal sacrifice, A pays VG and B pays VH (VG+VH=MG). The aggregate sacrifice (EX+KY) is at minimum.

Mathematically, the conditions are as follows:

- Equal absolute sacrifice=U(Y)-U(Y-T), where y=income and t=tax amount

- Equal proportional sacrifice=(U(Y)-U(Y-T))/U(Y), where U(Y)=total utility from y

- Equal marginal sacrifice=(dU(Y-T))/(d(Y-T))[5]

References

- ↑ Samuelson, Paul A. "Diagrammatic Exposition of a Theory of Public Extpenditure" (PDF). University of California, Santa Barbara. Retrieved August 27, 2012.

- ↑ "Erik Robert Lindahl". Encyclopædia Britannica. 1960-01-06. Retrieved 2012-08-27.

- ↑ "Theories of Taxation – Benefit Theory – Cost of Service Theory – Ability to Pay Theory – Proportionate Principle". Economicsconcepts.com. Retrieved 2012-08-27.

- ↑ Giersch, Thorsten (August 2007). "From Lindahl’s Garden to Global Warming: How Useful is the Lindahl Approach in the Context of Global Public Goods?" (PDF).

- ↑ Friedman, David D. (December 1999). "Price Theory: an intermediate text". South-Western Publishing Co. ISBN 978-0538805643. Archived from the original on November 23, 2012. Retrieved November 23, 2012.