Beta (finance)

In finance, the beta (β) of an investment is a measure of the risk arising from exposure to general market movements as opposed to idiosyncratic factors. The market portfolio of all investable assets has a beta of exactly 1. A beta below 1 can indicate either an investment with lower volatility than the market, or a volatile investment whose price movements are not highly correlated with the market. An example of the first is a treasury bill: the price does not go up or down a lot, so it has a low beta. An example of the second is gold. The price of gold does go up and down a lot, but not in the same direction or at the same time as the market.[1]

A beta above one generally means that the asset both is volatile and tends to move up and down with the market. An example is a stock in a big technology company. Negative betas are possible for investments that tend to go down when the market goes up, and vice versa. There are few fundamental investments with consistent and significant negative betas, but some derivatives like equity put options can have large negative betas.[2]

Beta is important because it measures the risk of an investment that cannot be diversified away. It does not measure the risk of an investment held on a stand-alone basis, but the amount of risk the investment adds to an already-diversified portfolio. In the capital asset pricing model, beta risk is the only kind of risk for which investors should receive an expected return higher than the risk-free rate of interest.[3]

The definition above covers only theoretical beta. The term is used in many related ways in finance. For example, the betas commonly quoted in mutual fund analyses generally measure the risk of the fund arising from exposure to a benchmark for the fund, rather than from exposure to the entire market portfolio. Thus they measure the amount of risk the fund adds to a diversified portfolio of funds of the same type, rather than to a portfolio diversified among all fund types.[4]

Beta decay refers to the tendency for a company with a high beta coefficient (β > 1) to have its beta coefficient decline to the market beta. It is an example of regression toward the mean.

Statistical estimation

Beta is estimated by linear regression. Given an asset and a benchmark that we are interested in, we want to find an approximate formula

where ra is the return of the asset and rb is return of the benchmark.

Since the data are usually in the form of time series, the statistical model is

,

,

where εt is an error term (the unexplained return). Click here for a definition of Alpha (α).

The best (in the sense of least squared error) estimates for α and β are those such that Σεt2 is as small as possible.

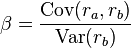

A common expression for beta is

,

,

where Cov and Var are the covariance and variance operators.

This can also be expressed as

where ρa,b is the correlation of the two returns, and σa and σb are the respective volatilities.

- σa=√[Var(ra)], σb=√[Var(rb)], ρa,b=Cov(ra, rb)/√[Var(ra)·Var(rb)]

Beta can be computed for prices in the past, where the data is known, which is historical beta. However, what most people are interested in is future beta, which relates to risks going forward. Estimating future beta is a difficult problem. One guess is that future beta equals historical beta.

From this, we find that beta can be explained as "correlated relative volatility". This has three components:

- correlated

- relative

- volatility

Beta is also referred to as financial elasticity or correlated relative volatility, and can be referred to as a measure of the sensitivity of the asset's returns to market returns, its non-diversifiable risk, its systematic risk, or market risk. On an individual asset level, measuring beta can give clues to volatility and liquidity in the marketplace. In fund management, measuring beta is thought to separate a manager's skill from his or her willingness to take risk.

The portfolio of interest in the CAPM formulation is the market portfolio that contains all risky assets, and so the rb terms in the formula are replaced by rm, the rate of return of the market. The regression line is then called the security characteristic line (SCL).

is called the asset's alpha and

is called the asset's alpha and  is called the asset's beta coefficient. Both coefficients have an important role in modern portfolio theory.

is called the asset's beta coefficient. Both coefficients have an important role in modern portfolio theory.

For example, in a year where the broad market or benchmark index returns 25% above the risk free rate, suppose two managers gain 50% above the risk free rate. Because this higher return is theoretically possible merely by taking a leveraged position in the broad market to double the beta so it is exactly 2.0, we would expect a skilled portfolio manager to have built the outperforming portfolio with a beta somewhat less than 2, such that the excess return not explained by the beta is positive. If one of the managers' portfolios has an average beta of 3.0, and the other's has a beta of only 1.5, then the CAPM simply states that the extra return of the first manager is not sufficient to compensate us for that manager's risk, whereas the second manager has done more than expected given the risk. Whether investors can expect the second manager to duplicate that performance in future periods is of course a different question.

Security market line

The Security Market Line |

The SML graphs the results from the capital asset pricing model (CAPM) formula. The x-axis represents the risk (beta), and the y-axis represents the expected return. The market risk premium is determined from the slope of the SML.

The relationship between β and required return is plotted on the security market line (SML) which shows expected return as a function of β. The intercept is the nominal risk-free rate available for the market, while the slope is E(Rm)− Rf. The security market line can be regarded as representing a single-factor model of the asset price, where Beta is exposure to changes in value of the Market. The equation of the SML is thus:

It is a useful tool in determining if an asset being considered for a portfolio offers a reasonable expected return for risk. Individual securities are plotted on the SML graph. If the security's risk versus expected return is plotted above the SML, it is undervalued because the investor can expect a greater return for the inherent risk. A security plotted below the SML is overvalued because the investor would be accepting a lower return for the amount of risk assumed.

Choice of benchmark

In the U.S., published betas typically use a stock market index such as the S&P 500 as a benchmark. The S&P 500 is a popular index of U.S. large-cap stocks. Other choices may be an international index such as the MSCI EAFE. The benchmark is often chosen to be similar to the assets chosen by the investor. For example, for a person who owns S&P 500 index funds and gold bars, the index would combine the S&P 500 and the price of gold. In practice a standard index is used.

The choice of the index need not reflect the portfolio under question; e.g., beta for gold bars compared to the S&P 500 may be low or negative carrying the information that gold does not track stocks and may provide a mechanism for reducing risk. The restriction to stocks as a benchmark is somewhat arbitrary. A model portfolio may be stocks plus bonds. Sometimes the market is defined as "all investable assets" (see Roll's critique); unfortunately, this includes lots of things for which returns may be hard to measure.

Investing

By definition, the market itself has a beta of 1.0, and individual stocks are ranked according to how much they deviate from the macro market (for simplicity purposes, the S&P 500 is sometimes used as a proxy for the market as a whole). A stock whose returns vary more than the market's returns over time can have a beta whose absolute value is greater than 1.0 (whether it is, in fact, greater than 0 will depend on the correlation of the stock's returns and the market's returns). A stock whose returns vary less than the market's returns has a beta with an absolute value less than 1.0.

A stock with a beta of 2 has returns that change, on average, by twice the magnitude of the overall market's returns; when the market's return falls or rises by 3%, the stock's return will fall or rise (respectively) by 6% on average. (However, because beta also depends on the correlation of returns, there can be considerable variance about that average; the higher the correlation, the less variance; the lower the correlation, the higher the variance.) Beta can also be negative, meaning the stock's returns tend to move in the opposite direction of the market's returns. A stock with a beta of −3 would see its return decline 9% (on average) when the market's return goes up 3%, and would see its return climb 9% (on average) if the market's return falls by 3%.

Higher-beta stocks tend to be more volatile and therefore riskier, but provide the potential for higher returns. Lower-beta stocks pose less risk but generally offer lower returns. Some have challenged this idea, claiming that the data show little relation between beta and potential reward, or even that lower-beta stocks are both less risky and more profitable (contradicting CAPM).[5] In the same way a stock's beta shows its relation to market shifts, it is also an indicator for required returns on investment (ROI). Given a risk-free rate of 2%, for example, if the market (with a beta of 1) has an expected return of 8%, a stock with a beta of 1.5 should return 11% (= 2% + 1.5(8% − 2%)) in accordance with the financial CAPM model.

Adding to a portfolio

Suppose an investor has all his money in an asset class X and wishes to move a small amount to an asset class Y. For example, X could be U.S. stocks, while Y could be stocks of a different country, or bonds. Then the new portfolio, Z, can be expressed symbolically

The variance can be computed as

which can be simplified by ignoring δ2 terms:

The first formula is exact, while the second one is only valid for small δ. Using the formula for β of Y relative to X,

we can compute

This suggests that an asset with β greater than one will increase variance, while an asset with β less than one will decrease variance, if added in the right amount. This assumes that variance is an accurate measure of risk, which is usually good. However, the beta does need to be computed with respect to what the investor currently owns.

Academic theory

Academic theory claims that higher-risk investments should have higher returns over the long-term. Wall Street has a saying that "higher return requires higher risk", not that a risky investment will automatically do better. Some things may just be poor investments (e.g., playing roulette). Further, highly rational investors should consider correlated volatility (beta) instead of simple volatility (sigma). Theoretically, a negative beta equity is possible; for example, an inverse ETF should have negative beta to the relevant index. Also, a short position should have opposite beta.

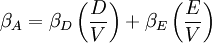

This expected return on equity, or equivalently, a firm's cost of equity, can be estimated using the capital asset pricing model (CAPM). According to the model, the expected return on equity is a function of a firm's equity beta (βE) which, in turn, is a function of both leverage and asset risk (βA):

where:

- KE = firm's cost of equity

- RF = risk-free rate (the rate of return on a "risk free investment"; e.g., U.S. Treasury Bonds)

- RM = return on the market portfolio

-

![\beta_E = \beta =\left[ \beta_A - \beta_D \left(\frac {D}{V}\right) \right] \frac {V}{E}](../I/m/886efee7ec7edade19175a572534f9a7.png)

because:

and

- Firm value (V) + cash and risk-free securities = debt value (D) + equity value (E)

An indication of the systematic riskiness attaching to the returns on ordinary shares. It equates to the asset Beta for an ungeared firm, or is adjusted upwards to reflect the extra riskiness of shares in a geared firm., i.e. the Geared Beta.[6]

Multiple beta model

The arbitrage pricing theory (APT) has multiple betas in its model. In contrast to the CAPM that has only one risk factor, namely the overall market, APT has multiple risk factors. Each risk factor has a corresponding beta indicating the responsiveness of the asset being priced to that risk factor.

Multiple-factor models contradict CAPM by claiming that some other factors can influence return, therefore one may find two stocks (or funds) with equal beta, but one may be a better investment.

Estimation of beta

To estimate beta, one needs a list of returns for the asset and returns for the index; these returns can be daily, weekly or any period. Then one uses standard formulas from linear regression. The slope of the fitted line from the linear least-squares calculation is the estimated Beta. The y-intercept is the alpha.

Myron Scholes and Joseph Williams (1977) provided a model for estimating betas from nonsynchronous data.[7]

Beta specifically gives the volatility ratio multiplied by the correlation of the plotted data. To take an extreme example, something may have a beta of zero even though it is highly volatile, provided it is uncorrelated with the market. Tofallis (2008) provides a discussion of this,[8] together with a real example involving AT&T Inc. The graph showing monthly returns from AT&T is visibly more volatile than the index and yet the standard estimate of beta for this is less than one.

The relative volatility ratio described above is actually known as Total Beta (at least by appraisers who practice business valuation). Total beta is equal to the identity: beta/R or the standard deviation of the stock/standard deviation of the market (note: the relative volatility). Total beta captures the security's risk as a stand-alone asset (because the correlation coefficient, R, has been removed from beta), rather than part of a well-diversified portfolio. Because appraisers frequently value closely held companies as stand-alone assets, total beta is gaining acceptance in the business valuation industry. Appraisers can now use total beta in the following equation: total cost of equity (TCOE) = risk-free rate + total beta·equity risk premium. Once appraisers have a number of TCOE benchmarks, they can compare/contrast the risk factors present in these publicly traded benchmarks and the risks in their closely held company to better defend/support their valuations.

Interpretations of Beta

Some interpretations of beta are explained in the following table:[9]

| Value of Beta | Interpretation | Example |

|---|---|---|

| β < 0 | Asset generally moves in the opposite direction as compared to the index | An inverse exchange-traded fund or a short position |

| β = 0 | Movement of the asset is uncorrelated with the movement of the benchmark | Fixed-yield asset, whose growth is unrelated to the movement of the stock market |

| 0 < β < 1 | Movement of the asset is generally in the same direction as, but less than the movement of the benchmark | Stable, "staple" stock such as a company that makes soap. Moves in the same direction as the market at large, but less susceptible to day-to-day fluctuation. |

| β = 1 | Movement of the asset is generally in the same direction as, and about the same amount as the movement of the benchmark | A representative stock, or a stock that is a strong contributor to the index itself. |

| β > 1 | Movement of the asset is generally in the same direction as, but more than the movement of the benchmark | Stocks which are very strongly influenced by day-to-day market news, or by the general health of the economy. |

It measures the part of the asset's statistical variance that cannot be removed by the diversification provided by the portfolio of many risky assets, because of the correlation of its returns with the returns of the other assets that are in the portfolio. Beta can be estimated for individual companies using regression analysis against a stock market index. An alternative to standard beta is downside beta.

Beta is always measured in respect to some benchmark. Therefore an asset may have different betas depending on which benchmark is used. Just a number is useless if the benchmark is not known.

Extreme and interesting cases

- Beta has no upper or lower bound, and betas as large as 3 or 4 will occur with highly volatile stocks.

- Beta can be zero. Some zero-beta assets are risk-free, such as treasury bonds and cash. However, simply because a beta is zero does not mean that it is risk-free. A beta can be zero simply because the correlation between that item's returns and the market's returns is zero. An example would be betting on horse racing. The correlation with the market will be zero, but it is certainly not a risk-free endeavor.

- On the other hand, if a stock has a moderately low but positive correlation with the market, but a high volatility, then its beta may still be high.

- A negative beta simply means that the stock is inversely correlated with the market.

- A negative beta might occur even when both the benchmark index and the stock under consideration have positive returns. It is possible that lower positive returns of the index coincide with higher positive returns of the stock, or vice versa. The slope of the regression line in such a case will be negative.

- Using beta as a measure of relative risk has its own limitations. Most analyses consider only the magnitude of beta. Beta is a statistical variable and should be considered with its statistical significance (R square value of the regression line). Higher R square value implies higher correlation and a stronger relationship between returns of the asset and benchmark index.

- If beta is a result of regression of one stock against the market where it is quoted, betas from different countries are not comparable.

- Utility stocks commonly show up as examples of low beta. These have some similarity to bonds, in that they tend to pay consistent dividends, and their prospects are not strongly dependent on economic cycles. They are still stocks, so the market price will be affected by overall stock market trends, even if this does not make sense.

- Staple stocks are thought to be less affected by cycles and usually have lower beta. Procter & Gamble, which makes soap, is a classic example. Other similar ones are Philip Morris (tobacco) and Johnson & Johnson (Health & Consumer Goods).

- 'Tech' stocks are commonly equated with higher beta. This is based on experience of the dot-com bubble around year 2000. Although tech did very well in the late 1990s, it also fell sharply in the early 2000s, much worse than the decline of the overall market. More recently, this is not a good example.

- During the 2008 market fall, finance stocks did very poorly, much worse than the overall market. Then in the following years they gained the most, although not to make up for their losses. They are still higher beta.

- Foreign stocks may provide some diversification. World benchmarks such as S&P Global 100 have slightly lower betas than comparable US-only benchmarks such as S&P 100. However, this effect is not as good as it used to be; the various markets are now fairly correlated, especially the US and Western Europe.

- Derivatives and other non-linear assets. Beta relies on a linear model. An out of the money option may have a distinctly non-linear payoff. The change in price of an option relative to the change in the price of the underlying asset (for example a stock) is not constant. For example, if one purchased a put option on the S&P 500, the beta would vary as the price of the underlying index (and indeed as volatility, time to expiration and other factors) changed. (see options pricing, and Black–Scholes model).

Criticism

Seth Klarman of the Baupost group wrote in Margin of Safety: "I find it preposterous that a single number reflecting past price fluctuations could be thought to completely describe the risk in a security. Beta views risk solely from the perspective of market prices, failing to take into consideration specific business fundamentals or economic developments. The price level is also ignored, as if IBM selling at 50 dollars per share would not be a lower-risk investment than the same IBM at 100 dollars per share. Beta fails to allow for the influence that investors themselves can exert on the riskiness of their holdings through such efforts as proxy contests, shareholder resolutions, communications with management, or the ultimate purchase of sufficient stock to gain corporate control and with it direct access to underlying value. Beta also assumes that the upside potential and downside risk of any investment are essentially equal, being simply a function of that investment's volatility compared with that of the market as a whole. This too is inconsistent with the world as we know it. The reality is that past security price volatility does not reliably predict future investment performance (or even future volatility) and therefore is a poor measure of risk."[10]

At the industry level, beta tends to underestimate downside beta two-thirds of the time (resulting in value overestimation) and overestimate upside beta one-third of the time resulting in value underestimation.[11]

Another weakness of beta can be illustrated through an easy example by considering two hypothetical stocks, A and B. The returns on A, B and the market follow the probability distribution below:

| Probability | Market | Stock A | Stock B |

|---|---|---|---|

| 0.25 | −30% | −15% | −60% |

| 0.25 | −15% | −7.5% | −30% |

| 0.25 | 15% | 30% | 7.5% |

| 0.25 | 30% | 60% | 15% |

The table shows that stock A goes down half as much as the market when the market goes down and up twice as much as the market when the market goes up. Stock B, on the other hand, goes down twice as much as the market when the market goes down and up half as much as the market when the market goes up. Most investors would label stock B as more risky. In fact, stock A has better return in every possible case. However, according to the capital asset pricing model, stock A and B would have the same beta, meaning that theoretically, investors would require the same rate of return for both stocks. This is an illustration of how using standard beta might mislead investors. The dual-beta model, in contrast, takes into account this issue and differentiates downside beta from upside beta, or downside risk from upside risk, and thus allows investors to make better informed investing decisions.[11]

See also

References

- ↑ Sharpe, William (1970). Portfolio Theory and Capital Markets. McGraw-Hill Trade. ISBN 978-0071353205.

- ↑ Markowitz, Harry (1958). Portfolio Selection. John Wiley & Sons. ISBN 978-1557861085.

- ↑ Fama, Eugene (1976). Foundations of Finance: Portfolio Decisions and Securities Prices. Basic Books. ISBN 978-0465024995.

- ↑ Ilmanen, Antti (2011). Expected Returns: An Investor's Guide to Harvesting Market Rewards. John Wiley & Sons. ISBN 978-1119990727.

- ↑ McAlpine, Chad (2010). "Low-risk TSX stocks have outearned riskiest peers over 30-year period", The Financial Post Trading Desk, June 22, 2010

- ↑ "Click here definition of Equity Beta, what is Equity Beta, what does Equity Beta mean? Finance Glossary - Search our financial terms for a definition - London South East". Lse.co.uk. Retrieved 2012-12-03.

- ↑ Scholes, Myron; Williams, Joseph (1977). "Estimating betas from nonsynchronous data". Journal of Financial Economics 5 (3): 309–327. doi:10.1016/0304-405X(77)90041-1.

- ↑ Tofallis, Chris (2008). "Investment Volatility: A Critique of Standard Beta Estimation and a Simple Way Forward". European Journal of Operational Research 187 (3): 1358–1367. doi:10.1016/j.ejor.2006.09.018.

- ↑ Definition of Beta Definition via Wikinvest

- ↑ Klarman, Seth; Williams, Joseph (1991). "Beta". Journal of Financial Economics 5 (3): 117. doi:10.1016/0304-405X(77)90041-1.

- ↑ 11.0 11.1 James Chong; Yanbo Jin; Michael Phillips (April 29, 2013). "The Entrepreneur's Cost of Capital: Incorporating Downside Risk in the Buildup Method". Retrieved 25 June 2013.

External links

- ETFs & Diversification: A Study of Correlations

- Leverage and diversification effects of public companies

- Calculate Beta in a Spreadsheet