Chow test

The Chow test is a statistical and econometric test of whether the coefficients in two linear regressions on different data sets are equal. The Chow test was invented by economist Gregory Chow in 1960. In econometrics, the Chow test is most commonly used in time series analysis to test for the presence of a structural break. In program evaluation, the Chow test is often used to determine whether the independent variables have different impacts on different subgroups of the population.

| structural break | program evaluation |

|---|---|

|

|

|

|

At |

Comparison of 2 different programs (red, green) existing in a common data set, separate regressions for both programs deliver a better modelling than a combined regression (black). |

there is a structural break, regression on the subintervals

there is a structural break, regression on the subintervals ![[0,1.7]](../I/m/83dcdd20cb06638c88055a2214851654.png) and

and ![[1.7,4]](../I/m/5135911b0ccbe339dff52b21d8f57b2e.png) delivers a better modelling than the combined regression(dashed) over the whole interval.

delivers a better modelling than the combined regression(dashed) over the whole interval.Suppose that we model our data as

If we split our data into two groups, then we have

and

The null hypothesis of the Chow test asserts that  ,

,  , and

, and  , and there is the assumption that the model errors

, and there is the assumption that the model errors  are independent and identically distributed from a normal distribution with unknown variance.

are independent and identically distributed from a normal distribution with unknown variance.

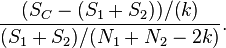

Let  be the sum of squared residuals from the combined data,

be the sum of squared residuals from the combined data,  be the sum of squared residuals from the first group, and

be the sum of squared residuals from the first group, and  be the sum of squared residuals from the second group.

be the sum of squared residuals from the second group.  and

and  are the number of observations in each group and

are the number of observations in each group and  is the total number of parameters (in this case, 3). Then the Chow test statistic is

is the total number of parameters (in this case, 3). Then the Chow test statistic is

The test statistic follows the F distribution with and  degrees of freedom.

degrees of freedom.

Remarks

- The global sum of squares (SSE) if often called Restricted Sum of Squares (RSSM) as we basically test a constrained model where we have 2K assumptions (with K the number of regressors).

- Some software like SAS will use a predictive Chow test when the size of a subsample is less than the number of regressors.

References

- Chow, Gregory C. (1960). "Tests of Equality Between Sets of Coefficients in Two Linear Regressions". Econometrica 28 (3): 591–605. doi:10.2307/1910133. JSTOR 1910133.

- Doran, Howard E. (1989). Applied Regression Analysis in Econometrics. CRC Press. p. 146. ISBN 0-8247-8049-3.

- Dougherty, Christopher (2007). Introduction to Econometrics. Oxford University Press. p. 194. ISBN 0-19-928096-7.

- Kmenta, Jan (1986). Elements of Econometrics (Second ed.). New York: Macmillan. pp. 412–423. ISBN 0-472-10886-7.

- Wooldridge, Jeffrey M. (2009). Introduction to Econometrics: A Modern Approach (Fourth ed.). Mason: South-Western. pp. 243–246. ISBN 978-0-324-66054-8.

External links

- Computing the Chow statistic, Chow and Wald tests, Chow tests: Series of FAQ explanations from the Stata Corporation at https://www.stata.com/support/faqs/

- : Series of FAQ explanations from the SAS Corporation