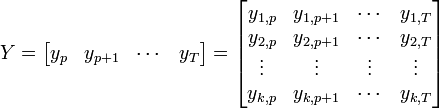

General matrix notation of a VAR(p)

This page shows the details for different matrix notations of a vector autoregression process with k variables.

Var(p)

Main article: Vector autoregression

Where each  is a vector of length k and each

is a vector of length k and each  is a k × k matrix.

is a k × k matrix.

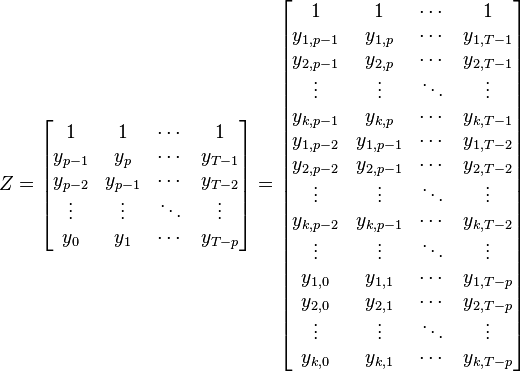

Large matrix notation

Equation by regression notation

Rewriting the y variables one to one gives:

Concise matrix notation

One can rewrite a VAR(p) with k variables in a general way which includes T+1 observations  through

through

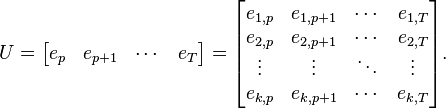

Where:

and

One can then solve for the coefficient matrix B (e.g. using an ordinary least squares estimation of  )

)

References

- Lütkepohl, Helmut (2005). New Introduction to Multiple Time Series Analysis. Berlin: Springer. ISBN 3540401725.

This article is issued from Wikipedia - version of the Monday, January 19, 2015. The text is available under the Creative Commons Attribution/Share Alike but additional terms may apply for the media files.