Lomax distribution

| Parameters |

shape (real) shape (real) |

|---|---|

| Support |

|

![{\alpha \over \lambda} \left[{1+ {x \over \lambda}}\right]^{-(\alpha+1)}](../I/m/0736a202d2554f581160ca8717f1ceb7.png) | |

| CDF |

![1- \left[{1+ {x \over \lambda}}\right]^{-\alpha}](../I/m/90e6e43b7e320b4d54b2e6c74ec67de2.png) |

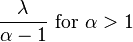

| Mean |

Otherwise undefined |

| Median |

![\lambda (\sqrt[\alpha]{2} - 1)](../I/m/bfe5d9e3d27049719646b10e15644dcc.png) |

| Mode | 0 |

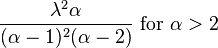

| Variance |

Otherwise undefined |

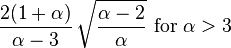

| Skewness |

|

| Ex. kurtosis |

|

The Lomax distribution, conditionally also called the Pareto Type II distribution, is a heavy-tail probability distribution often used in business, economics, and actuarial modeling.[1][2] It is named after K. S. Lomax. It is essentially a Pareto distribution that has been shifted so that its support begins at zero.[3]

Characterization

Probability density function

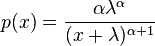

The probability density function (pdf) for the Lomax distribution is given by

![p(x) = {\alpha \over \lambda} \left[{1+ {x \over \lambda}}\right]^{-(\alpha+1)}, \qquad x \geq 0,](../I/m/db9f9896afe353eb6bca5832d6cd5940.png)

with shape parameter and scale parameter  . The density can be rewritten in such a way that more clearly shows the relation to the Pareto Type I distribution. That is:

. The density can be rewritten in such a way that more clearly shows the relation to the Pareto Type I distribution. That is:

.

.

Differential equation

The pdf of the Lomax distribution is a solution to the following differential equation:

Relation to the Pareto distribution

The Lomax distribution is a Pareto Type I distribution shifted so that its support begins at zero. Specifically:

The Lomax distribution is a Pareto Type II distribution with xm=λ and μ=0:[4]

Relation to generalized Pareto distribution

The Lomax distribution is a special case of the generalized Pareto distribution. Specifically:

Relation to q-exponential distribution

The Lomax distribution is a special case of the q-exponential distribution. The q-exponential extends this distribution to support on a bounded interval. The Lomax parameters are given by:

Non-central moments

The  th non-central moment

th non-central moment ![E[X^\nu]](../I/m/4abb67e3766516b7e9ff27cd0a15c9d3.png) exists only if the shape parameter

exists only if the shape parameter  strictly exceeds , when the moment has the value

strictly exceeds , when the moment has the value

See also

References

- ↑ Lomax, K. S. (1954) "Business Failures; Another example of the analysis of failure data". Journal of the American Statistical Association, 49, 847–852. JSTOR 2281544

- ↑ Johnson, N.L., Kotz, S., Balakrishnan, N. (1994) Continuous Univariate Distributions, Volume 1, 2nd Edition, Wiley. ISBN 0-471-58495-9 (pages 575, 602)

- ↑ Van Hauwermeiren M and Vose D (2009). A Compendium of Distributions [ebook]. Vose Software, Ghent, Belgium. Available at www.vosesoftware.com. Accessed 07/07/11

- ↑ Kleiber, Christian; Kotz, Samuel (2003), Statistical Size Distributions in Economics and Actuarial Sciences, Wiley Series in Probability and Statistics 470, John Wiley & Sons, p. 60, ISBN 9780471457169.