Capital allocation line

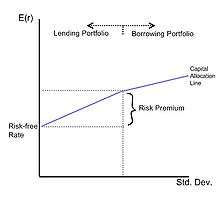

Capital allocation line (CAL) is a graph created by investors to measure the risk of risky and risk-free assets. The graph displays the return to be made by taking on a certain level of risk. Its slope is known as the "reward-to-variability ratio".[1]

Formula

It can be proven that it is a straight line and that it has the following equation:

In this formula P is the risky portfolio, F is riskless portfolio, and C is a combination of portfolios P and F.

The slope of the capital allocation line is equal to the incremental return of the portfolio to the incremental increase of risk. Hence, the slope of the capital allocation line is called the reward-to-variability ratio because the expected return increases continually with the increase of risk as measured by the standard deviation.[2]

See also

- Capital market line

- Security market line

- Security characteristic line

- Market portfolio

- Sharpe ratio, which equals the slope of the Capital Allocation Line