Executive compensation

Executive compensation or executive pay is composed of the financial compensation and other non-financial awards received by an executive from their firm for their service to the organization. It is typically a mixture of salary, bonuses, shares of or call options on the company stock, benefits, and perquisites, ideally configured to take into account government regulations, tax law, the desires of the organization and the executive, and rewards for performance.[1]

The three decades starting with the 1980s, saw a dramatic rise in executive pay relative to that of an average worker's wage in the United States,[2] and to a lesser extent in a number of other countries. Observers differ as to whether this rise is a natural and beneficial result of competition for scarce business talent that can add greatly to stockholder value in large companies, or a socially harmful phenomenon brought about by social and political changes that have given executives greater control over their own pay.[3][4] Executive pay is an important part of corporate governance, and is often determined by a company's board of directors.

Types

There are six basic tools of compensation or remuneration:

- salary

- short-term incentives (STIs), sometimes known as bonuses

- long-term incentive plans (LTIPs)

- employee benefits

- paid expenses (perquisites)

- insurance

In a modern corporation, the CEO and other top executives are often paid salary plus short-term incentives or bonuses. This combination is referred to as Total Cash Compensation (TCC). Short-term incentives usually are formula-driven and have some performance criteria attached depending on the role of the executive. For example, the Sales Director's performance related bonus may be based on incremental revenue growth turnover; a CEO's could be based on incremental profitability and revenue growth. Bonuses are after-the-fact (not formula driven) and often discretionary. Executives may also be compensated with a mixture of cash and shares of the company which are almost always subject to vesting restrictions (a long-term incentive). To be considered a long-term incentive the measurement period must be in excess of one year (3–5 years is common). The vesting term refers to the period of time before the recipient has the right to transfer shares and realize value. Vesting can be based on time, performance or both. For example, a CEO might get 1 million in cash, and 1 million in company shares (and share buy options used). Vesting can occur in two ways: "cliff vesting" (vesting occurring on one date), and "graded vesting" (which occurs over a period of time) and which maybe "uniform" (e.g., 20% of the options vest each year for 5 years) or "non-uniform" (e.g., 20%, 30% and 50% of the options vest each year for the next three years). Other components of an executive compensation package may include such perks as generous retirement plans, health insurance, a chauffeured limousine, an executive jet, and interest-free loans for the purchase of housing.

Stock options

Executive stock option pay rose dramatically in the United States after scholarly support from University of Chicago educated Professors Michael C. Jensen and Kevin J. Murphy. Due to their publications in the Harvard Business Review 1990 and support from Wall Street and institutional investors, Congress passed a law making it cost effective to pay executives in equity.

Supporters of stock options say they align the interests of CEOs to those of shareholders, since options are valuable only if the stock price remains above the option's strike price. Stock options are now counted as a corporate expense (non-cash), which impacts a company's income statement and makes the distribution of options more transparent to shareholders. Critics of stock options charge that they are granted without justification as there is little reason to align the interests of CEOs with those of shareholders. Empirical evidence shows since the wide use of stock options, executive pay relative to workers has dramatically risen. Moreover, executive stock options contributed to the accounting manipulation scandals of the late 1990s and abuses such as the options backdating of such grants. Finally, researchers have shown that relationships between executive stock options and stock buybacks, implying that executives use corporate resources to inflate stock prices before they exercise their options.

Stock options also incentivize executives to engage in risk-seeking behavior. This is because the value of a call option increases with increased volatility (see options pricing). Stock options also present a potential up-side gain (if the stock price goes up) for the executive, but no downside risk (if the stock price goes down, the option simply isn't exercised). Stock options therefore can incentivize excessive risk seeking behavior that can lead to catastrophic corporate failure.

Restricted stock

Executives are also compensated with restricted stock, which is stock given to an executive that cannot be sold until certain conditions are met and has the same value as the market price of the stock at the time of grant. As the size of stock option grants have been reduced, the number of companies granting restricted stock either with stock options or instead of, has increased. Restricted stock has its detractors, too, as it has value even when the stock price falls. As an alternative to straight time vested restricted stock, companies have been adding performance type features to their grants. These grants, which could be called performance shares, do not vest or are not granted until these conditions are met. These performance conditions could be earnings per share or internal financial targets.

Levels

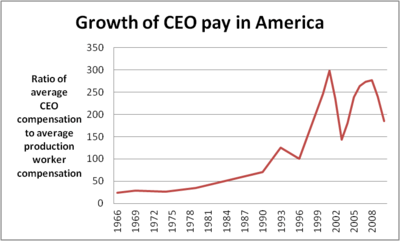

The levels of compensation in all countries has been rising dramatically over the past decades. Not only is it rising in absolute terms, but also in relative terms. In 2007, the world's highest paid chief executive officers and chief financial officers were American. They made 400 times more than average workers—a gap 20 times bigger than it was in 1965.[5] In 2010 the highest paid CEO was Viacom's Philippe P. Dauman at $84.5 million[6] The U.S. has the world's highest CEO's compensation relative to manufacturing production workers. According to one 2005 estimate the U.S. ratio of CEO's to production worker pay is 39:1 compared to 31.8:1 in UK; 25.9:1 in Italy; 24.9:1 in New Zealand.[7]

Controversy

The explosion in executive pay has become controversial, criticized by not only leftists but conservative establishmentarians such as Peter Drucker, John Bogle,[8][9] Warren Buffett.[5]

The idea that stock options and other alleged pay-for-performance are driven by economics has also been questioned. According to economist Paul Krugman,

"Today the idea that huge paychecks are part of a beneficial system in which executives are given an incentive to perform well has become something of a sick joke. A 2001 article in Fortune, "The Great CEO Pay Heist" encapsulated the cynicism: You might have expected it to go like this: The stock isn't moving, so the CEO shouldn't be rewarded. But it was actually the opposite: The stock isn't moving, so we've got to find some other basis for rewarding the CEO.` And the article quoted a somewhat repentant Michael Jensen [a theorist for stock option compensation]: `I've generally worried these guys weren't getting paid enough. But now even I'm troubled.'"[10][11]

Defenders of high executive pay say that the global war for talent and the rise of private equity firms can explain much of the increase in executive pay. For example, while in conservative Japan a senior executive has few alternatives to his current employer, in the United States it is acceptable and even admirable for a senior executive to jump to a competitor, to a private equity firm, or to a private equity portfolio company. Portfolio company executives take a pay cut but are routinely granted stock options for ownership of ten percent of the portfolio company, contingent on a successful tenure. Rather than signaling a conspiracy, defenders argue, the increase in executive pay is a mere byproduct of supply and demand for executive talent. However, U.S. executives make substantially more than their European and Asian counterparts.[5]

United States

The U.S. Securities and Exchange Commission (SEC) has asked publicly traded companies to disclose more information explaining how their executives' compensation amounts are determined. The SEC has also posted compensation amounts on its website[13] to make it easier for investors to compare compensation amounts paid by different companies. It is interesting to juxtapose SEC regulations related to executive compensation with Congressional efforts to address such compensation.[14]

Since the 1990s, CEO compensation in the US has outpaced corporate profits, economic growth and the average compensation of all workers. Between 1980 and 2004, Mutual Fund founder John Bogle estimates total CEO compensation grew 8.5%/year, compared to corporate profit growth of 2.9%/year and per capita income growth of 3.1%.[15][16] By 2006 CEOs made 400 times more than average workers—a gap 20 times bigger than it was in 1965.[5] As a general rule, the larger the corporation the larger the CEO compensation package.[17]

The share of corporate income devoted to compensating the five highest paid executives of (each) public firms more than doubled from 4.8% in 1993-1995 to 10.3% in 2001-2003.[18] The pay for the five top-earning executives at each of the largest 1500 American companies for the ten years from 1994 to 2004 is estimated at approximately $500 billion in 2005 dollars.[19]

As of late March 2012 USA Today's tally showed the median CEO pay of the S&P 500 for 2011 was $9.6 million.[20]

Lower level executives also have fared well. About 40% of the top 0.1% income earners in the United States are executives, managers, or supervisors (and this doesn't include the finance industry) — far out of proportion to less than 5% of the working population that management occupations make up.[21]

A study by University of Florida researchers found that highly paid CEOs improve company profitability as opposed to executives making less for similar jobs.[22] However, a review of the experimental and quasi-experimental research relevant to executive compensation, by Philippe Jacquart and J. Scott Armstrong, found opposing results. In particular, the authors conclude that "the notion that higher pay leads to the selection of better executives is undermined by the prevalence of poor recruiting methods. Moreover, higher pay fails to promote better performance. Instead, it undermines the intrinsic motivation of executives, inhibits their learning, leads them to ignore other stakeholders, and discourages them from considering the long-term effects of their decisions on stakeholders" [23] Another study by Professors Lynne M. Andersson and Thomas S. Batemann published in the Journal of Organizational Behavior found that highly paid executives are more likely to behave cynically and therefore show tendencies of unethical performance.[24]

Australia

In Australia, shareholders can vote against the pay rises of board members, but the vote is non-binding. Instead the shareholders can sack some or all of the board members.[25] Australia's corporate watchdog, the Australian Securities and Investments Commission has called on companies to improve the disclosure of their remuneration arrangements for directors and executives.[26]

Canada

A 2012 report by the Canadian Centre for Policy Alternatives demonstrated that the top 100 Canadian CEOs were paid an average of C$8.4 million in 2010, a 27% increase over 2009, this compared to C$44,366 earned by the average Canadian that year, 1.1% more than in 2009.[27] The top three earners were automotive supplier Magna International Inc. founder Frank Stronach at C$61.8 million, co-CEO Donald Walker at C$16.7 million and former co-CEO Siegfried Wolf at C$16.5 million.[27]

Europe

In 2008, Jean-Claude Juncker, president of the European Commission's “Eurogroup” of finance ministers, called excessive pay a “social scourge” and demanded action.[28]

United Kingdom

Although executive compensation in the UK is said to be "dwarfed" by that of corporate America, it has caused public upset.[29] In response to criticism of high levels of executive pay, the Compass organisation set up the High Pay Commission. Its 2011 report described the pay of executives as "corrosive".[30]

In December 2011/January 2012 two of the country’s biggest investors, Fidelity Worldwide Investment, and the Association of British Insurers, called for greater shareholder control over executive pay packages.[31] Dominic Rossi of Fidelity Worldwide Investment stated, “Inappropriate levels of executive reward have destroyed public trust and led to a situation where all directors are perceived to be overpaid. The simple truth is that remuneration schemes have become too complex and, in some cases, too generous and out of line with the interests of investors.” Two sources of public anger were Barclays, where senior executives were promised million-pound pay packages despite a 30% drop in share price; and Royal Bank of Scotland where the head of investment banking was set to earn a "large sum" after thousands of employees were made redundant.[31]

Regulation

There are a number of strategies that could be employed as a response to the growth of executive compensation.

- Extend the vesting period of executives' stock and options.[32] Current vesting periods can be as short as three years, which encourages managers to inflate short-term stock price at the expense of long-run value, since they can sell their holdings before a decline occurs.[33]

- As passed in the Swiss referendum "against corporate Rip-offs" of 2013, investors gain total control over executive compensation, and the executives of a board of directors. Institutional intermediaries must all vote in the interests of their beneficiaries and banks are prohibited from voting on behalf of investors.

- Disclosure of salaries is the first step, so that company stakeholders can know and decide whether or not they think remuneration is fair. In the UK, the Directors' Remuneration Report Regulations 2002[34] introduced a requirement into the old Companies Act 1985, the requirement to release all details of pay in the annual accounts. This is now codified in the Companies Act 2006. Similar requirements exist in most countries, including the U.S., Germany, and Canada.

- A say on pay - a non-binding vote of the general meeting to approve director pay packages, is practised in a growing number of countries. Some commentators have advocated a mandatory binding vote for large amounts (e.g. over $5 million).[35] The aim is that the vote will be a highly influential signal to a board to not raise salaries beyond reasonable levels. The general meeting means shareholders in most countries. In most European countries though, with two-tier board structures, a supervisory board will represent employees and shareholders alike. It is this supervisory board which votes on executive compensation.

- Another proposed reform is the bonus-malus system, where executives carry down-side risk in addition to potential up-side reward.

- Progressive taxation is a more general strategy that affects executive compensation, as well as other highly paid people. There has been a recent trend to cutting the highest bracket tax payers, a notable example being the tax cuts in the U.S. For example, the Baltic States have a flat tax system for incomes. Executive compensation could be checked by taxing more heavily the highest earners, for instance by taking a greater percentage of income over $200,000.

- Maximum wage is an idea which has been enacted in early 2009 in the United States, where they capped executive pay at $500,000 per year for companies receiving extraordinary financial assistance from the U.S. taxpayers. The argument is to place a cap on the amount that any person may legally make, in the same way as there is a floor of a minimum wage so that people can not earn too little.[36]

- Debt Like Compensation - If an executive is compensated exclusively with equity, he will take risks to benefit shareholders at the expense of debtholders. Thus, there are several proposals to compensate executives with debt as well as equity, to mitigate their risk-shifting tendencies.[37][38]

- Indexing Operating Performance is a way to make bonus targets business cycle independent. Indexed bonus targets move with the business cycle and are therefore fairer and valid for a longer period of time.

- Two strikes - In Australia an amendment to the Corporations Amendment(Improving Accountability on Director and Executive Remuneration) Bill 2011[39] puts in place processes to trigger a re-election of a Board where a 25% "no" vote by shareholders to the company's remuneration report has been recorded in two consecutive annual general meetings. When the second "no" vote is recorded at an AGM, the meeting will be suspended and shareholders will be asked to vote on whether a spill meeting is to be held. This vote must be upheld by at least a 50% majority for the spill (or re-election process) to be run. At a spill meeting all directors current at the time the remuneration report was considered are required to stand for re-election.[40]

- Independent non-executive director setting of compensation is widely practised. An independent remuneration committee is an attempt to have pay packages set at arms' length from the directors who are getting paid.

See also

- Agency cost

- Bonus-Malus

- Corporate-owned life insurance

- Golden handshake

- Golden parachute

- Options backdating

- Proxy Advisor

- Remuneration

- We are the 99%

Notes

- ↑ The complete guide to executive compensation By Bruce R. Ellig, 2002

- ↑ see, for one example, The Guardian, August 4, 2005, "US executive pay goes off the scale"

- ↑ Lucian Bebchuk and Jesse Fried, Pay Without Performance (2004)

- ↑ Krugman, Paul, The Conscience of a Liberal, W W Norton & Company, 2007, 143-148

- 1 2 3 4 "Letter From Washington: As U.S. rich-poor gap grows, so does public outcry". Bloomberg News. International Herald Tribune. Retrieved 2007-02-18.

- ↑ The Pay at the Top April 9, 2011

- ↑ Landy, Heather, "Behind the Big Paydays", The Washington Post, November 15, 2008

- ↑ The Executive Compensation System is Broken John C. Bogle| December 2005

- ↑ A Crisis of Ethic Proportions By JOHN C. BOGLE wsj.com April 21, 2009

- ↑ The Great CEO Pay Heist Executive 25 June 2001, Fortune

- ↑ Krugman, Paul, The Conscience of a Liberal, 2007, p.148

- ↑ More compensation heading to the very top: 1965-2009. May 16, 2011.

- ↑ The Securities and Exchange Commission website

- ↑ Kenneth Rosen, Who Killed Katie Couric? And Other Tales from the World of Executive Compensation Reform, 76 Fordham Law Review 2907 (2007)

- ↑ Reflections on CEO Compensation by John C. Bogle| Academy of Management| May 2008

- ↑ Pay Madness At Enron Dan Ackman, 03.22.2002

- ↑ Kevin Hallock, `Dual Agency: Corporate Boards with Reciprocally Interlocking Relationships,` in Executive Compensation and Shareholder Value: Theory and Evidence, ed. Jennifer Carpenter and David Yermack (Boston: Kluwer Academic Publishers, 1999) p.58

- ↑ Based on the ExecuComp database of 1500 companies. Bebchuk, Lucian; Grinstein, Yaniv (April 2005). "The Growth of Executive Pay" (PDF). Harvard University: John M. Olin Center for Law, Economics and Business.

- ↑ Based on the ExecuComp database , from Bebchuk and Fried, Pay Without Performance (2004), (p.9-10)

- ↑ CEO pay rises again in 2011, while workers struggle to find work By Matt Krantz and Barbara Hansen, USA TODAY. Updated 31 March 2012

- ↑ Jobs and Income Growth of Top Earners and the Causes of Changing Income Inequality: Evidence from U.S. Tax Return Data Jon Bakija, Adam Cole, Bradley T. Heim| March 2012

- ↑ Cathy Keen (2009-12-17). "Paying CEOs more than other CEOs results in stockholder dividends". University of Florida News. ufl.edu.

- ↑ Jacquart, Philippe; Armstrong, J. Scott. "Are Top Executives Paid Enough? An Evidence Based Review".

- ↑ Batemann, Thomas. "Journal of Organizational Behavior" 18 (5). Retrieved 2010.

- ↑ "Shareholders told to oust directors". Business Day. The Age. 28 February 2009. Retrieved 10 March 2014.

- ↑ "ASIC calls for better executive remuneration disclosure". Media Release: 12–34MR. ASIC. 29 February 2012. Retrieved 10 March 2014.

- 1 2 Highest-paid Canadian CEOs got 27 per cent pay hike Dana Flavelle| thestar.com 2| January 2012

- ↑ Executive pay in Europe| Jun 12th 2008

- ↑ "US executive pay goes off the scale" The Guardian, August 4, 2005

- ↑ High pay of UK executives corrosive, report says, BBC News

- 1 2 In Britain, Rising Outcry Over Executive Pay That Makes ‘People’s Blood Boil’ By JULIA WERDIGIER| nytimes.com 22 January 2012| accessed 2 April 2012

- ↑ How to Fix Executive Compensation by Alex Edmans, 27 February 2012

- ↑ When Bosses Take The Short-Term View by The Economist, 8 February 2014

- ↑ SI 2002/1986

- ↑ Failing Banks' Executive Pay May Face New Rules

- ↑ Dietl, H., Duschl, T. and Lang, M. (2010): "Executive Salary Caps: What Politicians, Regulators and Managers Can Learn from Major Sports Leagues", University of Zurich, ISU Working Paper Series No. 129.

- ↑ Alex Edmans and Qi Liu (2011): Inside Debt Review of Finance

- ↑ Why It Pays to Link Executive Compensation with Corporate Debt 7 July 2010 Knowledge@Wharton

- ↑ Quest, Two strikes rule passed by Senate Accessed 30 December 2011

- ↑ Allion Legal, Remuneration Reform: How does the '2 strikes' rule affect your Company and your Board? Accessed 30 December 2011

Further reading

Books

- Lucian Bebchuk and Jesse Fried, Pay without performance: The Unfulfilled Promise of Executive Compensation (2006)

Policy papers

- Allaire, Yvan Executive compensation Pay for value: Cutting the Gordian Knot of Executive Compensation (March 2013) Institute for governance (IGOPP)

Journal articles

- Frydman, Carola; Saks, Raven E. (2007-01-18). "Historical Trends in Executive Compensation 1936-2005" (PDF).

- Bebchuk, Lucian; Grinstein, Yaniv (April 2005). "The Growth of Executive Pay" (PDF). Harvard University: John M. Olin Center for Law, Economics and Business.

- Yoram Landskroner and Alon Raviv, 'The 2007-2009 Financial Crisis and Executive Compensation: An Analysis and a Proposal for a Novel Structure'

- Paolo Cioppa, 'Executive Compensation: The Fallacy of Disclosure'

- Kenneth Rosen, 'Who Killed Katie Couric? And Other Tales from the World of Executive Compensation Reform' (2007) 76 Fordham Law Review 2907

- Carola Frydman 'Learning from the Past: Trends in Executive Compensation over the Twentieth Century' (2008) Center for Economic Studies

Newspaper articles

- Sean O'Grady, 'Economist Stiglitz blames crunch on 'flawed' City bonuses system' (24.3.2008) The Independent

- Louise Story, 'Windfall Is Seen as Bank Bonuses Are Paid in Stock' (7.11.2009) New York Times

- '"Chief executives' pay rises to £2.5m average' (4.8.2005) The Guardian

External links

- Cost-Cutting Strategies in the Downturn: 2009 Pulse Survey

- 2012 Executive Pay Rankings by ExecutivePay.info

- Forbes.com - Executive Pay (updated with 2004 pay)

- 2011 Executive PayWatch

- America's Highest Paid CEOs

- Why CEOs earn 400 times average employee salaries | CanadianBusiness.com

- High Pay Commission

- 466 Hours of Worker Overtime Equals One Hour of CEO Pay | NerdWallet Investing—NerdWallet.com (December 6, 2013)