Compound interest

.gif)

| Part of a series of articles on the |

| mathematical constant e |

|---|

|

| Properties |

| Applications |

| Defining e |

| People |

| Related topics |

Compound interest is interest added to the principal of a deposit or loan so that the added interest also earns interest from then on. This addition of interest to the principal is called compounding. A bank account, for example, may have its interest compounded every year: in this case, an account with $1000 initial principal and 20% interest per year would have a balance of $1200 at the end of the first year, $1440 at the end of the second year, $1728 at the end of the third year, and so on.

To define an interest rate fully, allowing comparisons with other interest rates, both the interest rate and the compounding frequency must be disclosed. Since most people prefer to think of rates as a yearly percentage, many governments require financial institutions to disclose the equivalent yearly compounded interest rate on deposits or advances. For instance, the yearly rate for a loan with 1% interest per month is approximately 12.68% per annum (1.0112 − 1). This equivalent yearly rate may be referred to as annual percentage rate (APR), annual equivalent rate (AER), effective interest rate, effective annual rate, and other terms. When a fee is charged up front to obtain a loan, APR usually counts that cost as well as the compound interest in converting to the equivalent rate. These government requirements assist consumers in comparing the actual costs of borrowing more easily.

For any given interest rate and compounding frequency, an equivalent rate for any different compounding frequency exists.

Compound interest may be contrasted with simple interest, where interest is not added to the principal (there is no compounding). Compound interest is standard in finance and economics, and simple interest is used infrequently (although certain financial products may contain elements of simple interest).

Terminology

The effect of compounding depends on the frequency with which interest is compounded and the periodic interest rate which is applied. Therefore, to accurately define the amount to be paid under a legal contract with interest, the frequency of compounding (yearly, half-yearly, quarterly, monthly, daily, etc.) and the interest rate must be specified. Different conventions may be used from country to country, but in finance and economics the following usages are common:

The periodic rate is the amount of interest that is charged (and subsequently compounded) for each period divided by the amount of the principal. The periodic rate is used primarily for calculations and is rarely used for comparison.

The nominal annual rate or nominal interest rate is defined as the periodic rate multiplied by the number of compounding periods per year. For example, a monthly rate of 1% is equivalent to an annual nominal interest rate of 12%.

The effective annual rate is the total accumulated interest that would be payable up to the end of one year divided by the principal.

Economists generally prefer to use effective annual rates to simplify comparisons, but in finance and commerce the nominal annual rate may be quoted. When quoted together with the compounding frequency, a loan with a given nominal annual rate is fully specified (the amount of interest for a given loan scenario can be precisely determined), but the nominal rate cannot be directly compared with that of loans that have a different compounding frequency.

Loans and financing may have charges other than interest, and the terms above do not attempt to capture these differences. Other terms such as annual percentage rate and annual percentage yield may have specific legal definitions and may or may not be comparable, depending on the jurisdiction.

The use of the terms above (and other similar terms) may be inconsistent and vary according to local custom or marketing demands, for simplicity or for other reasons.

Exceptions

- US and Canadian T-Bills (short term Government debt) have a different convention. Their interest is calculated as (100 − P)/Pbnm, where P is the price paid. Instead of normalizing it to a year, the interest is prorated by the number of days t: (365/t)×100. (See day count convention).

- The interest on corporate bonds and government bonds is usually payable twice yearly. The amount of interest paid (each six months) is the disclosed interest rate divided by two and multiplied by the principal. The yearly compounded rate is higher than the disclosed rate.

- Canadian mortgage loans are generally compounded semi-annually with monthly (or more frequent) payments.[1]

- U.S. mortgages use an amortizing loan, not compound interest. With these loans, an amortization schedule is used to determine how to apply payments toward principal and interest. Interest generated on these loans is not added to the principal, but rather is paid off monthly as the payments are applied.

- It is sometimes mathematically simpler, e.g. in the valuation of derivatives, to use continuous compounding, which is the limit as the compounding period approaches zero. Continuous compounding in pricing these instruments is a natural consequence of Itō calculus, where financial derivatives are valued at ever increasing frequency, until the limit is approached and the derivative is valued in continuous time.

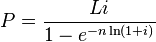

Mathematics of interest rates

Compound interest

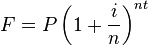

A formula for calculating the future value of a value generating compound interest is as follows:

where

- F = future value

- P = present value

- i = nominal interest rate

- n = compounding frequency

- t = time

Explanation

Time: Number of time units the sum will be subject to the compound interest computation. It is usually expressed in years.

Future value: Value after t time units.

Present value: It is the value before it becomes subject to the compound interest computation. In some fields like Engineering Economics it receives this name, in other fields such as Banking it is called principal value and; even in others, such as Finance, it may be called indistinctly by both names. Other names include current value, principal sum; or, simply, principal, which is widely used.

Compounding frequency: The number of times the interest is compounded per time unit. In other words, the frequency with which the interest is added to the principal to make the next computation to get the generated interest. For example, when a bank talks about monthly capitalization with a yearly rate of interest, it means that n is 12 and t is measured in years.

Nominal interest rate: When expressed in this form, it does not account for the full effect of the compounding frequency. It is usually expressed as a yearly percentage.

The total compound interest generated after t is:

where

- CI = compound interest

- F = future value

- P = present value

Example 1

Suppose an amount of 1500.00 is deposited in a bank paying an annual interest rate of 4.3%, compounded quarterly.

Then the balance after 6 years is found by using the formula above, with P = 1500, i = 4.3% = 0.043, n = 4, and t = 6:

So, the balance after 6 years is approximately 1938.84.

The amount of interest received can be calculated by subtracting the principal from this amount.

Example 2

Suppose the same amount of 1500.00 is deposited but now it is compounded biennially.

Then the balance after 6 years is found by using the formula above, with P = 1500, i = 0.043 (4.3%), n = 1/2 = 0.5 (the interest is compounded every two years), and t = 6:

So, the balance after 6 years is approximately 1921.24.

The amount of interest received can be calculated by subtracting the principal from this amount.

As expected, the interest is lesser because the compounding frequency decreased.

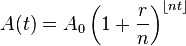

Periodic compounding

The amount function for compound interest is an exponential function in terms of time.

-

= Total time in years

= Total time in years

-

= Number of compounding periods per year (note that the total number of compounding periods is

= Number of compounding periods per year (note that the total number of compounding periods is  )

)

-

= Nominal annual interest rate expressed as a decimal. e.g.: 6% = 0.06

= Nominal annual interest rate expressed as a decimal. e.g.: 6% = 0.06

-

means that nt is rounded down to the nearest integer.

means that nt is rounded down to the nearest integer.

As n, the number of compounding periods per year, increases without limit, we have the case known as continuous compounding, in which case the effective annual rate approaches an upper limit of er − 1.

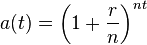

Since the principal  is simply a coefficient, it is often dropped for simplicity, and the resulting accumulation function is used in interest theory instead. Accumulation functions for simple and compound interest are listed below:

is simply a coefficient, it is often dropped for simplicity, and the resulting accumulation function is used in interest theory instead. Accumulation functions for simple and compound interest are listed below:

Note: A(t) is the amount function and a(t) is the accumulation function.

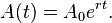

Continuous compounding

Continuous compounding can be thought of as making the compounding period infinitesimally small, achieved by taking the limit as n goes to infinity. See definitions of the exponential function for the mathematical proof of this limit. The amount after t periods of continuous compounding can be expressed in terms of the initial amount A0 as

It has been shown that the mathematics of continuous compounding is not limited to the valuation of continuously compounded financial instruments and flow annuities, but rather that the exponential equation is a versatile model that may be used for valuation of all financial contracts normally encountered.[2] In particular, any given interest rate (r) and compounding frequency (n) can be expressed in terms of a continuously compounded rate  :

:

which will also hold true for any other interest rate and compounding frequency. All formulas involving specific interest rates and compounding frequencies may be expressed in terms of the continuous interest rate and the compounding frequencies.

Force of interest

In mathematics, the accumulation functions are often expressed in terms of e, the base of the natural logarithm. This facilitates the use of calculus to manipulate interest formulae.

For any continuously differentiable accumulation function a(t) the force of interest, or more generally the logarithmic or continuously compounded return is a function of time defined as follows:

which is the rate of change with time of the natural logarithm of the accumulation function.

Conversely:  (since

(since  ; this can be viewed as a particular case of a product integral)

; this can be viewed as a particular case of a product integral)

When the above formula is written in differential equation format, then the force of interest is simply the coefficient of amount of change:

For compound interest with a constant annual interest rate r, the force of interest is a constant, and the accumulation function of compounding interest in terms of force of interest is a simple power of e:  or

or

The force of interest is less than the annual effective interest rate, but more than the annual effective discount rate. It is the reciprocal of the e-folding time. See also notation of interest rates.

A way of modeling the force of inflation is with Stoodley's formula:  where p, r and s are estimated.

where p, r and s are estimated.

Compounding basis

To convert an interest rate from one compounding basis to another compounding basis, use

![r_2=\left[\left(1+\frac{r_1}{n_1}\right)^\frac{n_1}{n_2}-1\right]{n_2},](../I/m/d66ee2cb42506817e2f21c63af6d4350.png)

where r1 is the interest rate with compounding frequency n1, and r2 is the interest rate with compounding frequency n2.

When interest is continuously compounded, use

where R is the interest rate on a continuous compounding basis, and r is the stated interest rate with a compounding frequency n.

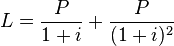

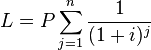

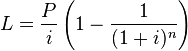

Mathematics of interest rate on loans

Monthly amortized loan or mortgage payments

The interest on loans and mortgages that are amortized—that is, have a smooth monthly payment until the loan has been paid off—is often compounded monthly. The formula for payments is found from the following argument.

Exact formula for monthly payment

An exact formula for the monthly payment is

or equivalently

-

= monthly payment

= monthly payment -

= principal

= principal -

= monthly interest rate

= monthly interest rate - = number of payment periods

This can be derived by considering how much is left to be repaid after each month. After the first month  is left, i.e. the initial amount has increased less the payment. If the whole loan was repaid after a month then

is left, i.e. the initial amount has increased less the payment. If the whole loan was repaid after a month then  so

so  After the second month

After the second month  is left, that is

is left, that is  . If the whole loan was repaid after two months

. If the whole loan was repaid after two months  this gives the equation

this gives the equation  . This equation generalises for a term of n months,

. This equation generalises for a term of n months,  . This is a geometric series which has the sum

. This is a geometric series which has the sum

which can be rearranged to give

This formula for the monthly payment on a U.S. mortgage is exact and is what banks use.

In Excel, the PMT() function is used. The syntax for the PMT function is:

= - PMT( interest_rate, number_payments, PV, [FV],[Type] )

See https://support.office.com/en-us/article/PMT-function-0214da64-9a63-4996-bc20-214433fa6441 for more details.

For example, for interest rate of 6% (0.06/12 p.m.), 25 years * 12 p.a., PV of $150,000, FV of 0, type of 0 gives:

= - PMT( 0.06/12, 25 * 12, 150000, 0, 0 )

= $966.45 p.m.

Approximate formula for monthly payment

A formula that is accurate to within a few percent can be found by

noting that for typical U.S. note rates ( and terms T=10–30 years), the monthly note rate is small compared to 1:

and terms T=10–30 years), the monthly note rate is small compared to 1:

so that the

so that the  which yields

a simplification so that

which yields

a simplification so that

which suggests defining auxiliary variables

.

.

is the monthly payment required for a zero

interest loan paid off in installments. In terms of these variables the

approximation can be written

is the monthly payment required for a zero

interest loan paid off in installments. In terms of these variables the

approximation can be written

The function  is even:

is even:

implying that it can be expanded in even powers of

implying that it can be expanded in even powers of  .

.

It follows immediately that  can be expanded in even powers

of plus the single term:

can be expanded in even powers

of plus the single term:

It will prove convenient then to define

so that  which can be expanded:

which can be expanded:

where the ellipses indicate terms that are higher order in even powers of  . The expansion

. The expansion

is valid to better than 1% provided  .

.

Example of mortgage payment

For a mortgage with a term of 30 years and a note rate of 4.5% we find:

which gives

so that

The exact payment amount is  so the approximation is an overestimate of about a sixth of a percent.

so the approximation is an overestimate of about a sixth of a percent.

Example of compound interest

Suppose that one cent had been invested at year 0 at a constant annual interest rate of 2%. After the first year, this interest rate was applied to the initial principal of one cent and the capital grew to 1.02 cent. In the second year, the interest earned was again 2%. However, from that time onwards, it was not applied to the principal only but to the compound capital value (i.e., 1.02 cent). Thus, after the second year, the capital increased to 1.02×1.02 cent. After the third year, the capital grew to 1.023 cent. After 2015 years, the capital has eventually grown to 1.022015 cent, which is roughly equal to 2.13x1017 cent or, more precisely, 213,474,546,813,926,768.7 cent.

Compare this figure to a similar investment using simple interest rather than compound interest. Suppose again that 1 cent is invested for a period of 2015 years at a constant annual interest rate of 2%. In this case, after 2015 years, the final capital is only 41.3 cent. This comparison highlights the effect of compounding, especially for long-term investments.

History

Compound interest was once regarded as the worst kind of usury and was severely condemned by Roman law and the common laws of many other countries.[3]

Richard Witt's book Arithmeticall Questions, published in 1613, was a landmark in the history of compound interest. It was wholly devoted to the subject (previously called anatocism), whereas previous writers had usually treated compound interest briefly in just one chapter in a mathematical textbook. Witt's book gave tables based on 10% (the then maximum rate of interest allowable on loans) and on other rates for different purposes, such as the valuation of property leases. Witt was a London mathematical practitioner and his book is notable for its clarity of expression, depth of insight and accuracy of calculation, with 124 worked examples.[4][5]

See also

| Look up interest in Wiktionary, the free dictionary. |

- Credit card interest

- Exponential growth

- Fisher equation

- Rate of return on investment

- Yield curve

- e (mathematical constant)

References

- ↑ http://laws.justice.gc.ca/en/showdoc/cs/I-15/bo-ga:s_6//en#anchorbo-ga:s_6 Interest Act (Canada), Department of Justice. The Interest Act specifies that interest is not recoverable unless the mortgage loan contains a statement showing the rate of interest chargeable, "calculated yearly or half-yearly, not in advance." In practice, banks use the half-yearly rate.

- ↑ Munshi, Jamal. "A New Discounting Model". ssrn.com.

- ↑

This article incorporates text from a publication now in the public domain: Chambers, Ephraim, ed. (1728). "article name needed". Cyclopædia, or an Universal Dictionary of Arts and Sciences (first ed.). James and John Knapton, et al.

This article incorporates text from a publication now in the public domain: Chambers, Ephraim, ed. (1728). "article name needed". Cyclopædia, or an Universal Dictionary of Arts and Sciences (first ed.). James and John Knapton, et al.

- ↑ Lewin, C G (1970). "An Early Book on Compound Interest - Richard Witt's Arithmeticall Questions". Journal of the Institute of Actuaries 96 (1): 121–132.

- ↑ Lewin, C G (1981). "Compound Interest in the Seventeenth Century". Journal of the Institute of Actuaries 108 (3): 423–442.

|