Girsanov theorem

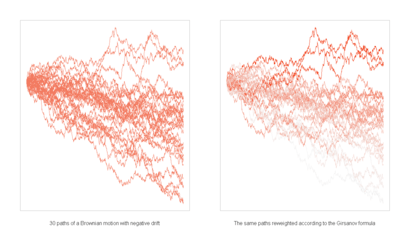

In probability theory, the Girsanov theorem (named after Igor Vladimirovich Girsanov) describes how the dynamics of stochastic processes change when the original measure is changed to an equivalent probability measure.[1]:607 The theorem is especially important in the theory of financial mathematics as it tells how to convert from the physical measure which describes the probability that an underlying instrument (such as a share price or interest rate) will take a particular value or values to the risk-neutral measure which is a very useful tool for pricing derivatives on the underlying.

History

Results of this type were first proved by Cameron–Martin in the 1940s and by Girsanov in 1960. They have been subsequently extended to more general classes of process culminating in the general form of Lenglart (1977).

Significance

Girsanov's theorem is important in the general theory of stochastic processes since it enables the key result that if Q is a measure absolutely continuous with respect to P then every P-semimartingale is a Q-semimartingale.

Statement of theorem

We state the theorem first for the special case when the underlying stochastic process is a Wiener process. This special case is sufficient for risk-neutral pricing in the Black-Scholes model and in many other models (e.g. all continuous models).

Let  be a Wiener process on the Wiener probability space

be a Wiener process on the Wiener probability space  . Let

. Let  be a measurable process adapted to the natural filtration of the Wiener process

be a measurable process adapted to the natural filtration of the Wiener process  .

.

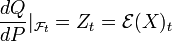

Given an adapted process with  define

define

where  is the stochastic exponential (or Doléans exponential) of X with respect to W, i.e.

is the stochastic exponential (or Doléans exponential) of X with respect to W, i.e.

![\mathcal{E}(X)_t=\exp \left ( X_t - \frac{1}{2} [X]_t \right ),](../I/m/9ee3a84d37dc5d1d850856e967f16d72.png)

where ![[X]_t](../I/m/b09ede298b85f6af03c182d75a6497be.png) is a quadratic variation for . If

is a quadratic variation for . If  is a strictly positive martingale, a probability

measure Q can be defined on

is a strictly positive martingale, a probability

measure Q can be defined on  such that we have Radon–Nikodym derivative

such that we have Radon–Nikodym derivative

Then for each t the measure Q restricted to the unaugmented sigma fields  is equivalent to P restricted to

is equivalent to P restricted to

Furthermore if Y is a local martingale under P then the process

![\tilde Y_t = Y_t - \left[ Y,X \right]_t](../I/m/b19819ff9bc30e43dcbf90a340dfa629.png)

is a Q local martingale on the filtered probability space  .

.

Corollary

If X is a continuous process and W is Brownian motion under measure P then

![\tilde W_t =W_t - \left [ W, X \right]_t](../I/m/e2a1fcd630586691ee2292cc206f9023.png)

is Brownian motion under Q.

The fact that  is continuous is trivial; by Girsanov's theorem it is a Q local martingale, and by computing the quadratic variation

is continuous is trivial; by Girsanov's theorem it is a Q local martingale, and by computing the quadratic variation

![\left[\tilde W \right]_t=

\left[W_t, W_t\right] - 2 \left[W_t, [W, X]_t\right] + \left[[W, X]_t, [W, X]_t \right] = \left [ W \right]_t = t](../I/m/fd730dee4d4554fa7c1aa5d9a959a491.png)

it follows by Lévy's characterization of Brownian motion that this is a Q Brownian motion.

Comments

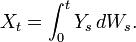

In many common applications, the process X is defined by

For X of this form then a sufficient condition for to be a martingale is Novikov's condition which requires that

![E_P\left [\exp\left (\frac{1}{2}\int_0^T Y_s^2\, ds\right )\right ] < \infty.](../I/m/86920c2a504d7394b6eb2621ffa7d08a.png)

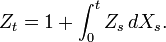

The stochastic exponential is the process Z which solves the stochastic differential equation

The measure Q constructed above is not equivalent to P on  as this would only be the case if the Radon–Nikodym derivative were a uniformly integrable martingale, which the exponential martingale described above is not (for

as this would only be the case if the Radon–Nikodym derivative were a uniformly integrable martingale, which the exponential martingale described above is not (for  ).

).

Application to finance

In finance, Girsanov theorem is used each time one needs to derive an asset's or rate's dynamics under a new probability measure. The most well known case is moving from historic measure P to risk neutral measure Q which is done - in Black Scholes framework - via Radon–Nikodym derivative:

where  denotes the instantaneous risk free rate,

denotes the instantaneous risk free rate,  the asset's drift and

the asset's drift and  its volatility.

its volatility.

Other classical applications of Girsanov theorem are quanto adjustments and the calculation of forwards' drifts under LIBOR market model.

See also

References

- C. Dellacherie and P.-A. Meyer, "Probabilités et potentiel -- Théorie de Martingales" Chapitre VII, Hermann 1980

- Girsanov, I. V., "On transforming a certain class of stochastic processes by absolutely continuous substitution of measures", Theory of Probability and its Applications, 1960

- E. Lenglart "Transformation de martingales locales par changement absolue continu de probabilités", Zeitschrift für Wahrscheinlichkeit 39 (1977) pp 65–70.

External links

- ↑ M. Musiela, M. Rutkowski: Martingale methods in financial modelling. 2nd ed. New York : Springer-Verlag, 2004. Print.

- Notes on Stochastic Calculus which contains a simple outline proof of Girsanov's theorem.

- Applied Multidimensional Girsanov Theorem which contains financial applications of Girsanov's theorem.