Minimum mean square error

In statistics and signal processing, a minimum mean square error (MMSE) estimator is an estimation method which minimizes the mean square error (MSE), which is a common measure of estimator quality, of the fitted values of a dependent variable. In the Bayesian setting, the term MMSE more specifically refers to estimation with quadratic cost function. In such case, the MMSE estimator is given by the posterior mean of the parameter to be estimated. Since the posterior mean is cumbersome to calculate, the form of the MMSE estimator is usually constrained to be within a certain class of functions. Linear MMSE estimators are a popular choice since they are easy to use, calculate, and very versatile. It has given rise to many popular estimators such as the Wiener-Kolmogorov filter and Kalman filter.

Motivation

The term MMSE more specifically refers to estimation in a Bayesian setting with quadratic cost function. The basic idea behind the Bayesian approach to estimation stems from practical situations where we often have some prior information about the parameter to be estimated. For instance, we may have prior information about the range that the parameter can assume; or we may have an old estimate of the parameter that we want to modify when a new observation is made available; or the statistics of an actual random signal such as speech. This is in contrast to the non-Bayesian approach like minimum-variance unbiased estimator (MVUE) where absolutely nothing is assumed to be known about the parameter in advance and which does not account for such situations. In the Bayesian approach, such prior information is captured by the prior probability density function of the parameters; and based directly on Bayes theorem, it allows us to make better posterior estimates as more observations become available. Thus unlike non-Bayesian approach where parameters of interest are assumed to be deterministic, but unknown constants, the Bayesian estimator seeks to estimate a parameter that is itself a random variable. Furthermore, Bayesian estimation can also deal with situations where the sequence of observations are not necessarily independent. Thus Bayesian estimation provides yet another alternative to the MVUE. This is useful when the MVUE does not exist or cannot be found.

Definition

Let  be a

be a  hidden random vector variable, and let

hidden random vector variable, and let  be a

be a  known random vector variable (the measurement or observation), both of them not necessarily of the same dimension. An estimator

known random vector variable (the measurement or observation), both of them not necessarily of the same dimension. An estimator  of is any function of the measurement . The estimation error vector is given by

of is any function of the measurement . The estimation error vector is given by  and its mean squared error (MSE) is given by the trace of error covariance matrix

and its mean squared error (MSE) is given by the trace of error covariance matrix

,

,

where the expectation  is taken over both and . When is a scalar variable, the MSE expression simplifies to

is taken over both and . When is a scalar variable, the MSE expression simplifies to  . Note that MSE can equivalently be defined in other ways, since

. Note that MSE can equivalently be defined in other ways, since

The MMSE estimator is then defined as the estimator achieving minimal MSE:

Properties

- Under some weak regularity assumptions,[1] the MMSE estimator is uniquely defined, and is given by

- In other words, the MMSE estimator is the conditional expectation of given the known observed value of the measurements.

- The MMSE estimator is unbiased (under the regularity assumptions mentioned above):

- The MMSE estimator is asymptotically unbiased and it converges in distribution to the normal distribution:

- where

is the Fisher information of . Thus, the MMSE estimator is asymptotically efficient.

is the Fisher information of . Thus, the MMSE estimator is asymptotically efficient.

- The orthogonality principle: When is a scalar, an estimator constrained to be of certain form

is an optimal estimator, i.e.

is an optimal estimator, i.e.  if and only if

if and only if

- for all

in closed, linear subspace

in closed, linear subspace  of the measurements. For random vectors, since the MSE for estimation of a random vector is the sum of the MSEs of the coordinates, finding the MMSE estimator of a random vector decomposes into finding the MMSE estimators of the coordinates of X separately:

of the measurements. For random vectors, since the MSE for estimation of a random vector is the sum of the MSEs of the coordinates, finding the MMSE estimator of a random vector decomposes into finding the MMSE estimators of the coordinates of X separately:

- for all i and j. More succinctly put, the cross-correlation between the minimum estimation error

and the estimator

and the estimator  should be zero,

should be zero,

- If and are jointly Gaussian, then the MMSE estimator is linear, i.e., it has the form

for matrix

for matrix  and constant

and constant  . This can be directly shown using the Bayes theorem. As a consequence, to find the MMSE estimator, it is sufficient to find the linear MMSE estimator.

. This can be directly shown using the Bayes theorem. As a consequence, to find the MMSE estimator, it is sufficient to find the linear MMSE estimator.

Linear MMSE estimator

In many cases, it is not possible to determine the analytical expression of the MMSE estimator. Two basic numerical approaches to obtain the MMSE estimate depends on either finding the conditional expectation  or finding the minima of MSE. Direct numerical evaluation of the conditional expectation is computationally expensive, since they often require multidimensional integration usually done via Monte Carlo methods. Another computational approach is to directly seek the minima of the MSE using techniques such as the gradient descent methods; but this method still requires the evaluation of expectation. While these numerical methods have been fruitful, a closed form expression for the MMSE estimator is nevertheless possible if we are willing to make some compromises.

or finding the minima of MSE. Direct numerical evaluation of the conditional expectation is computationally expensive, since they often require multidimensional integration usually done via Monte Carlo methods. Another computational approach is to directly seek the minima of the MSE using techniques such as the gradient descent methods; but this method still requires the evaluation of expectation. While these numerical methods have been fruitful, a closed form expression for the MMSE estimator is nevertheless possible if we are willing to make some compromises.

One possibility is to abandon the full optimality requirements and seek a technique minimizing the MSE within a particular class of estimators, such as the class of linear estimators. Thus we postulate that the conditional expectation of given is a simple linear function of ,  , where the measurement is a random vector, is a matrix and is a vector. This can be seen as the first order Taylor approximation of . The linear MMSE estimator is the estimator achieving minimum MSE among all estimators of such form. That is, it solves the following the optimization problem:

, where the measurement is a random vector, is a matrix and is a vector. This can be seen as the first order Taylor approximation of . The linear MMSE estimator is the estimator achieving minimum MSE among all estimators of such form. That is, it solves the following the optimization problem:

One advantage of such linear MMSE estimator is that it is not necessary to explicitly calculate the posterior probability density function of . Such linear estimator only depends on the first two moments of and . So although it may be convenient to assume that and are jointly Gaussian, it is not necessary to make this assumption, so long as the assumed distribution has well defined first and second moments. The form of the linear estimator does not depend on the type of the assumed underlying distribution.

The expression for optimal and is given by

where  ,

,  the

the  is cross-covariance matrix between and , the

is cross-covariance matrix between and , the  is auto-covariance matrix of .

is auto-covariance matrix of .

Thus the expression for linear MMSE estimator, its mean, and its auto-covariance is given by

where the  is cross-covariance matrix between and .

is cross-covariance matrix between and .

Lastly, the error covariance and minimum mean square error achievable by such estimator is

For the special case when both and are scalars, the above relations simplify to

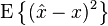

Let us have the optimal linear MMSE estimator given as  , where we are required to find the expression for and . It is required that the MMSE estimator be unbiased. This means,

, where we are required to find the expression for and . It is required that the MMSE estimator be unbiased. This means,

Plugging the expression for in above, we get

where and  . Thus we can re-write the estimator as

. Thus we can re-write the estimator as

and the expression for estimation error becomes

From the orthogonality principle, we can have  , where we take

, where we take  . Here the left hand side term is

. Here the left hand side term is

When equated to zero, we obtain the desired expression for as

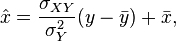

The is cross-covariance matrix between X and Y, and is auto-covariance matrix of Y. Since  , the expression can also be re-written in terms of as

, the expression can also be re-written in terms of as

Thus the full expression for the linear MMSE estimator is

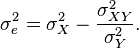

Since the estimate is itself a random variable with  , we can also obtain its auto-covariance as

, we can also obtain its auto-covariance as

Putting the expression for and  , we get

, we get

Lastly, the covariance of linear MMSE estimation error will then be given by

The first term in the third line is zero due to the orthogonality principle. Since  , we can re-write

, we can re-write  in terms of covariance matrices as

in terms of covariance matrices as

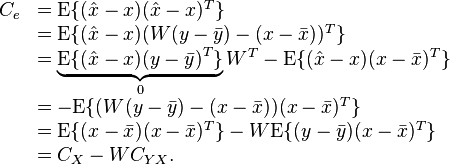

This we can recognize to be the same as  Thus the minimum mean square error achievable by such a linear estimator is

Thus the minimum mean square error achievable by such a linear estimator is

.

.

Calculation

Standard method like Gauss elimination can be used to solve the matrix equation for . A more numerically stable method is provided by QR decomposition method. Since the matrix  is a symmetric positive definite matrix, can be solved twice as fast with the Cholesky decomposition, while for large sparse systems conjugate gradient method is more effective. Levinson recursion is a fast method when is also a Toeplitz matrix. This can happen when is a wide sense stationary process. In such stationary cases, these estimators are also referred to as Wiener-Kolmogorov filters.

is a symmetric positive definite matrix, can be solved twice as fast with the Cholesky decomposition, while for large sparse systems conjugate gradient method is more effective. Levinson recursion is a fast method when is also a Toeplitz matrix. This can happen when is a wide sense stationary process. In such stationary cases, these estimators are also referred to as Wiener-Kolmogorov filters.

Linear MMSE estimator for linear observation process

Let us further model the underlying process of observation as a linear process:  , where

, where  is a known matrix and

is a known matrix and  is random noise vector with the mean

is random noise vector with the mean  and cross-covariance

and cross-covariance  . Here the required mean and the covariance matrices will be

. Here the required mean and the covariance matrices will be

Thus the expression for the linear MMSE estimator matrix further modifies to

Putting everything into the expression for , we get

Lastly, the error covariance is

The significant difference between the estimation problem treated above and those of least squares and Gauss-Markov estimate is that the number of observations m, (i.e. the dimension of ) need not be at least as large as the number of unknowns, n, (i.e. the dimension of ). The estimate for the linear observation process exists so long as the m-by-m matrix  exists; this is the case for any m if, for instance,

exists; this is the case for any m if, for instance,  is positive definite. Physically the reason for this property is that since is now a random variable, it is possible to form a meaningful estimate (namely its mean) even with no measurements. Every new measurement simply provides additional information which may modify our original estimate. Another feature of this estimate is that for m < n, there need be no measurement error. Thus, we may have

is positive definite. Physically the reason for this property is that since is now a random variable, it is possible to form a meaningful estimate (namely its mean) even with no measurements. Every new measurement simply provides additional information which may modify our original estimate. Another feature of this estimate is that for m < n, there need be no measurement error. Thus, we may have  , because as long as

, because as long as  is positive definite, the estimate still exists. Lastly, this technique can handle cases where the noise is correlated.

is positive definite, the estimate still exists. Lastly, this technique can handle cases where the noise is correlated.

Alternative form

An alternative form of expression can be obtained by using the matrix identity

which can be established by post-multiplying by  and pre-multiplying by

and pre-multiplying by  to obtain

to obtain

and

Since can now be written in terms of as  , we get a simplified expression for as

, we get a simplified expression for as

In this form the above expression can be easily compared with weighed least square and Gauss-Markov estimate. In particular, when  , corresponding to infinite variance of the apriori information concerning , the result

, corresponding to infinite variance of the apriori information concerning , the result  is identical to the weighed linear least square estimate with

is identical to the weighed linear least square estimate with  as the weight matrix. Moreover, if the components of are uncorrelated and have equal variance such that

as the weight matrix. Moreover, if the components of are uncorrelated and have equal variance such that  where

where  is an identity matrix, then

is an identity matrix, then  is identical to the ordinary least square estimate.

is identical to the ordinary least square estimate.

Sequential linear MMSE estimation

In many real-time application, observational data is not available in a single batch. Instead the observations are made in a sequence. A naive application of previous formulas would have us discard an old estimate and recompute a new estimate as fresh data is made available. But then we lose all information provided by the old observation. When the observations are scalar quantities, one possible way of avoiding such re-computation is to first concatenate the entire sequence of observations and then apply the standard estimation formula as done in Example 2. But this can be very tedious because as the number of observation increases so does the size of the matrices that need to be inverted and multiplied grow. Also, this method is difficult to extend to the case of vector observations. Another approach to estimation from sequential observations is to simply update an old estimate as additional data becomes available, leading to finer estimates. Thus a recursive method is desired where the new measurements can modify the old estimates. Implicit in these discussions is the assumption that the statistical properties of does not change with time. In other words, is stationary.

For sequential estimation, if we have an estimate  based on measurements generating space

based on measurements generating space  , then after receiving another set of measurements, we should subtract out from these measurements that part that could be anticipated from the result of the first measurements. In other words, the updating must be based on that part of the new data which is orthogonal to the old data.

, then after receiving another set of measurements, we should subtract out from these measurements that part that could be anticipated from the result of the first measurements. In other words, the updating must be based on that part of the new data which is orthogonal to the old data.

Suppose an optimal estimate has been formed on the basis of past measurements and that error covariance matrix is  . For linear observation processes the best estimate of based on past observation, and hence old estimate , is

. For linear observation processes the best estimate of based on past observation, and hence old estimate , is  . Subtracting

. Subtracting  from , we obtain

from , we obtain

.

.

The new estimate based on additional data is now

where  is the cross-covariance between and

is the cross-covariance between and  and

and  is the auto-covariance of

is the auto-covariance of

Using the fact that  and

and  , we can obtain the covariance matrices in terms of error covariance as

, we can obtain the covariance matrices in terms of error covariance as

Putting everything together, we have the new estimate as

and the new error covariance as

The repeated use of the above two equations as more observations become available lead to recursive estimation techniques. The expressions can be more compactly written as

The matrix  is often referred to as the gain factor. The repetition of these three steps as more data becomes available leads to an iterative estimation algorithm. The generalization of this idea to non-stationary cases gives rise to the Kalman filter.

is often referred to as the gain factor. The repetition of these three steps as more data becomes available leads to an iterative estimation algorithm. The generalization of this idea to non-stationary cases gives rise to the Kalman filter.

Special Case: Scalar Observations

As an important special case, an easy to use recursive expression can be derived when at each m-th time instant the underlying linear observation process yields a scalar such that  , where

, where  is 1-by-n known row vector whose values can change with time,

is 1-by-n known row vector whose values can change with time,  is n-by-1 random column vector to be estimated, and

is n-by-1 random column vector to be estimated, and  is scalar noise term with variance

is scalar noise term with variance  . After (m+1)-th observation, the direct use of above recursive equations give the expression for the estimate

. After (m+1)-th observation, the direct use of above recursive equations give the expression for the estimate  as:

as:

where  is the new scalar observation and the gain factor

is the new scalar observation and the gain factor  is n-by-1 column vector given by

is n-by-1 column vector given by

The  is n-by-n error covariance matrix given by

is n-by-n error covariance matrix given by

Here no matrix inversion is required. Also the gain factor depends on our confidence in the new data sample, as measured by the noise variance, versus that in the previous data. The initial values of and are taken to be the mean and covariance of the aprior probability density function of .

This important special case has also given rise to many other iterative methods (or adaptive filters), such as the least mean squares filter and recursive least squares filter, that directly solves the original MSE optimization problem using gradient descent methods. These methods bypass the need for covariance matrices.

Examples

Example 1

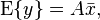

We shall take a linear prediction problem as an example. Let a linear combination of observed scalar random variables  and

and  be used to estimate another future scalar random variable

be used to estimate another future scalar random variable  such that

such that  . If the random variables

. If the random variables ![z=[z_{1},z_{2},z_{3},z_{4}]^{T}](../I/m/bf4e2a339e7a966b8cf5cb43ff6fe392.png) are real Gaussian random variables with zero mean and its covariance matrix given by

are real Gaussian random variables with zero mean and its covariance matrix given by

![\operatorname{cov}(Z)=\mathrm{E}[zz^{T}]=\left[\begin{array}{cccc}

1 & 2 & 3 & 4\\

2 & 5 & 8 & 9\\

3 & 8 & 6 & 10\\

4 & 9 & 10 & 15\end{array}\right],](../I/m/bfb8f9f074652ea18fc765d9453a7d7b.png)

then our task is to find the coefficients  such that it will yield an optimal linear estimate

such that it will yield an optimal linear estimate  .

.

In terms of the terminology developed in the previous sections, for this problem we have the observation vector ![y = [z_1, z_2, z_3]^T](../I/m/95351e126598ae5cd155475de4791c2f.png) , the estimator matrix

, the estimator matrix ![W = [w_1, w_2, w_3]](../I/m/d176656b323bef562352f647dab9156c.png) as a row vector, and the estimated variable

as a row vector, and the estimated variable  as a scalar quantity. The autocorrelation matrix is defined as

as a scalar quantity. The autocorrelation matrix is defined as

![C_Y=\left[\begin{array}{ccc}

E[z_{1},z_{1}] & E[z_{2},z_{1}] & E[z_{3},z_{1}]\\

E[z_{1},z_{2}] & E[z_{2},z_{2}] & E[z_{3},z_{2}]\\

E[z_{1},z_{3}] & E[z_{2},z_{3}] & E[z_{3},z_{3}]\end{array}\right]=\left[\begin{array}{ccc}

1 & 2 & 3\\

2 & 5 & 8\\

3 & 8 & 6\end{array}\right].](../I/m/8ead1a8cf8e859838a62dd8547c1f443.png)

The cross correlation matrix is defined as

![C_{YX}=\left[\begin{array}{c}

E[z_{4},z_{1}]\\

E[z_{4},z_{2}]\\

E[z_{4},z_{3}]\end{array}\right]=\left[\begin{array}{c}

4\\

9\\

10\end{array}\right].](../I/m/7450b188d496880965299b9004de13b5.png)

We now solve the equation  by inverting and pre-multiplying to get

by inverting and pre-multiplying to get

![C_Y^{-1}C_{YX}=\left[\begin{array}{ccc}

4.85 & -1.71 & -.142\\

-1.71 & .428 & .2857\\

-.142 & .2857 & -.1429\end{array}\right]\left[\begin{array}{c}

4\\

9\\

10\end{array}\right]=\left[\begin{array}{c}

2.57\\

-.142\\

.5714\end{array}\right]=W^T.](../I/m/1ab465e4d17d0a1b1be96836c6a7e6a2.png)

So we have

and

and  as the optimal coefficients for . Computing the minimum

mean square error then gives

as the optimal coefficients for . Computing the minimum

mean square error then gives ![\left\Vert e\right\Vert _{\min}^{2}=\mathrm{E}[z_{4}z_{4}]-WC_{YX}=15-WC_{YX}=.2857](../I/m/c6af80e742216bc13f473d993a783d1c.png) .[2] Note that it is not necessary to obtain an explicit matrix inverse of to compute the value of . The matrix equation can be solved by well known methods such as Gauss elimination method. A shorter, non-numerical example can be found in orthogonality principle.

.[2] Note that it is not necessary to obtain an explicit matrix inverse of to compute the value of . The matrix equation can be solved by well known methods such as Gauss elimination method. A shorter, non-numerical example can be found in orthogonality principle.

Example 2

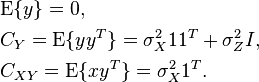

Consider a vector formed by taking  observations of a fixed but unknown scalar parameter disturbed by white Gaussian noise. We can describe the process by a linear equation

observations of a fixed but unknown scalar parameter disturbed by white Gaussian noise. We can describe the process by a linear equation  , where

, where ![1 = [1,1,\ldots,1]^T](../I/m/a9e1745d34e17c1de1c6be5a53019b9c.png) . Depending on context it will be clear if

. Depending on context it will be clear if  represents a scalar or a vector. Suppose that we know

represents a scalar or a vector. Suppose that we know ![[-x_0,x_0]](../I/m/b885887a892988181baa2e3c39029fb1.png) to be the range within which the value of is going to fall in. We can model our uncertainty of by an aprior uniform distribution over an interval , and thus will have variance of

to be the range within which the value of is going to fall in. We can model our uncertainty of by an aprior uniform distribution over an interval , and thus will have variance of  . Let the noise vector be normally distributed as

. Let the noise vector be normally distributed as  where is an identity matrix. Also and are independent and . It is easy to see that

where is an identity matrix. Also and are independent and . It is easy to see that

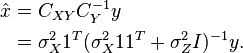

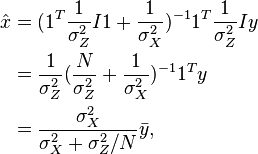

Thus, the linear MMSE estimator is given by

We can simplify the expression by using the alternative form for as

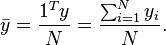

where for ![y = [y_1,y_2,\ldots,y_N]^T](../I/m/dd0a55e69918ad8c467a2d5f66e1c60d.png) we have

we have

Similarly, the variance of the estimator is

Thus the MMSE of this linear estimator is

For very large , we see that the MMSE estimator of a scalar with uniform aprior distribution can be approximated by the arithmetic average of all the observed data

while the variance will be unaffected by data  and the LMMSE of the estimate will tend to zero.

and the LMMSE of the estimate will tend to zero.

However, the estimator is suboptimal since it is constrained to be linear. Had the random variable also been Gaussian, then the estimator would have been optimal. Notice, that the form of the estimator will remain unchanged, regardless of the apriori distribution of , so long as the mean and variance of these distributions are the same.

Example 3

Consider a variation of the above example: Two candidates are standing for an election. Let the fraction of votes that a candidate will receive on an election day be ![x \in [0,1].](../I/m/4fc4d7b3b0488e4d3a5b5d4f5c317840.png) Thus the fraction of votes the other candidate will receive will be

Thus the fraction of votes the other candidate will receive will be  We shall take as a random variable with a uniform prior distribution over

We shall take as a random variable with a uniform prior distribution over ![[0,1]](../I/m/ccfcd347d0bf65dc77afe01a3306a96b.png) so that its mean is

so that its mean is  and variance is

and variance is  A few weeks before the election, two independent public opinion polls were conducted by two different pollsters. The first poll revealed that the candidate is likely to get

A few weeks before the election, two independent public opinion polls were conducted by two different pollsters. The first poll revealed that the candidate is likely to get  fraction of votes. Since some error is always present due to finite sampling and the particular polling methodology adopted, the first pollster declares their estimate to have an error

fraction of votes. Since some error is always present due to finite sampling and the particular polling methodology adopted, the first pollster declares their estimate to have an error  with zero mean and variance

with zero mean and variance  Similarly, the second pollster declares their estimate to be

Similarly, the second pollster declares their estimate to be  with an error

with an error  with zero mean and variance

with zero mean and variance  Note that except for the mean and variance of the error, the error distribution is unspecified. How should the two polls be combined to obtain the voting prediction for the given candidate?

Note that except for the mean and variance of the error, the error distribution is unspecified. How should the two polls be combined to obtain the voting prediction for the given candidate?

As with previous example, we have

Here both the  . Thus we can obtain the LMMSE estimate as the linear combination of and as

. Thus we can obtain the LMMSE estimate as the linear combination of and as

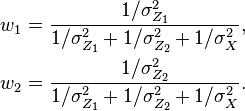

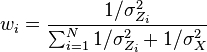

where the weights are given by

Here since the denominator term is constant, the poll with lower error is given higher weight in order to predict the election outcome. Lastly, the variance of the prediction is given by

which makes  smaller than

smaller than

In general, if we have pollsters, then the weight for i-th pollster is given by

Example 4

Suppose that a musician is playing an instrument and that the sound is received by two microphones, each of them located at two different places. Let the attenuation of sound due to distance at each microphone be  and

and  , which are assumed to be known constants. Similarly, let the noise at each microphone be and , each with zero mean and variances

, which are assumed to be known constants. Similarly, let the noise at each microphone be and , each with zero mean and variances  and

and  respectively. Let denote the sound produced by the musician, which is a random variable with zero mean and variance How should the recorded music from these two microphones be combined, after being synced with each other?

respectively. Let denote the sound produced by the musician, which is a random variable with zero mean and variance How should the recorded music from these two microphones be combined, after being synced with each other?

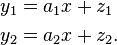

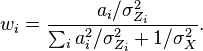

We can model the sound received by each microphone as

Here both the  . Thus, we can combine the two sounds as

. Thus, we can combine the two sounds as

where the i-th weight is given as

See also

- Bayesian estimator

- Mean squared error

- Least squares

- Minimum-variance unbiased estimator (MVUE)

- Orthogonality principle

- Wiener filter

- Kalman filter

- Linear prediction

- Zero forcing equalizer

Notes

Further reading

- Johnson, D. Minimum Mean Squared Error Estimators "Minimum Mean Squared Error Estimators" Check

|url= - Jaynes, E.T. (2003). Probability Theory: The Logic of Science. Cambridge University Press. ISBN 978-0521592710.

- Bibby, J.; Toutenburg, H. (1977). Prediction and Improved Estimation in Linear Models. Wiley. ISBN 9780471016564.

- Lehmann, E. L.; Casella, G. (1998). "Chapter 4". Theory of Point Estimation (2nd ed.). Springer. ISBN 0-387-98502-6.

- Kay, S. M. (1993). Fundamentals of Statistical Signal Processing: Estimation Theory. Prentice Hall. pp. 344–350. ISBN 0-13-042268-1.

- Luenberger, D.G. (1969). "Chapter 4, Least-squares estimation". Optimization by Vector Space Methods (1st ed.). Wiley. ISBN 978-0471181170.

- Moon, T.K.; Stirling, W.C. (2000). Mathematical Methods and Algorithms for Signal Processing (1st ed.). Prentice Hall. ISBN 978-0201361865.

- Van Trees, H. L. (1968). Detection, Estimation, and Modulation Theory, Part I. New York: Wiley. ISBN 0-471-09517-6.

- Haykin, S.O. (2013). Adaptive Filter Theory (5th ed.). Prentice Hall. ISBN 978-0132671453.