Tax rate

| Taxation |

|---|

| An aspect of fiscal policy |

|

|

|

Distribution |

|

|

By country

|

In a tax system and in economics, the tax rate describes the ratio (usually expressed as a percentage) at which a business or person is taxed. There are several methods used to present a tax rate: statutory, average, marginal, and effective. These rates can also be presented using different definitions applied to a tax base: inclusive and exclusive.

Statutory

A statutory tax rate is the legally imposed rate. An income tax could have multiple statutory rates for different income levels, where a sales tax may have a flat statutory rate.[1]

Average

An average tax rate is the ratio of the total amount of taxes paid to the total tax base (taxable income or spending), expressed as a percentage.[1]

- Let

be the total tax liability.

be the total tax liability. - Let

be the total tax base.

be the total tax base.

In a proportional tax, the tax rate is fixed and the average tax rate equals this tax rate. In case of tax brackets, commonly used for progressive taxes, the average tax rate increases as taxable income increases through tax brackets, asymptoting to the top tax rate. For example, consider a system with three tax brackets, 10%, 20%, and 30%, where the 10% rate applies to income from $1 to $10,000, the 20% rate applies to income from $10,001 to $20,000, and the 30% rate applies to all income above $20,000. Under this system, someone earning $25,000 would pay $1,000 for the first $10,000 of income (10%); $2,000 for the second $10,000 of income (20%); and $1,500 for the last $5,000 of income (30%). In total, they would pay $4,500, or an 18% average tax rate.

Marginal

A marginal tax rate refers to the tax rate an individual would pay on one additional dollar of income.[1][2][3] Thus, the marginal tax rate is the tax percentage on the last dollar earned. In the United States in 2013, for example, the highest marginal tax rate was 39.6%, applying to earnings over $400,000. Earnings under $400,000 that year had a lower tax rate of 33% or less.[4]

The marginal tax rate on income can be expressed mathematically as follows:

where t is the total tax liability and i is total income, and ∆ refers to a numerical change. In accounting practice, the tax denominator in the above equation usually includes taxes at federal, state, provincial, and municipal levels. Marginal tax rates are applied to income in countries with progressive taxation schemes, with incremental increases in income taxed in progressively higher tax brackets.

In economics, marginal tax rates are important because they impact the incentive of increased income. With higher marginal tax rates, individuals have less incentive to earn more. This is the basis of the Laffer curve, which theorizes that population-wide taxable income decreases as a function of the marginal tax rate, making net governmental tax revenues decrease beyond a certain taxation point.

With a flat tax, by comparison, all income is taxed at the same percentage, regardless of amount. An example is a sales tax where all purchases are taxed equally. A poll tax is a flat tax of a set dollar amount per person. The marginal tax in these scenarios would be zero.

Implicit marginal tax rate

For individuals that receive means tested benefits, benefits are decreased as more income is earned. This is sometimes described as an implicit tax.[5] These implicit marginal tax rates can exceed 90%[6] or even greater than 100%.[7] Some economists argue that these issues create a disincentive for work or promotion and may result in a structural income inequality.

Effective

The term effective tax rate has different meanings in different contexts. Generally its calculation attempts to adjust a nominal tax rate to make it more meaningful. It may incorporate econometric, estimated, or assumed adjustments to actual data, or may be based entirely on assumptions or simulations.[8]

The term is used in financial reporting to measure the total tax paid as a percentage of the company's accounting income, instead of as a percentage of the taxable income. International Accounting Standard 12,[9] define it as income tax expense or benefit for accounting purposes divided by accounting profit. In Generally Accepted Accounting Principles (United States), the term is used in official guidance only with respect to determining income tax expense for interim (e.g., quarterly) periods by multiplying accounting income by an "estimated annual effective tax rate," the definition of which rate varies depending on the reporting entity's circumstances.[10]

In U.S. income tax law, the term is used in relation to determining whether a foreign income tax on specific types of income exceeds a certain percentage of U.S. tax that would apply on such income if U.S. tax had been applicable to the income.[11]

The popular press, Congressional Budget Office, and various think tanks have used the term to mean varying measures of tax divided by varying measures of income, with little consistency in definition.[12]

Investors usually modify a statutory marginal tax rate to create the effective tax rate appropriate for their decision.

For example: If capital gains are only taxed when realized by a sale, the effective tax rate is the yearly rate that would have applied to the average yearly gain so that the resulting after-tax profit is the same as when all taxed at statutory rates on sale. It will be lower than the statutory rate because unrealized profits are reinvested without tax.

For example: When dividends are both taxed as income, and also generate a tax credit in the UK and Canadian system, the effective tax rate is the net effect of both - the net tax divided by the actual dividend's value.

For example: When contributions are made to Tax Deferred Accounts the reduced tax base will result in reduced taxes calculated at the statutory marginal rate. But the reduction in the tax base may also affect qualification for other government benefits. The difference in those benefits is added to the numerator to increase the effective marginal rate due to the contribution.

Inclusive and exclusive

Tax rates can be presented differently due to differing definitions of tax base, which can make comparisons between tax systems confusing.

Some tax systems include the taxes owed in the tax base (tax-inclusive, Before Tax), while other tax systems do not include taxes owed as part of the base (tax-exclusive, After Tax).[13] In the United States, sales taxes are usually quoted exclusively and income taxes are quoted inclusively. The majority of Europe, value added tax (VAT) countries, include the tax amount when quoting merchandise prices, including Goods and Services Tax (GST) countries, such as Australia and New Zealand. However, those countries still define their tax rates on a tax exclusive basis.

For direct rate comparisons between exclusive and inclusive taxes, one rate must be manipulated to look like the other. When a tax system imposes taxes primarily on income, the tax base is a household's pre-tax income. The appropriate income tax rate is applied to the tax base to calculate taxes owed. Under this formula, taxes to be paid are included in the base on which the tax rate is imposed. If an individual's gross income is $100 and income tax rate is 20%, taxes owed equals $20.

The income tax is taken "off the top", so the individual is left with $80 in after-tax money. Some tax laws impose taxes on a tax base equal to the pre-tax portion of a good's price. Unlike the income tax example above, these taxes do not include actual taxes owed as part of the base. A good priced at $80 with a 25% exclusive sales tax rate yields $20 in taxes owed. Since the sales tax is added "on the top", the individual pays $20 of tax on $80 of pre-tax goods for a total cost of $100. In either case, the tax base of $100 can be treated as two parts—$80 of after-tax spending money and $20 of taxes owed. A 25% exclusive tax rate approximates a 20% inclusive tax rate after adjustment.[13] By including taxes owed in the tax base, an exclusive tax rate can be directly compared to an inclusive tax rate.

- Inclusive income tax rate comparison to an exclusive sales tax rate:

- Let be the income tax rate. For a 20% rate, then

- Let

be the rate in terms of a sales tax.

be the rate in terms of a sales tax. - Let

be the price of the good (including the tax).

be the price of the good (including the tax).

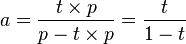

- The revenue that would go to the government:

- The revenue remaining for the seller of the good:

- To convert the tax, divide the money going to the government by the money the company nets:

- Therefore, to adjust any inclusive tax rate to that of an exclusive tax rate, divide the given rate by 1 minus that rate.

- 15% inclusive = 18% exclusive

- 20% inclusive = 25% exclusive

- 25% inclusive = 33% exclusive

- 33% inclusive = 50% exclusive

- 50% inclusive = 100% exclusive

See also

- Progressive tax

- Proportional tax

- Regressive tax

- Tax incidence

- List of countries by tax rates

- List of countries by tax revenue as percentage of GDP

- Tax rates of Europe

- Tax exporting

- Capital flight

References

- ↑ 1.0 1.1 1.2 "What is the difference between statutory, average, marginal, and effective tax rates?". Americans For Fair Taxation. Retrieved 2007-04-23.

- ↑ Piper, Mike (Sep 12, 2014). Taxes Made Simple: Income Taxes Explained in 100 Pages or Less. Simple Subjects, LLC. ISBN 978-0981454214.

- ↑ Reynolds, Alan (2008). "Marginal Tax Rates". In David R. Henderson (ed.). Concise Encyclopedia of Economics (2nd ed.). Indianapolis: Library of Economics and Liberty. ISBN 978-0865976658. OCLC 237794267.

- ↑ William Perez. "Federal Income Tax Rates for the Year 2013". about.com. Retrieved 2013-11-18.

- ↑ http://economix.blogs.nytimes.com/2013/10/28/the-marginal-tax-rate-mess/

- ↑ http://www.cnn.com/2013/02/08/opinion/mccaffery-marginal-tax-rates/

- ↑ https://www.epionline.org/wp-content/studies/shaviro_02-1999.pdf

- ↑ For example, one study provides the caveat that "The effective tax rate calculations utilize information on the median level of assessment within a given geographical area. While a property is likely to be near the median level of assessment, the actual level of assessment for any given property could be greater or lesser than the median."

- ↑ IAS 12, paragraphs 86.

- ↑ ASC 740-270-30-6 through -9.

- ↑ See, e.g., 26 CFR 1.904-4(c).

- ↑ For example, in CBO tables comparing historical tax rates, "Effective tax rates are calculated by dividing taxes by comprehensive household income," where comprehensive household income "equals pretax cash income plus income from other sources. Pretax cash income is the sum of wages, salaries, self-employment income, rents, taxable and nontaxable interest, dividends, realized capital gains, cash transfer payments, and retirement benefits plus taxes paid by businesses (corporate income taxes and the employer's share of Social Security, Medicare, and federal unemployment insurance payroll taxes) and employee contributions to 401(k) retirement plans. Other sources of income include all in-kind benefits (Medicare, Medicaid, employer-paid health insurance premiums, food stamps, school lunches and breakfasts, housing assistance, and energy assistance). Households with negative income are excluded from the lowest income category but are included in totals." This CBO definition includes in income many items, such as employer share of Social Security tax, not considered income for most purposes. In a different context, CBO uses the term to include total Federal corporate income taxes imputed to individuals based on the assumed level of corporate shareholdings for a class of individuals.

- ↑ 13.0 13.1 Bachman, Paul; Haughton, Jonathan; Kotlikoff, Laurence J.; Sanchez-Penalver, Alfonso; Tuerck, David G. (November 2006). "Taxing Sales under the FairTax – What Rate Works?". Beacon Hill Institute. Tax Analysts. Retrieved 2007-04-24.

External links

| Wikimedia Commons has media related to Marginal tax rates. |