L-moment

In statistics, L-moments[1][2][3] are statistics used to summarize the shape of a probability distribution. They are analogous to conventional moments in that they can be used to calculate quantities analogous to standard deviation, skewness and kurtosis, termed the L-scale, L-skewness and L-kurtosis respectively (the L-mean is identical to the conventional mean). Standardised L-moments are called L-moment ratios and these are analogous to standardized moments.

L-moments differ from conventional moments in that they are calculated using linear combinations of the ordered data; the "l" in "linear" is what leads to the name being "L-moments". Just as for conventional moments, a theoretical distribution has a set of population L-moments. Estimates of the population L-moments (sample L-moments) can be defined for a sample from the population.

Contents |

Population L-moments

For a random variable X, the rth population L-moment is[1]

where Xk:n denotes the kth order statistic (kth smallest value) in an independent sample of size n from the distribution of X and  denotes expected value. In particular, the first four population L-moments are

denotes expected value. In particular, the first four population L-moments are

The first two of these L-moments have conventional names:

The L-scale is equal to half the mean difference.[4]

Sample L-moments

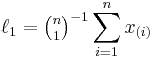

Direct estimators for the first four L-moments in a finite sample of n observations are[5]:

where x(i) is the ith order statistic and  is a binomial coefficient. Sample L-moments can also be defined indirectly in terms of probability weighted moments,[1] which leads to a more efficient algorithm for their computation.[5]

is a binomial coefficient. Sample L-moments can also be defined indirectly in terms of probability weighted moments,[1] which leads to a more efficient algorithm for their computation.[5]

L-moment ratios

A set of L-moment ratios, or scaled L-moments, is defined by

The most useful of these are  , called the L-skewness, and

, called the L-skewness, and  , the L-kurtosis.

, the L-kurtosis.

L-moment ratios lie within the interval (–1, 1). Tighter bounds can be found for some specific L-moment ratios; in particular, the L-kurtosis lies in [-¼,1), and

A quantity analogous to the coefficient of variation, but based on L-moments, can also be defined:  which is called the "coefficient of L-variation", or "L-CV". For a non-negative random variable, this lies in the interval (0,1)[1] and is identical to the Gini coefficient.

which is called the "coefficient of L-variation", or "L-CV". For a non-negative random variable, this lies in the interval (0,1)[1] and is identical to the Gini coefficient.

Usage

There are two common ways that L-moments are used:

- As summary statistics for data.

- To derive estimates for the parameters of probability distributions.

In statistics the latter is most commonly done using maximum likelihood methods or using the method of moments, however using L-moments provides an alternative method of parameter estimation. The former can also be performed using conventional moments, however using L-moments provides many advantages. As an example consider a dataset with a few data points and one outlying data value. If the ordinary standard deviation of this data set is taken it will be highly influenced by this one point: however, if the L-scale is taken it will be far less sensitive to this data value. Consequently L-moments are far more meaningful when dealing with outliers in data than conventional moments. One example of this is using L-moments as summary statistics in extreme value theory (EVT).

Another advantage L-moments have over conventional moments is that their existence only requires the random variable to have finite mean, so the L-moments exist even if the higher conventional moments do not exist (for example, for Student's t distribution with low degrees of freedom). A finite variance is required in addition in order for the standard errors of estimates of the L-moments to be finite.[1]

Some appearances of L-moments in the statistical literature include the book by David & Nagaraja (2003, Section 9.9)[6] and a number of papers.[7][8][9][10][11] A number of favourable comparisons of L-moments with ordinary moments have been reported.[12][13]

Values for some common distributions

The table below gives expressions for the first two L-moments and numerical values of the first two L-moment ratios of some common continuous probability distributions with constant L-moment ratios.[1][4] More complex expressions have been derived for some further distributions for which the L-moment ratios vary with one or more of the distributional parameters, including the log-normal, Gamma, generalized Pareto, generalized extreme value, and generalized logistic distributions.[1]

| Distribution | Parameters | mean, λ1 | L-scale, λ2 | L-skewness, τ3 | L-kurtosis, τ4 |

|---|---|---|---|---|---|

| Uniform | a, b | (a+b) / 2 | (b–a) / 6 | 0 | 0 |

| Logistic | μ, s | μ | s | 0 | ⅙ = 0.1667 |

| Normal | μ, σ2 | μ | σ / √π | 0 | 0.1226 |

| Laplace | μ, b | μ | 3b / 4 | 0 | 1 / (3√2) = 0.2357 |

| Student's t, 2 d.f. | ν = 2 | 0 | π/23/2 = 1.111 | 0 | ⅜ = 0.375 |

| Student's t, 4 d.f. | ν = 4 | 0 | 15π/64 = 0.7363 | 0 | 111/512 = 0.2168 |

| Exponential | λ | 1 / λ | 1 / (2λ) | ⅓ = 0.3333 | ⅙ = 0.1667 |

| Gumbel | μ, β | μ + γβ | β log 2 | 0.1699 | 0.1504 |

The notation for the parameters of each distribution is the same as that used in the linked article. In the expression for the mean of the Gumbel distribution, γ is the Euler–Mascheroni constant 0.57721… .

Extensions

Trimmed L-moments are generalizations of L-moments that give zero weight to extreme observations. They are therefore more robust to the presence of outliers, and unlike L-moments they may be well-defined for distributions for which the mean does not exist, such as the Cauchy distribution.[14]

See also

References

- ^ a b c d e f g h Hosking, J.R.M. (1990). "L-moments: analysis and estimation of distributions using linear combinations of order statistics". Journal of the Royal Statistical Society, Series B 52: 105–124. JSTOR 2345653.

- ^ Hosking, J.R.M. (1992). "Moments or L moments? An example comparing two measures of distributional shape". The American Statistician 46 (3): 186–189. JSTOR 2685210.

- ^ Hosking, J.R.M. (2006). "On the characterization of distributions by their L-moments". Journal of Statistical Planning and Inference 136: 193–198.

- ^ a b Jones, M.C. (2002). "Student's Simplest Distribution". Journal of the Royal Statistical Society. Series D (The Statistician) 51 (1): 41–49. JSTOR 3650389.

- ^ a b Wang, Q. J. (1996). "Direct Sample Estimators of L Moments". Water Resources Research 32 (12): 3617–3619. doi:10.1029/96WR02675.

- ^ David, H.A. & Nagaraja, H.N. (2003) Order Statistics, 3rd Edition. Wiley. ISBN 0-471-38926-9

- ^ Serfling, R. & Xiao, P. (2007) A contribution to multivariate L-moments: L-comoment matrices. Journal of Multivariate Analysis, 98, 1765–1781.

- ^ Delicado, P. & N. Goriab M.N. (2008) A small sample comparison of maximum likelihood, moments and L-moments methods for the asymmetric exponential power distribution. Computational Statistics & Data Analysis, 52, 1661–1673

- ^ Alkasasbeh, M.R., Raqab, M.Z. (2009) Estimation of the generalized logistic distribution parameters: comparative study. Statistical Methodology, 6(3), 262–279.

- ^ Jones, M.C. (2004) On some expressions for variance, covariance, skewness and L-moments. Journal of Statistical Planning and Inference, 126, 97–106. doi:10.1016/j.jspi.2003.09.001

- ^ Jones, M.C. (2009) Kumaraswamy's distribution: A beta-type distribution with some tractability advantages. Statistical Methodology, 6 (1), 70–81.

- ^ Royston, P. (1992). Which measures of skewness and kurtosis are best? Statistics in Medicine, 11, 333–343. doi:10.1002/sim.4780110306

- ^ Ulrych, T. J., Velis, D. R., Woodbury, A. D., Sacchi, M. D. (2000) L-moments and C-moments. Stochastic Environmental Research and Risk Assessment, 14 (1), 50–68.

- ^ Elamir, Elsayed A. H.; Seheult, Allan H. (2003). "Trimmed L-moments". Computational Statistics & Data Analysis 43 (3): 299–314. doi:10.1016/S0167-9473(02)00250-5.

External links

- The L-moments page Jonathan R.M. Hosking, IBM Research

- L Moments. Dataplot reference manual, vol. 1, auxiliary chapter. National Institute of Standards and Technology, 2006. Accessed 2010-05-25.

|

|||||||||||||

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||