Random walk model of consumption

The random walk model of consumption was introduced by economist Robert Hall.[1] This model uses the Euler equation to model consumption. He created his consumption theory in response to the Lucas critique. Using Euler equations to model the random walk of consumption has become the dominant approach to modeling consumption.[2]

Background

Hall introduced his famous random walk model of consumption in 1978.[3] His approach is differentiated from earlier theories by the introduction of the Lucas critique to modeling consumption. He incorporated the idea of rational expectations into his consumption models and sets up the model so that consumers will maximize their utility.

Model

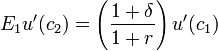

Consider a two-period case. The Euler equation for this model is

-

(1)

where  is the subjective time preference rate,

is the subjective time preference rate,  is the constant interest rate, and

is the constant interest rate, and  is the conditional expectation at time period 1.

is the conditional expectation at time period 1.

Assuming that the utility function is quadratic and  , equation (1) will yield

, equation (1) will yield

-

(2)

Applying the definition of expectations to equation (2) will give:

-

(3)

where  is the innovation term. Equation (3) suggests that consumption is a random walk because consumption is a function of only consumption from the previous period plus the innovation term.

is the innovation term. Equation (3) suggests that consumption is a random walk because consumption is a function of only consumption from the previous period plus the innovation term.

Advantages

Use of the Euler equations to estimate consumption appears to have advantages over traditional models. First, using Euler equations is simpler than conventional methods. This avoids the need to solve the consumer's optimization problem and is the most appealing element of using Euler equations to some economists.[4]

Criticisms

Controversy has arisen over using Euler equations to model consumption. Applying the Euler consumption equations has trouble explaining empirical data.[5][6] Attempting to use to Euler equations to model consumption in the United States has led some to reject the random walk hypothesis.[7] Some argue that this is due to the model's inability to uncover consumer preference variables such as the intertemporal elasticity of substitution.[8]

References

- ↑ Hall (1978)

- ↑ Chao, Hsiang-Ke (2007). "A Structure of the Consumption Function". Journal of Economic Methodology 14 (2): 227–248. doi:10.1080/13501780701394102.

- ↑ Hall, Robert (1978). "Stochastic Implications of the Life Cycle-Permanent Income Hypothesis: Theory and Evidence". Journal of Political Economy 86 (6): 971–987. doi:10.1086/260724. JSTOR 1840393.

- ↑ Attanasio, Orazio; Low, Hamish. "Estimating Euler Equations". Review of Economic Dynamics 7: 405–435. doi:10.1016/j.red.2003.09.003.

- ↑ Molana, H. (1991). "The Time Series Consumption Function: Error Correction, Random Walk and the Steady-State". The Economic Journal 101 (406): 382–403. doi:10.2307/2233547. JSTOR 2233547.

- ↑ Canzoneri, M. B.; Cumby, R. E.; Diba, B. T. (2007). "Euler equations and money market interest rates: A challenge for monetary policy models". Journal of Monetary Economics 54 (7): 1863. doi:10.1016/j.jmoneco.2006.09.001.

- ↑ Jaeger, Albert (1992). "Does Consumption Take a Random Walk?". The Review of Economics and Statistics 74 (4): 607–614. doi:10.2307/2109374.

- ↑ Carroll, Christopher D. (2001). "Death to the Log-Linearized Consumption Euler Equation! (And Very Poor Health to the Second-Order Approximation)". Advances in Macroeconomics 1 (1).

| ||||||||||||||