Budget constraint

and

and

Disambig: Budget constraint is sometimes called a budget line. For the meaning of budget line as a lower cost product range see value brand.

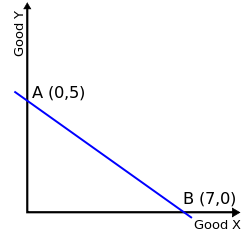

A budget constraint represents all the combinations of goods and services that a consumer may purchase given current prices within his or her given income. Consumer theory uses the concepts of a budget constraint and a preference map to analyze consumer choices. Both concepts have a ready graphical representation in the two-good case.

Uses

Individual choice

Consumer behaviour is a maximisation problem. It means making the most of our limited resources to maximise our utility. As consumers are insatiable, and utility functions grow with quantity, the only thing that limits our consumption is our own budget.[1]

An individual consumer should choose to consume goods at the point where the most preferred available indifference curve on his preference map is tangent to his budget constraint. That is, the indifference curve tangent to the budget constraint represents the maximum utility obtained utilizing the entire budget of the consumer. The tangent point (the xy coordinate) represents the amount of goods x and y the consumer should purchase to fully utilize their budget to obtain maximum utility.[2] A line connecting all points of tangency between the indifference curve and the budget constraint is called the expansion path.[3]

All two dimensional budget constraints are generalized into the equation:

Where:

-

money income allocated to consumption (after saving and borrowing)

money income allocated to consumption (after saving and borrowing) -

the price of a specific good

the price of a specific good -

the price of all other goods

the price of all other goods -

amount purchased of a specific good

amount purchased of a specific good -

amount purchased of all other goods

amount purchased of all other goods

The equation can be rearranged to represent the shape of the curve on a graph:

, where

, where  is the y-intercept and

is the y-intercept and  is the slope, representing a downward sloping budget line.

is the slope, representing a downward sloping budget line.

The factors that can shift the budget line are a change in income (m), a change in the price of a specific good ( ), or a change in the price of all other goods (

), or a change in the price of all other goods ( ).

).

International economics

A production-possibility frontier is a constraint in some ways analogous to a budget constraint, showing limitations on a country's production of multiple goods based on the limitation of available factors of production. Under autarky this is also the limitation of consumption by individuals in the country. However, the benefits of international trade are generally demonstrated through allowance of a shift in the consumption-possibility frontiers of each trade partner which allows access to a more appealing indifference curve. In the "toolbox" Hecksher-Ohlin and Krugman models of international trade, the budget constraint of the economy (its CPF) is determined by the terms-of-trade (TOT) as a downward-sloped line with slope equal to those TOTs of the economy. (The TOTs are given by the price ratio Px/Py, where x is the exportable commodity and y is the importable).

Many goods

While low level demonstrations of budget constraints are often limited to ←two good situations which provide easy graphical representation, it is possible to demonstrate the relationship between multiple goods through a budget constraint.

In such a case, assuming there are  goods, called

goods, called  for

for  , that the price of good is denoted by

, that the price of good is denoted by  , and if

, and if  is the total amount that may be spent, then the budget constraint is:

is the total amount that may be spent, then the budget constraint is:

Further, if the consumer spends his income entirely, the budget constraint binds:

In this case, the consumer cannot obtain an additional unit of good without giving up some other good. For example, he could purchase an additional unit of good by giving up  units of good

units of good

Notes

- ↑ http://www.policonomics.com/budget-constraint/

- ↑ Lipsey (1975). p 182.

- ↑ Salvatore, Dominick (1989). Schaum's outline of theory and problems of managerial economics, McGraw-Hill, ISBN 978-0-07-054513-7

See also

- Choice modelling

- Contingent valuation

- Guns versus butter model

- Heckscher–Ohlin theorem on country level budget constraints called resource endowments

- Intertemporal budget constraint

- Opportunity cost

- Scarcity

- Trade-off

References

- Lipsey, Richard G. (1975). An introduction to positive economics (fourth ed.). Weidenfeld & Nicolson. pp. 214–7. ISBN 0-297-76899-9.