Excess reserves

In banking, excess reserves are bank reserves in excess of a reserve requirement set by a central bank. They are reserves of cash more than the required amounts.[1]

In the United States, bank reserves are held as FRB (Federal Reserve Bank) credit in FRB accounts; they are not separated into separate "minimum reserves" and "excess reserves" accounts. The total amount of FRB credit held in all FRB accounts, together with all currency and vault cash form the M0 monetary base. Holding excess reserves has an opportunity cost if higher risk-adjusted interest can be earned by putting the funds elsewhere. For banks in the U.S. Federal Reserve System, this is accomplished by making short-term (usually overnight) loans on the federal funds market to banks who may be short of their reserve requirements. However, some banks may choose to hold their excess reserves in order to facilitate upcoming transactions or meet contractual clearing balance requirements.[2]

Interest on excess reserves

In the United States (2008-)

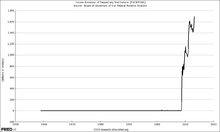

On October 3, 2008, Section 128 of the Emergency Economic Stabilization Act of 2008 allowed the Fed to begin paying interest on excess reserve balances ("IOER") as well as required reserves. They began doing so three days later.[3] Banks had already begun increasing the amount of their money on deposit with the Fed at the beginning of September, up from about $10 billion total at the end of August, 2008, to $880 billion by the end of the second week of January, 2009.[4][5] In comparison, the increase in reserve balances reached only $65 billion after September 11, 2001 before falling back to normal levels within a month. Former U.S. Treasury Secretary Henry Paulson's original bailout proposal under which the government would acquire up to $700 billion worth of mortgage-backed securities contained no provision to begin paying interest on reserve balances.[6]

The day before the change was announced, on October 7, Fed Chairman Ben Bernanke expressed some confusion about it, saying, "We're not quite sure what we have to pay in order to get the market rate, which includes some credit risk, up to the target. We're going to experiment with this and try to find what the right spread is."[7] The Fed adjusted the rate on October 22, after the initial rate they set October 6 failed to keep the benchmark U.S. overnight interest rate close to their policy target,[7][8] and again on November 5 for the same reason.[9]

The Congressional Budget Office estimated that payment of interest on reserve balances would cost the American taxpayers about one tenth of the present 0.25% interest rate on $800 billion in deposits:

| Year | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Millions of dollars | 0 | -192 | -192 | -202 | -212 | -221 | -242 | -253 | -266 | -293 | -308 |

| (Negative numbers represent expenditures; losses in revenue not included.) | |||||||||||

0.25% simple interest on $800 billion is $2 billion, not $202 million as shown for 2009. But those expenditures pale in comparison to the lost tax revenues worldwide resulting from decreased economic activity from damage to the short-term commercial paper and associated credit markets.

Beginning December 18, the Fed directly established interest rates paid on required reserve balances and excess balances instead of specifying them with a formula based on the target federal funds rate.[11][12][13] On January 13, Ben Bernanke said, "In principle, the interest rate the Fed pays on bank reserves should set a floor on the overnight interest rate, as banks should be unwilling to lend reserves at a rate lower than they can receive from the Fed. In practice, the federal funds rate has fallen somewhat below the interest rate on reserves in recent months, reflecting the very high volume of excess reserves, the inexperience of banks with the new regime, and other factors. However, as excess reserves decline, financial conditions normalize, and banks adapt to the new regime, we expect the interest rate paid on reserves to become an effective instrument for controlling the federal funds rate."[14]

Also on January 13, Financial Week said Mr. Bernanke admitted that a huge increase in banks' excess reserves is stifling the Fed's monetary policy moves and its efforts to revive private sector lending.[15] On January 7, 2009, the Federal Open Market Committee had decided that, "the size of the balance sheet and level of excess reserves would need to be reduced."[16] On January 15, Chicago Fed president and Federal Open Market Committee member Charles Evans said, "once the economy recovers and financial conditions stabilize, the Fed will return to its traditional focus on the federal funds rate. It also will have to scale back the use of emergency lending programs and reduce the size of the balance sheet and level of excess reserves. Some of this scaling back will occur naturally as market conditions improve on account of how these programs have been designed. Still, financial market participants need to be prepared for the eventual dismantling of the facilities that have been put in place during the financial turmoil" [17]

At the end of January, 2009, excess reserve balances at the Fed stood at $793 billion[18] but less than two weeks later on February 11, total reserve balances had fallen to $603 billion. On April 1, reserve balances had again increased to $806 billion. By August 2011, they had reached $1.6 trillion.[19]

On March 20, 2013, excess reserves stood at $1.76 trillion.[19] As the economy began to show signs of recovery in 2013, the Fed began to worry about the public relations problem that paying dozens of billions of dollars in interest on excess reserves (IOER) would cause when interest rates rise. St. Louis Fed president James B. Bullard said, "paying them something of the order of $50 billion [is] more than the entire profits of the largest banks." Bankers quoted in the Financial Times said the Fed could increase IOER rates more slowly than benchmark Fed funds rates, and reserves should be shifted out of the Fed and lent out by banks as the economy improves. Foreign banks have also steeply increased their excess reserves at the Fed which the Financial Times said could aggravate the Fed’s PR problem.[20]

By October 2013 the excess reserves at the Federal Reserve had exceeded $2.3 trillion.[19]

Related measures

In Sweden (2009-)

The Riksbank started to charge 0.25% interest on overnight deposits (reserves) on 2 July 2009. It had previous paid positive interest rates on all overnight deposits.

In the United Kingdom (2009-)

The Bank of England started to pay interest of 0.5% on reserves on 5 March 2009.[21] Technically these are not excess reserves, because the United Kingdom does not have reserve requirements.

Impact on inflation of excess reserve balances

Research by the Fed claims that counterintuitively, it is interest paid on reserves that helps to guard against inflationary pressures.[2] Under a traditional operating framework, in which central bank controls interest rates by changing the level of reserves and pays no interest on excess reserves, it would need to remove almost all of these excess reverves to raise market interest rates. Now when central bank pays interest on excess reserves the link between the level of reserves and willingness of commercial banks to lend is broken.[2] It allows the central bank to raise market interest rates by simply raising the interest rate it pays on reserves without changing the quantity of reserves thus reducing lending growth and curbing economic activity.[2]

See also

References

- ↑ American Heritage Dictionary of Business Terms, 2009

- ↑ 2.0 2.1 2.2 2.3 Todd Keister and James J. McAndrews (December 2009). "Why Are Banks Holding So Many Excess Reserves?". New York Fed. Retrieved September 9, 2012.

- ↑ Federal Reserve Board of Governors (October 6, 2008) "Board announces that it will begin to pay interest on depository institutions required and excess reserve balance" FRB press release

- ↑ Crescenzi, T. (December 22, 2008) "Crescenzi: Banks Sitting on $1 Trillion Cash" CNBC

- ↑ Krell, E. (December 10, 2008) "What Is Wrong With TARP?" Business Finance

- ↑ "Text of Draft Proposal for Bailout Plan". New York Times. September 20, 2008.

- ↑ 7.0 7.1 Lanman, S. (October 22, 2008) "Fed Raises Rate It Pays on Banks' Reserve Balances (Update2)" Bloomberg

- ↑ Federal Reserve Board of Governors (October 22, 2008) "Federal Reserve announces it will alter the formula used to determine the interest rate paid to depository institutions on excess balances" FRB Press Release

- ↑ Federal Reserve Board of Governors (November 5, 2008) "Board announces it will alter formulas used to determine interest rates paid to depository institutions on required reserve balances and excess reserve balances" FRB Press Release

- ↑ Congressional Budget Office (May 18, 2006) "CBO Cost Estimate, Financial Services Regulatory Relief Act of 2006," Table 1

- ↑ Federal Reserve Board of Governors (December 16, 2008) "Federal Reserve issues technical note concerning the calculation of interest rates on required reserve balances and excess balances for the maintenance periods ending December 17, 2008-December 16, 2008" FRB Press Release

- ↑ Federal Reserve Board of Governors (December 31, 2008) "Interest on Required Reserve Balances and Excess Balances" accessed January 5, 2008

- ↑ Wilder, R. (January 7, 2009) "FOMC minutes show the Fed is trying to think outside the box" News N Economics (excerpts of the December 15–16, 2008 Federal Open Market Committee meeting minutes)

- ↑ Bernanke, B. (January 13, 2009) "The Crisis and the Policy Response" (London School of Economics)

- ↑ Quinn, M. (January 13, 2009) "Bernanke admits Fed struggling to revive private lending" FinancialWeek.com

- ↑ Irwin, N. (January 7, 2009) "Fed Expects Weak Economy, Fears 'Prolonged Retraction'" Washington Post

- ↑ Cooke, K. (January 15, 2008) "Fed's Evans: U.S. in midst of serious recession" Reuters

- ↑ Moyer, L. (February 3, 2009) "Banks Promise Loans but Hoard Cash" Forbes

- ↑ 19.0 19.1 19.2 Federal Reserve Bank of St. Louis (March 20, 2013) "Series: WRESBAL, Reserve Balances with Federal Reserve Banks" FRED Economic Data System

- ↑ Robin Harding; Tom Braithwaite (February 18, 2013). "Fears at Fed of rate payouts to banks". Financial Times. Retrieved 20 March 2013.

- ↑ Claire Jones (12 August 2009), "Bank will consider cutting interest on reserves", CentralBanking.com, retrieved 20 January 2013