Poll tax (United States)

In the United States, payment of a poll tax was a prerequisite to the registration for voting in a number of states. The tax emerged in some states of the United States in the late 19th century as part of the Jim Crow laws. After the right to vote was extended to all races by the enactment of the Fifteenth Amendment to the United States Constitution, a number of states enacted poll tax laws as a device for restricting voting rights. The laws often included a grandfather clause, which allowed any adult male whose father or grandfather had voted in a specific year prior to the abolition of slavery to vote without paying the tax. These laws, along with unfairly implemented literacy tests and extra-legal intimidation,[1] achieved the desired effect of disenfranchising African-American and Native American voters, as well as poor whites.

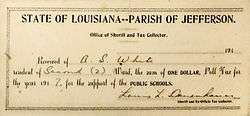

Proof of payment of a poll tax was a prerequisite to voter registration in Florida, Alabama, Tennessee, Arkansas, Louisiana, Mississippi, Georgia (1877), North and South Carolina, Virginia (until 1882 and again from 1902 with its new constitution),[2][3] and Texas (1902).[4] The Texas poll tax "required otherwise eligible voters to pay between $1.50 and $1.75 to register to vote – a lot of money at the time, and a big barrier to the working classes and poor."[4] Georgia created a cumulative poll tax requirement in 1877: men of any race 21 to 60 years of age had to pay a sum of money for every year from the time they had turned 21, or from the time that the law took effect.[5]

The poll tax requirements applied to whites as well as blacks, and also adversely affected poor citizens. The laws that allowed the poll tax did not specify a certain group of people.[6] This meant that white women could also be discriminated against when they went to vote. One example is in Alabama where white women were discriminated against and then organized to secure their right to vote. One group of women that did this was Women's Joint Legislative Council of Alabama (WJLC).[7] Discrimination on voting extended further than white women as well. African Americans and African American women faced discrimination as well.[8] African American women also organized in groups against being denied voting rights. One African American woman sued the county with the help of the NAACP. She sued for her right to vote as she was stopped from even registering to vote. As a result of her suing the county the mailman did not deliver her mail for quite some time.[8] Many states required payment of the tax at a time separate from the election, and then required voters to bring receipts with them to the polls. If they could not locate such receipts, they could not vote. In addition, many states surrounded registration and voting with complex record-keeping requirements.[9] These were particularly difficult for sharecropper and tenant farmers to comply with, as they moved frequently.

The poll tax was sometimes used alone or together with a literacy qualification. In a kind of grandfather clause, North Carolina in 1900 exempted from the poll tax those men entitled to vote as of January 1, 1867. This excluded all blacks, who did not then have suffrage.[10]

Although largely associated with states of the former Confederacy, poll taxes were also in place in some northern and western states. For instance, California had a poll tax until 1914 when it was abolished through a popular referendum.

Judicial challenge

In 1937, in Breedlove v. Suttles, 302 U.S. 277 (1937), the United States Supreme Court found that a prerequisite that poll taxes be paid for registration to vote was constitutional. The case involved the Georgia poll tax of $1. Georgia abolished its poll tax in 1945.[11]

The 24th Amendment, ratified in 1964, abolished the use of the poll tax (or any other tax) as a pre-condition for voting in federal elections,[12] but made no mention of poll taxes in state elections.

In the 1966 case of Harper v. Virginia Board of Elections, the Supreme Court overruled its decision in Breedlove v. Suttles, and extended the prohibition of poll taxes to state elections. It declared that the imposition of a poll tax in state elections violated the Equal Protection Clause of the 14th Amendment to the United States Constitution.

The Harper ruling was one of several that relied on the Equal Protection clause of the 14th Amendment rather than the more direct provision of the 15th Amendment. In a two-month period in the spring of 1966, Federal courts declared unconstitutional poll tax laws in the last four states that still had them, starting with Texas on 9 February. Decisions followed for Alabama (3 March) and Virginia (25 March). Mississippi's $2.00 poll tax (equal to $14.59 in 2013) was the last to fall, declared unconstitutional on 8 April 1966, by a federal panel.[13] Virginia attempted to partially abolish its poll tax by requiring a residence certification, but the Supreme Court rejected the arrangement in 1965 in Harman v. Forssenius.

References

- ↑ http://www.crmvet.org/info/lithome.htm

- ↑ "Virginia's Constitutional Convention of 1901–1902". Virginia Historical Society. Retrieved 2006-09-14.

- ↑ Dabney, Virginius (1971). Virginia, The New Dominion. University Press of Virginia. pp. 436–437. ISBN 0-8139-1015-3.

- 1 2 "Historical Barriers to Voting", in Texas Politics, University of Texas, accessed 4 November 2012.

- ↑ "Atlanta in the Civil Rights Movement", Atlanta Regional Council for Higher Education

- ↑ Wilkerson-Freeman, Sarah. The Second Battle for Woman Suffrage: Alabama White Women, the Poll Tax, and V. O. Key's Master Narrative of Southern Politics, The Journal of Southern History Vol. 68, No. 2 (May, 2002), pp. 333-374.

- ↑ Wilkerson-Freeman, Sarah. The Second Battle for Woman Suffrage: Alabama White Women, the Poll Tax, and V. O. Key's Master Narrative of Southern Politics, The Journal of Southern History Vol. 68, No. 2 (May, 2002), p 351.

- 1 2 Jones-Branch, Cherisse. "To Speak When and Where I Can": African American Women’s Political Activism in South Carolina in the 1940’s and 1950’s. The South Carolina Historical Magazine, Vol. 107, No. 3 (Jul., 2006.) pp. 204-224.

- ↑ Andrews, E. Benjamin (1912). History of the United States. New York: Charles Scribner's Sons.

- ↑ Richard H. Pildes, "Democracy, Anti-Democracy, and the Canon", 2000, pp.12 and 27 Accessed 10 Mar 2008

- ↑ Novotny, Patrick (2007). This Georgia Rising: Education, Civil Rights, and the Politics of Change in Georgia in The 1940s. Mercer University Press. pp. 150–. ISBN 9780881460889. Retrieved 6 January 2013.

- ↑ Jillson, Cal (2011-02-22). Texas Politics: Governing the Lone Star State. Taylor & Francis. pp. 38–. ISBN 9780415890601. Retrieved 6 January 2013.

- ↑ The World Almanac 1966, p. 68

| ||||||||||||||||||||||||||||||||||||