Risk-neutral measure

In mathematical finance, a risk-neutral measure, also called an equivalent martingale measure, is heavily used in the pricing of financial derivatives due to the fundamental theorem of asset pricing, which implies that in a complete market a derivative's price is the discounted expected value of the future payoff under the unique risk-neutral measure.[1]

Motivating the use of risk-neutral measures

Prices of assets depend crucially on their risk as investors typically demand more profit for bearing more uncertainty. Therefore, today's price of a claim on a risky amount realised tomorrow will generally differ from its expected value. Most commonly, investors are risk-averse and today's price is below the expectation, remunerating those who bear the risk. (At least in large financial markets. Example of risk-seeking markets are casinos and lotteries.)

To price assets, consequently, the calculated expected values need to be adjusted for an investor's risk preferences (see also Sharpe ratio). Unfortunately, the discounted rates would vary between investors and an individual's risk preference is difficult to quantify.

It turns out that in a complete market with no arbitrage opportunities there is an alternative way to do this calculation: Instead of first taking the expectation and then adjusting for an investor's risk preference, one can adjust, once and for all, the probabilities of future outcomes such that they incorporate all investors' risk premia, and then take the expectation under this new probability distribution, the risk-neutral measure. The main benefit stems from the fact that once the risk-neutral probabilities are found, every asset can be priced by simply taking its expected payoff. Note that if we used the actual real-world probabilities, every security would require a different adjustment (as they differ in riskiness).

The lack of arbitrage is crucial for existence of a risk-neutral measure. In fact, by the fundamental theorem of asset pricing, the condition of no-arbitrage is equivalent to the existence of a risk-neutral measure. Completeness of the market is also important because in an incomplete market there are a multitude of possible prices for an asset corresponding to different risk-neutral measures. It is usual to argue that market efficiency implies that there is only one price (the "law of one price"); the correct risk-neutral measure to price with must be selected using economic, rather than purely mathematical, arguments.

A common mistake is to confuse the constructed probability distribution with the real-world probability. They will be different because in the real-world, investors demand risk premia, whereas it can be shown that under the risk-neutral probabilities all assets have the same expected rate of return, the risk-free rate (or short rate) and thus do not incorporate any such premia. The method of risk-neutral pricing should be considered as many other useful computational tools -- convenient and powerful, even if seemingly artificial.

The origin of the risk-neutral measure (Arrow securities)

It is natural to ask how a risk-neutral measure arises in a market free of arbitrage. Somehow the prices of all assets will determine a probability measure. One explanation is given by utilizing the Arrow security. For simplicity, consider a discrete world with only one future time horizon. In other words, there is the present (time 0) and the future (time 1), and at time 1 the state of the world can be one of finitely many states. An Arrow security corresponding to state n, An, is one which pays $1 at time 1 in state n and $0 in any of the other states of the world.

What is the price of An now? It must be positive as there is a chance you will gain $1; it should be less than $1 as that is the maximum possible payoff. Thus the price of each An, which we denote by An(0), is strictly between 0 and 1.

Actually, the sum of all the security prices must be equal to the present value of $1, because holding a portfolio consisting of each Arrow security will result in certain payoff of $1. Consider a raffle where a single ticket wins a prize of all entry fees: if the prize is $1, the entry fee will be 1/number of tickets. For simplicity, we will consider the interest rate to be 0, so that the present value of $1 is $1.

Thus the An(0) 's satisfy the axioms for a probability distribution. Each is non-negative and their sum is 1. This is the risk-neutral measure! Now it remains to show that it works as advertised, i.e. taking expected values with respect to this probability measure will give the right price at time 0.

Suppose you have a security C whose price at time 0 is C(0). In the future, in a state i, its payoff will be Ci. Consider a portfolio P consisting of Ci amount of each Arrow security Ai. In the future, whatever state i occurs, then Ai pays $1 while the other Arrow securities pay $0, so P will pay Ci. In other words, the portfolio P replicates the payoff of C regardless of what happens in the future. The lack of arbitrage opportunities implies that the price of P and C must be the same now, as any difference in price means we can, without any risk, (short) sell the more expensive, buy the cheaper, and pocket the difference. In the future we will need to return the short-sold asset but we can fund that exactly by selling our bought asset, leaving us with our initial profit.

But regarding each Arrow security price as a probability, we see that the portfolio price P(0) is the expected value of C under the risk-neutral probabilities. If the interest rate were positive, we would need to discount the expected value appropriately to get the price.

Note that Arrow securities do not actually need to be traded in the market. This is where market completeness comes in. In a complete market, every Arrow security can be replicated using a portfolio of real, traded assets. The argument above still works considering each Arrow security as a portfolio.

In a more realistic model, such as the Black-Scholes model and its generalizations, our Arrow security would be something like a double digital option, which pays off $1 when the underlying asset lies between a lower and an upper bound, and $0 otherwise. The price of such an option then reflects the market's view of the likelihood of the spot price ending up in that price interval, adjusted by risk premia, entirely analogous to how we obtained the probabilities above for the one-step discrete world.

Usage

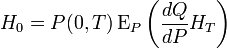

Risk-neutral measures make it easy to express the value of a derivative in a formula. Suppose at a future time  a derivative (e.g., a call option on a stock) pays

a derivative (e.g., a call option on a stock) pays  units, where is a random variable on the probability space describing the market. Further suppose that the discount factor from now (time zero) until time is

units, where is a random variable on the probability space describing the market. Further suppose that the discount factor from now (time zero) until time is  . Then today's fair value of the derivative is

. Then today's fair value of the derivative is

where the risk-neutral measure is denoted by  . This can be re-stated in terms of the physical measure P as

. This can be re-stated in terms of the physical measure P as

where  is the Radon–Nikodym derivative of with respect to

is the Radon–Nikodym derivative of with respect to  .[2]

.[2]

Another name for the risk-neutral measure is the equivalent martingale measure. If in a financial market there is just one risk-neutral measure, then there is a unique arbitrage-free price for each asset in the market. This is the fundamental theorem of arbitrage-free pricing. If there are more such measures, then in an interval of prices no arbitrage is possible. If no equivalent martingale measure exists, arbitrage opportunities do.

In markets with transaction costs, with no numéraire, the consistent pricing process takes the place of the equivalent martingale measure. There is in fact a 1-to-1 relation between a consistent pricing process and an equivalent martingale measure.

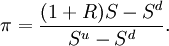

Example 1 — Binomial model of stock prices

Given a probability space  , consider a single-period binomial model. A probability measure

, consider a single-period binomial model. A probability measure  is called risk neutral if for all

is called risk neutral if for all

.

Suppose we have a two-state economy: the initial stock price

.

Suppose we have a two-state economy: the initial stock price  can go either up to

can go either up to  or down to

or down to  . If the interest rate is

. If the interest rate is  , and

, and  (else there is arbitrage in the market), then the risk-neutral probability of an upward stock movement is given by the number

(else there is arbitrage in the market), then the risk-neutral probability of an upward stock movement is given by the number

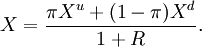

Given a derivative with payoff  when the stock price moves up and

when the stock price moves up and  when it goes down, we can price the derivative via

when it goes down, we can price the derivative via

Example 2 — Brownian motion model of stock prices

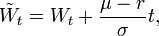

Suppose our economy consists of 2 assets, a stock and a risk-free bond, and that we use the Black-Scholes model. In the model the evolution of the stock price can be described by Geometric Brownian Motion:

where  is a standard Brownian motion with respect to the physical measure. If we define

is a standard Brownian motion with respect to the physical measure. If we define

Girsanov's theorem states that there exists a measure under which  is a Brownian motion.

is a Brownian motion.

is known as the market price of risk.

Differentiating and rearranging yields:

is known as the market price of risk.

Differentiating and rearranging yields:

Put this back in the original equation:

Let  be the discounted stock price given by

be the discounted stock price given by  , then by Ito's lemma we get the SDE:

, then by Ito's lemma we get the SDE:

is the unique risk-neutral measure for the model.

The discounted payoff process of a derivative on the stock  is a martingale under . Notice the drift of the SDE is r, the risk-free interest rate, implying risk neutrality. Since

is a martingale under . Notice the drift of the SDE is r, the risk-free interest rate, implying risk neutrality. Since  and

and  are -martingales we can invoke the martingale representation theorem to find a replicating strategy - a portfolio of stocks and bonds that pays off

are -martingales we can invoke the martingale representation theorem to find a replicating strategy - a portfolio of stocks and bonds that pays off  at all times

at all times  .

.

Notes

- ↑ Glyn A. Holton (2005). "Fundamental Theorem of Asset Pricing". riskglossary.com. Retrieved October 20, 2011.

- ↑ Hans Föllmer; Alexander Schied (2004). Stochastic Finance: An Introduction in Discrete Time (2 ed.). Walter de Gruyter. p. 6. ISBN 978-3-11-018346-7.

- ↑ Elliott, Robert James; Kopp, P. E. (2005). Mathematics of financial markets (2 ed.). Springer. pp. 48–50. ISBN 978-0-387-21292-0.

See also

- Mathematical finance

- Martingale pricing

- Forward measure

- Fundamental theorem of arbitrage-free pricing

- Law of one price

- Rational pricing

- Brownian model of financial markets

- Martingale (probability theory)

External links

- Gisiger, Nicolas: Risk-Neutral Probabilities Explained

- Tham, Joseph: Risk-neutral Valuation: A Gentle Introduction, Part II