Risk parity

Risk parity (or risk premia parity) is an approach to investment portfolio management which focuses on allocation of risk, usually defined as volatility, rather than allocation of capital. The risk parity approach asserts that when asset allocations are adjusted (leveraged or deleveraged) to the same risk level, the risk parity portfolio can achieve a higher Sharpe ratio and can be more resistant to market downturns than the traditional portfolio.

Risk parity can also be a generalized term that denotes a variety of investment systems and techniques that utilize its principles.[1] The principles of risk parity are applied differently according to the investment style and goals of various financial managers and yield different results.

Some of its theoretical components were developed in the 1950s and 1960s but the first risk parity fund, called the All Weather fund, was pioneered in 1996. In recent years many investment companies have begun offering risk parity funds to their clients. The term, risk parity, came into use in 2005 and was then adopted by the asset management industry. Risk parity can be seen as either a passive or active management strategy.

Interest in the risk parity approach has increased since the late 2000s financial crisis as the risk parity approach fared better than traditionally constructed portfolios, as well as many hedge funds.[2][3] Some portfolio managers have expressed skepticism about the practical application of the concept and its effectiveness in all types of market conditions[4][5] but others point to its performance during the financial crisis of 2007-2008 as an indication of its potential success.[6][7]

Description

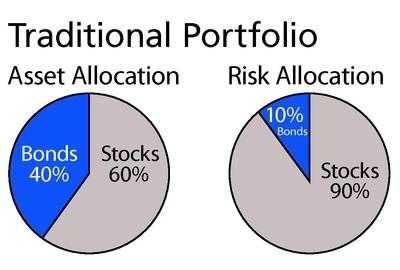

Risk parity is a conceptual approach to investing which attempts to provide a lower risk and lower fee alternative to the traditional portfolio allocation of 60% stocks and 40% bonds which carries 90% of its risk in the stock portion of the portfolio (see illustration).[8][9] The risk parity approach attempts to equalize risk by allocating funds to a wider range of categories such as stocks, government bonds, credit-related securities and inflation hedges (including real assets, commodities, real estate and inflation-protected bonds), while maximizing gains through financial leveraging.[10][11] According to Bob Prince, CIO at Bridgewater Associates, the defining parameters of a traditional risk parity portfolio are uncorrelated assets, low equity risk, and passive management.[12]

Some scholars contend that a risk parity portfolio requires strong management and continuous oversight to reduce the potential for negative consequences as a result of leverage and allocation building in the form of buying and selling of assets to keep dollar holdings at predetermined and equalized risk levels. For example, if the price of a security goes up or down and risk levels remain the same, the risk parity portfolio will be adjusted to keep its dollar exposure constant.[13] On the other hand some consider risk parity to be a passive approach, because it does not require the portfolio manager to buy or sell securities on the basis of judgments about future market behavior.[14]

The principles of risk parity may be applied differently by different financial managers, as they have different methods for categorizing assets into classes, different definitions of risk, different ways of allocating risk within asset classes, different methods for forecasting future risk and different ways of implementing exposure to risk.[15] However, many risk parity funds evolve away from their original intentions, including passive management. The extent to which a risk parity portfolio is managed, is often the distinguishing characteristic between the various kinds of risk parity funds available today.[12]

History

The seeds for the risk parity approach were sown when economist and Nobel Prize winner, Harry Markowitz introduced the concept of the efficient frontier into modern portfolio theory in 1952. Then in 1958, Nobel laureate James Tobin concluded that the efficient frontier model could be improved by adding risk-free investments and he advocated leveraging a diversified portfolio to improve its risk/return ratio.[14] The theoretical analysis of combining leverage and minimizing risk amongst multiple assets in a portfolio was also examined by Jack Treynor in 1961, William Sharpe in 1964, John Lintner in 1965 and Jan Mossin in 1966. However, the concept was not put into practice due to the difficulties of implementing leverage in the portfolio of a large institution.[16]

According to Joe Flaherty, senior vice president at MFS Investment Management, "the idea of risk parity goes back to the 1990s". In 1996, Bridgewater Associates launched a risk parity fund called the All Weather asset allocation strategy.[2][12][17][18] Although Bridgewater Associates was the first to bring a risk parity product to market, they did not coin the term. Instead the term, risk parity was first used by Edward Qian, of PanAgora Asset Management, when he authored a white paper in 2005. In 2008 the name Risk Parity (short for Risk Premia Parity) was given to this portfolio investment category by Andrew Zaytsev at the investment consulting firm Alan Biller and Associates. Soon, the term was adopted by the asset management industry.[17][19] In time, other firms such as Aquila Capital (2004), Northwater, Wellington, Invesco, First Quadrant, Putnam Investments, ATP (2006), PanAgora Asset Management (2006), 1741 Asset Management (2009), Neuberger Berman (2009), AllianceBernstein (2010),[20] AQR Capital Management (2010),[21] Clifton Group (2011),[22] Salient Partners (2012)[23][24][25] and Schroders (2012) began establishing risk parity funds.[17][26][27]

Performance

A white paper report from Callan Investments Institute Research in Feb 2010 reported that a "levered Risk Parity portfolio would have significantly underperformed" versus a standard institutional portfolio in the 1990s but "would have significantly outperformed" a standard institutional portfolio during the decade of 2000 to 2010.[28] According to a 2010 article in the Wall Street Journal "Risk-parity funds held up relatively well during the financial crisis" of 2008. For example AQR's risk parity fund declined 18% to 19% in 2008 compared with the 22% decline in the Vanguard Balanced Index fund.[29] According to a 2013 Wall Street Journal report the risk parity type of fund offered by hedge funds has "soared in popularity" and "consistently outperformed traditional strategies since the financial crisis".[30] However, mutual funds using the risk parity strategy were reported to have incurred losses of 6.75% during the first half of the year.[30]

Reception

With the bullish stock market of the 1990s, equity-heavy investing approaches outperformed risk parity in the near term.[31] However after the March 2000 crash, there was an increased interest in risk parity, first among institutional investors in the United States and then in Europe.[2][3] USA investors include the Wisconsin State Investment Board which has invested hundreds of millions in the risk parity funds of AQR and Bridgewater Associates.[32][33][34][35] The financial crisis of 2007-2010 was also hard on equity-heavy and Yale Model portfolios,[36] but risk parity funds fared reasonably well.[6][7][37][38]

According to a 2011 article in Investments & Pensions Europe, the risk parity approach has "moderate risks" which include: communicating its value to boards of directors; unforeseen events like the 2008 market decline; market timing risks associated with implementation; the use of leverage and derivatives and basis risks associated with derivatives.[4] Other critics warn that the use of leverage and relying heavily on fixed income assets may create its own risk.[39][40][41] Portfolio manager, Ben Inker has criticized risk parity for being a benchmarking approach that gives too much relative weight to bonds when compared to other alternative portfolio approaches. However, proponents of risk parity say that its purpose is to avoid predicting future returns.[42][43][44] Inker also says that risk parity requires too much leverage to produce the same expected returns as conventional alternatives. Proponents answer that the reduced risk from additional diversification more than offsets the additional leverage risk and that leverage through publicly traded futures and prime brokerage financing of assets also means a high percentage of cash in the portfolio to cover losses and margin calls.[36] Additionally Inker says that bonds have negative skew, (small probability of large losses and large probability of small gains) which makes them a dangerous investment to leverage. Proponents have countered by saying that their approach calls for reduced exposure to bonds as volatility increases and provides less skew than conventional portfolios.[45]

Risk parity advocates assert that the unlevered risk parity portfolio, is quite close to the tangency portfolio, as close as can be measured given uncertainties and noise in the data.[46] Theoretical and empirical arguments are made in support of this contention. One specific set of assumptions that puts the risk parity portfolio on the efficient frontier is that the individual asset classes are uncorrelated and have identical Sharpe ratios.[35] Risk parity critics rarely contest the claim that the risk parity portfolio is near the tangency portfolio but they say that the leveraged investment line is less steep and that the levered risk parity portfolio has slight or no advantage over 60% stocks / 40% bonds, and carries the disadvantage of greater explicit leverage.[5][43]

Despite criticisms from skeptics, the risk parity approach has seen a "flurry of activity" following a decade of "subpar equity performance".[47] During the period 2005 to 2012 several companies began offering risk parity products including: Barclays Global Investors, Schroders, First Quadrant, Mellon Capital Management, Neuberger Berman and State Street Global Advisors.[48] A 2011 survey of institutional investors and consultants suggests that over 50% of America-based benefit pension and endowments and foundations are currently using, or considering, risk parity products for their investment portfolios.[49] Companies like AQR Capital and Bridgewater Associates have attracted clients such as the Wisconsin State Investment Board, The Pennsylvania Public Schools Employees’ Retirement System and the Alaska Permanent Fund Corp to their risk parity funds.[2][12][43][50] A 2012 article in the Financial Times indicated possible challenges for risk parity funds "at the peak of a 30-year bull market for fixed income". While advocates point out their diversification amongst bonds as well as "inflation-linked securities, corporate credit, emerging market debt, commodities and equities, balanced by how each asset class responds to two factors: changes in the expected rate of economic growth and changes to expectations for inflation".[47] A 2013 article in the Financial News reported that "risk parity continues to prosper, as investors come to appreciate the better balance of different risks that it represents in an uncertain world."[51]

See also

References

- ↑ Peters, Ed, ed. (February 2009). "Balancing Betas: Essential Risk Diversification" (pdf). First Quadrant Perspective 6 (2).

- ↑ 2.0 2.1 2.2 2.3 Martin Steward (October 2010). The Truly Balance Portfolio. Investments and Pensions Europe

- ↑ 3.0 3.1 "Risk Parity: Nice Idea, Awkward Reality". I&PE. April 2, 2011. Retrieved June 2011.

- ↑ 4.0 4.1 Mathew Roberts (April 2011). Missed Opportunity?. I&PE

- ↑ 5.0 5.1 Anderson, Robert M.; Bianchi, Stephen W.; Goldberg, Lisa R. (November–December 2012). "Will My Risk Parity Strategy Outperform?". Financial Analysts Journal 68 (6): 75–93. doi:10.2469/faj.v68.n6.7.

- ↑ 6.0 6.1 Choueifaty, Y.; Coignard, Y. (2008). "Towards maximum diversification". Journal of Portfolio Management 34 (4): 40–51. doi:10.3905/JPM.2008.35.1.40.

- ↑ 7.0 7.1 Martellini, L. (2008). "Toward the design of better equity benchmarks". Journal of Portfolio Management 34 (4): 1–8. doi:10.3905/jpm.2008.709978.

- ↑ Amanda White (March 9, 2010). "Risk Parity Becomes Bittersweet Flavour". Top 1000 Funds. Retrieved October 18, 2011.

- ↑ Maillard, Sebastien; Roncalli, Thierry; Teiletche, Jerome (September 2008). "On the properties of equally-weighted risk contributions portfolios". Working Paper. doi:10.2139/ssrn.1271972. Retrieved October 18, 2011.

- ↑ Peters, ed. (December 2008). "Does Your Portfolio Have "Bad Breath?": Choosing Essential Betas". First Quadrant Perspective 5 (4).

- ↑ Allen, Gregory C. (February 2010). "The Risk Parity Approach to Asset Allocation" (pdf). Callan Investments Institute Research. Retrieved October 18, 2011.

- ↑ 12.0 12.1 12.2 12.3 Justin Mundt (October 2010). Defining Risk Parity. ai-CIO. p. 9

- ↑ Gregory D. Houser (November 2010). "Risk Parity; The Truly Balance Portfolio?". Fund Evaluation Group. Retrieved June 2011.

- ↑ 14.0 14.1 Levell, Christopher A. (March 2010). "Risk Parity: In the Spotlight After 50 Years" (pdf). NEPC. Retrieved October 18, 2011.

- ↑ Goldwhite, Paul (October 2008). "Diversification and Risk Management: What Volatility Tells Us" (pdf). First Quadrant Perspective 5 (3).

- ↑ Gregory C. Callan (February 2010). "The Risk Parity Approach to Asset Allocation" (pdf). Callan Investments Institute Research. p. 2. Retrieved June 2011.

- ↑ 17.0 17.1 17.2 Schwartz, Stephanie (April 2011). "Risk Parity: Taking the Long View". I&PE. Retrieved June 2011.

- ↑ John Plender (January 30, 2011). "Following the herd risks capital loss". Financial Times. Retrieved June 2011.

- ↑ The Institutional Investor, The Last Frontier, Francis Denmark, Sept 2010, page 7

- ↑ AllianceBernstein plans risk parity strategy. Global Pensions. Oct 2, 2010.

- ↑ Unknown author (Oct 5, 2010). "AQR Launches Risk Parity Mutual Fund". FIN Alternatives. Retrieved Feb 7, 2013.

- ↑ The Clifton Group Names New Manager of Risk Parity Strategies. Money Management Letter. March 1, 2011.

- ↑ McCann, Bailey. "Salient Partners launches Salient Risk Parity Inde". Aug 21, 2012. Opalesque. Retrieved Feb 7, 2013.

- ↑ "Salient Risk Parity Index". Salient Partners LP.

- ↑ "Salient Partners Debuts Industry-First Risk Parity Index". MarketWatch.

- ↑ Henrik Gade Jepsen (April 2011). "Case Study:ATP". Investments and Pensions Europe.

- ↑ Dori, F.; Häusler, F.; Stefanovits, D. (2011). "(R)Evolution of Asset Allocation" (pdf). White Paper.

- ↑ Allen, Gregory C. (February 2010). "President and Director of Research". Callan Investment Institute Research.

- ↑ Laise, Eleanor (Oct 2, 2010). "How Risky Are Those Low-Risk Funds?". Wall Street Journal. Retrieved Feb 7, 2013.

- ↑ 30.0 30.1 Corkery, Michael (June 27, 2013). "Fashionable 'Risk Parity' Funds Hit Hard". Wall Street Journal. Retrieved July 31, 2013.

- ↑ Clarke, R.; de Silva, H.; Thorley, S. (2002). "Portfolio constraints and the fundamental law of active management" (pdf). Financial Analysts Journal 58 (5): 48–66. doi:10.2469/faj.v58.n5.2468.

- ↑ PSERS Revamp Cash Management. Money Management Letter. Oct 18, 2010. p. 4

- ↑ Barry B. Burr (Jan 18, 2011). Wisconsin Picks Pair For $600 Million In Risk Parity. Pensions and Investments

- ↑ Francis Denmark (September 2010). The Last Frontier. The Institutional Investor

- ↑ 35.0 35.1 Qian, E. (September 2005). Risk parity portfolios: Efficient portfolios through true diversification (pdf). Panagora Asset Management

- ↑ 36.0 36.1 Qian, E. (2006). "On the Financial interpretation of risk contributions: Risk budgets do add up". Journal of Investment Management (Fourth Quarter).

- ↑ Lindberg, C. (2009). "Portfolio optimization when expected stock returns are determined by exposure to risk" (pdf). Bernoulli 15 (2): 464–474. arXiv:0906.2271. Bibcode:2009arXiv0906.2271L. doi:10.3150/08-BEJ163. Retrieved October 18, 2011. Unknown parameter

|class=ignored (help) - ↑ Neurich, Q. (April 2008). Alternative indexing with the MSCI World Index

- ↑ AllianceBernstein plans risk parity strategy. Global Pensions. October 2, 2010

- ↑ Anderson, Robert M.; Bianchi, Stephen W.; Goldberg, Lisa R. (July 2013). "The Decision to Lever". Working Paper # 2013-01, Center for Risk Management Research, University of California, Berkeley.

- ↑ Orr, Leanna (26 July 2013). "Is Levering a Portfolio Ever Worth It?". Asset International's Chief Investment Officer.

- ↑ Asness, Clifford S. (Winter 1996). "Why not 100% Equities". Journal of Portfolio Management 22 (2): 29. doi:10.3905/jpm.1996.29.

- ↑ 43.0 43.1 43.2 "Risk Parity, Or Simply Risky?|ai5000". May–June 2010. p. 27.

- ↑ Inker, Ben (March 2010). The Hidden Risk of Risk Parity Portfolios. GMO White Paper

- ↑ Foresti, Steven J.; Rush, Michael E. (February 11, 2010). Risk Focused Diversification: Utilizing Leverage within Asset Allocation. Wilshire Consulting

- ↑ Tütüncü, R.H; Koenig, M. (2004). "Robust asset allocation". Annals of Operations Research 132: 132–157. doi:10.1023/B:ANOR.0000045281.41041.ed.

- ↑ 47.0 47.1 McCrum, Dan (September 20, 2012). "Investors rush for ‘risk parity’ shield". Retrieved January 14, 2013.

- ↑ Appell, Douglas (November 30, 2009). Bridgewater under the Weather; 'Depression mode' decision good news for competitors. Pensions & Investments. p. 1

- ↑ aiCIO. "Risk Parity Investment Survey". aiCIO. Retrieved 12 September 2011.

- ↑ Barry B. Burr (January 18, 2011). "Wisconsin Picks Pair for $600 Million In Risk Parity". Pensions & Investments.

- ↑ "Views from the top: What’s hot and what’s not". March 8, 2013. Retrieved March 8, 2013.

| ||||||||||||||||||||||||||||