Exponential discounting

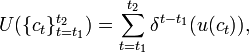

In economics exponential discounting is a specific form of the discount function, used in the analysis of choice over time (with or without uncertainty). Formally, exponential discounting occurs when total utility is given by

where ct is consumption at time t,  is the exponential discount factor, and u is the instantaneous utility function.

is the exponential discount factor, and u is the instantaneous utility function.

In continuous time, exponential discounting is given by

Exponential discounting implies that the marginal rate of substitution between consumption at any pair of points in time depends only on how far apart those two points are. Exponential discounting is not dynamically inconsistent.

For its simplicity, the exponential discounting assumption is the most commonly used in economics. However, alternatives like hyperbolic discounting have more empirical support.