Volume-weighted average price

In finance, volume-weighted average price (VWAP) is the ratio of the value traded to total volume traded over a particular time horizon (usually one day). It is a measure of the average price a stock traded at over the trading horizon.

VWAP is often used as a trading benchmark by investors who aim to be as passive as possible in their execution. Many pension funds, and some mutual funds, fall into this category. The aim of using a VWAP trading target is to ensure that the trader executing the order does so in-line with volume on the market. It is sometimes argued that such execution reduces transaction costs by minimizing market impact (the adverse effect of a trader's activities on the price of a security).

VWAP can be measured between any two points in time but is displayed as the one corresponding to elapsed time during the trading day by information provider.

VWAP is often used in algorithmic trading. Indeed, a broker may guarantee execution of an order at the VWAP price and have a computer program enter the orders into the market in order to earn the trader's commission and create P&L. This is called a guaranteed VWAP execution. The broker can also trade in a best effort way and answer to the client the realized price. This is called a VWAP target execution; it incurs more dispersion in the answered price compared to the VWAP price for the client but a lower received/paid commission. Trading algorithms that use VWAP as a target belong to a class of algorithms known as volume participation algorithms.

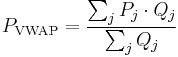

Formula

VWAP is calculated using the following formula:

where:

= Volume Weighted Average Price

= Volume Weighted Average Price = price of trade j

= price of trade j = quantity of trade j

= quantity of trade j = each individual trade that takes place over the defined period of time, excluding cross trades and basket cross trades.

= each individual trade that takes place over the defined period of time, excluding cross trades and basket cross trades.