Davis distribution

| Parameters |

scale scale shape shape location location |

|---|---|

| Support |

|

Where  is the Gamma function and is the Gamma function and  is the Riemann zeta function is the Riemann zeta function | |

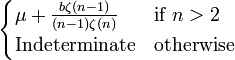

| Mean |

|

| Variance |

|

In statistics, the Davis distributions are a family of continuous probability distributions. It is named after Harold T. Davis (1892–1974), who in 1941 proposed this distribution to model income sizes. (The Theory of Econometrics and Analysis of Economic Time Series). It is a generalization of the Planck's law of radiation from statistical physics.

Definition

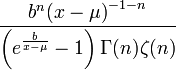

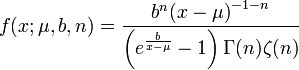

The probability density function of the Davis distribution is given by

where is the Gamma function and is the Riemann zeta function. Here μ, b, and n are parameters of the distribution, and n need not be an integer.

Background

In an attempt to derive an expression that would represent not merely the upper tail of the distribution of income, Davis required an appropriate model with the following properties[1]

-

for some

for some

- A modal income exists

- For large x, the density behaves like a Pareto distribution:

Related distributions

- If

then

then (Planck's law)

(Planck's law)

Notes

References

- Kleiber, Christian (2003). Statistical Size Distributions in Economics and Actuarial Sciences. Wiley Series in Probability and Statistics. ISBN 978-0-471-15064-0.

- Davis, H. T. (1941). The Analysis of Economic Time Series. The Principia Press, Bloomington, Indiana Download book

- VICTORIA-FESER, Maria-Pia. (1993) Robust methods for personal income distribution models. Thèse de doctorat : Univ. Genève, 1993, no. SES 384 (p. 178)