Economy

| Economics |

|

|

Economies by region

|

| General categories |

|---|

|

Microeconomics · Macroeconomics |

| Methods |

|

Mathematical (Game theory · Optimization) |

| Fields and subfields |

|

Behavioral · Cultural · Evolutionary |

| Lists |

|

Journals · Publications |

|

Economic ideologies

|

|

The economy: concept and history

|

| Business and Economics Portal |

An economy consists of the economic system of a country or other area, the labor, capital and land resources, and the economic agents that socially participate in the production, exchange, distribution, and consumption of goods and services of that area. A given economy is the end result of a process that involves its technological evolution, history and social organization, as well as its geography, natural resource endowment, and ecology, as main factors. These factors give context, content, and set the conditions and parameters in which an economy functions.

Today the range of fields of study examining the economy include social sciences such as economics, sociology (economic sociology), history (economic history) and geography (economic geography). Practical fields directly related to the human activities involving production, distribution, exchange, and consumption of goods and services as a whole, range from engineering to management and business administration to applied science to finance.

All kind of professions, occupations, economic agents or economic activities, contribute to the economy. Consumption, saving and investment are core variable components in the economy and determine market equilibrium. There are three main sectors of economic activity: primary, secondary and tertiary.

Contents |

Etymology

The English words "economy" and "economics" can be traced back to the Greek words οἰκονόμος "one who manages a household" (derived from οἴκος "house", and νέμω "distribute (especially, manage)"), οἰκονομία "household management", and οἰκονομικός "of a household or family". The first recorded sense of the word "economy", found in a work possibly composed in 1440, is "the management of economic affairs", in this case, of a monastery. Economy is later recorded in more general senses including "thrift" and "administration". The most frequently used current sense, "the economic system of a country or an area", seems not to have developed until the 19th or 20th century.[1]

History

Ancient times

As long as someone has been making and distributing goods or services, there has been some sort of economy; economies grew larger as societies grew and became more complex. Sumer developed a large scale economy based on commodity money, while the Babylonians and their neighboring city states later developed the earliest system of economics as we think of, in terms of rules/laws on debt, legal contracts and law codes relating to business practices, and private property.[2]

The Babylonians and their city state neighbors developed forms of economics comparable to currently used civil society (law) concepts.[3] They developed the first known codified legal and administrative systems, complete with courts, jails, and government records.

Several centuries after the invention of cuneiform, the use of writing expanded beyond debt/payment certificates and inventory lists to be applied for the first time, about 2600 BC, to messages and mail delivery, history, legend, mathematics, astronomical records and other pursuits. Ways to divide private property, when it is contended... amounts of interest on debt... rules as to property and monetary compensation concerning property damage or physical damage to a person... fines for 'wrong doing'... and compensation in money for various infractions of formalized law were standardized for the first time in history.[2]

The ancient economy was mainly based on subsistence farming. The Shekel referred to an ancient unit of weight and currency. The first usage of the term came from Mesopotamia circa 3000 BC. and referred to a specific mass of barley which related other values in a metric such as silver, bronze, copper etc. A barley/shekel was originally both a unit of currency and a unit of weight... just as the British Pound was originally a unit denominating a one pound mass of silver.

For most people the exchange of goods occurred through social relationships. There were also traders who bartered in the marketplaces. In Ancient Greece, where the present English word 'economy' originated, many people were bond slaves of the freeholders. Economic discussion was driven by scarcity. Aristotle (384-322 B.C.) was the first to differentiate between a use value and an exchange value of goods. (Politics, Book I.) The exchange ratio he defined was not only the expression of the value of goods but of the relations between the people involved in trade. For most of the time in history economy therefore stood in opposition to institutions with fixed exchange ratios as reign, state, religion, culture, and tradition.

Middle ages

In Medieval times, what we now call economy was not far from the subsistence level. Most exchange occurred within social groups. On top of this, the great conquerors raised venture capital (from ventura, ital.; risk) to finance their captures. The capital should be refunded by the goods they would bring up in the New World. Merchants such as Jakob Fugger (1459–1525) and Giovanni di Bicci de' Medici (1360–1428) founded the first banks. The discoveries of Marco Polo (1254–1324), Christopher Columbus (1451–1506) and Vasco da Gama (1469–1524) led to a first global economy. The first enterprises were trading establishments. In 1513 the first stock exchange was founded in Antwerpen. Economy at the time meant primarily trade

Early modern times

The European captures became branches of the European states, the so-called colonies. The rising nation-states Spain, Portugal, France, Great Britain and the Netherlands tried to control the trade through custom duties and taxes in order to protect their national economy. The so-called mercantilism (from mercator, lat.: merchant) was a first approach to intermediate between private wealth and public interest. The secularization in Europe allowed states to use the immense property of the church for the development of towns. The influence of the nobles decreased. The first Secretaries of State for economy started their work. Bankers like Amschel Mayer Rothschild (1773–1855) started to finance national projects such as wars and infrastructure. Economy from then on meant national economy as a topic for the economic activities of the citizens of a state.

The industrial revolution

The first economist in the true meaning of the word was the Scotsman Adam Smith (1723–1790). He defined the elements of a national economy: products are offered at a natural price generated by the use of competition - supply and demand - and the division of labour. He maintained that the basic motive for free trade is human self interest. The so-called self interest hypothesis became the anthropological basis for economics. Thomas Malthus (1766–1834) transferred the idea of supply and demand to the problem of overpopulation. The United States of America became the place where millions of expatriates from all European countries were searching for free economic evolvement.

The Industrial Revolution was a period from the 18th to the 19th century where major changes in agriculture, manufacturing, mining, and transport had a profound effect on the socioeconomic and cultural conditions starting in the United Kingdom, then subsequently spreading throughout Europe, North America, and eventually the world. The onset of the Industrial Revolution marked a major turning point in human history; almost every aspect of daily life was eventually influenced in some way. In Europe wild capitalism started to replace the system of mercantilism (today: protectionism) and led to economic growth. The period today is called industrial revolution because the system of Production, production and division of labour enabled the mass production of goods.

Communism and its view of capitalism

Starting in England, simultaneous processes of mechanization, and the enclosures of the commons, led to increases in wealth for the controllers of capital, and mass poverty, starvation, urbanization and pauperization for much of the population . This led some, such as Karl Marx (1818–1883) and the German industrialist and philosopher Friedrich Engels, (1820–1895) to describe economy as the "system of capitalism".

Capitalism is characterized by the division of labor between worker and capitalist, in which the means of production are separated from the direct producers and are instead owned by a parasitical capitalist class. Marx and Engels believed that under capitalism, the working class produces surplus value, of which only a small percentage is returned to workers in the form of wages to provide for their bare subsistence. The rest of the surplus value is kept as profit, and is reinvested into the commodity cycle by the capitalist. The competitive forces of the market will drive capital to constantly accumulate "for the sake of more accumulation", resulting in monopolies, economic crisis and imperialism.

Marx and Engels viewed capitalism as a historically-specific mode of production, as with feudalism and hunter-gatherer societies, embedded with its own internal contradictions. Capitalism is the first mode of production in which the direct producers have no control over their conditions of labour or the means of production.

The declining living conditions of the working class would drive workers to collectively fight back as part of a class struggle, eventually overthrowing the capitalist state in a proletarian revolution and establishing a democratically planned economy, in which production is controlled by the direct producers themselves - the proletariat - in order to satisfy human needs, not accumulation of profits. Thus in the Communist Manifesto, Marx and Engels state that capitalism, in bringing to existence an urbanized working class, has created its own "gravediggers", as well as the material conditions and abundance ripe for a classless socialist society.

The first centrally planned economy was established after the Russian Revolution of 1917, led by the Bolshevik Party, in which production (and social life) was organized around workers' councils called soviets. Similar councils of democratically elected recallable worker delegates have existed in subsequent revolutions and revolutionary situations throughout the 20th Century, including the 1936 Spanish Revolution, the 1974 Carnation Revolution in Portugal, the 1979 Iranian Revolution and the 1980 Solidarity uprising in Poland.

After World War II

After the chaos of two World Wars and the devastating Great Depression, policymakers searched for new ways of controlling the course of the economy. This was explored and discussed by Friedrich August von Hayek (1899–1992) and Milton Friedman (1912–2006) who pleaded for a global free trade and are supposed to be the fathers of the so called neoliberalism. However, the prevailing view was that held by John Maynard Keynes (1883–1946), who argued for a stronger control of the markets by the state. The theory that the state can alleviate economic problems and instigate economic growth through state manipulation of aggregate demand is called Keynesianism in his honor. In the late 1950s the economic growth in America and Europe—often called Wirtschaftswunder (ger: economic miracle) —brought up a new form of economy: mass consumption economy. In 1958 John Kenneth Galbraith (1908–2006) was the first to speak of an affluent society. In most of the countries the economic system is called a social market economy.

Postmodern economy

What economist Robert Reich terms, "the not quite golden age" (WW II to the mid-1970s) gave way to the current global economy, or supercapitalism.[4] This economic revolution took place in tandem with a radical transformation of Western cultures, and the growth of oligarchical/plutocratic tendencies within the polities of Western democracies.

Discussion of such issues as the politics of the World Bank, the World Trade Organization and global players within the World Economic Forum, as well as global ecology and sustainability, have all influenced the definition of economy.

Joseph E. Stiglitz has defined economy to be a global public good. Economists like Peter Barnes and Alexander Dill are reclaiming the commons and providing definitions that embrace new phenomena like freeware. Game theorists such as Ernst Fehr and Klaus M. Schmidt are contradicting the notion of omnipresent economic self-interest. Under the gift economy extensive grassroot movements have arisen; also the credit programs of Nobel laureate Muhammed Yunus. In 2006 the World Bank started issuing its Wealth of Nations Report, tracking social and human capital.

Economic sectors

The economy includes several sectors (also called industries), that evolved in successive phases.

- The ancient economy was mainly based on subsistence farming.

- The industrial revolution lessened the role of subsistence farming, converting it to more extensive and monocultural forms of agriculture in the last three centuries. The economic growth took place mostly in mining, construction and manufacturing industries.

- In the economies of modern consumer societies there is a growing part played by services, finance, and technology—the (knowledge economy).

In modern economies, there are four main sectors of economic activity:

- Primary sector of the economy: Involves the extraction and production of raw materials, such as corn, coal, wood and iron. (A coal miner and a fisherman would be workers in the primary sector.)

- Secondary sector of the economy: Involves the transformation of raw or intermediate materials into goods e.g. manufacturing steel into cars, or textiles into clothing. (A builder and a dressmaker would be workers in the secondary sector.)

- Tertiary sector of the economy: Involves the provision of services to consumers and businesses, such as baby-sitting, cinema and banking. (A shopkeeper and an accountant would be workers in the tertiary sector.)

- Quaternary sector of the economy: Involves the research and development needed to produce products from natural resources. (A logging company might research ways to use partially burnt wood to be processed so that the undamaged portions of it can be made into pulp for paper.) Note that education is sometimes included in this sector.

Other sectors include the

- Public Sector or state sector

- Private Sector or privately-run businesses

- Social sector or Voluntary sector

Economic measures

There are a number of ways to measure economic activity of a nation. These methods of measuring economic activity include:

- Consumer spending

- Exchange Rate

- Gross domestic product

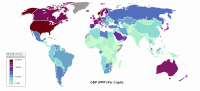

- GDP per capita

- GNP

- Stock Market

- Interest Rate

- National Debt

- Rate of Inflation

- Unemployment

- Balance of Trade

GDP

The GDP - Gross domestic product of a country is a measure of the size of its economy. The most conventional economic analysis of a country relies heavily on economic indicators like the GDP and GDP per capita. While often useful, it should be noted that GDP only includes economic activity for which money is exchanged.

Informal economy

An informal economy is economic activity that is neither taxed nor monitored by a government, contrasted with a formal economy. The informal economy is thus not included in that government's Gross National Product (GNP). Although the informal economy is often associated with developing countries, all economic systems contain an informal economy in some proportion.

Informal economic activity is a dynamic process which includes many aspects of economic and social theory including exchange, regulation, and enforcement. By its nature, it is necessarily difficult to observe, study, define, and measure. No single source readily or authoritatively defines informal economy as a unit of study.

The terms "under the table" and "off the books" typically refer to this type of economy. The term black market refers to a specific subset of the informal economy. The term "informal sector" was used in many earlier studies, and has been mostly replaced in more recent studies which use the newer term.

Micro economics are focused on an individual person in a given economic society and Macro economics is looking at an economy as a whole. (town, city, region)

The largest economies by GDP (millions of USD)

| Rank | Country | GDP (millions of USD) |

|---|---|---|

| World | 60,917,477[6] | |

| 18,387,785[6] | ||

| 1 | 14,441,425 | |

| 2 | 4,910,692 | |

| 3 | 4,327,448 | |

| 4 | 3,673,105 | |

| 5 | 2,866,951 | |

| 6 | 2,680,000 | |

| 7 | 2,313,893 | |

| 8 | 1,573,586 | |

| 9 | 1,601,964 | |

| 10 | 1,572,839 |

See also

- Ecological economics

- Economic history (includes list by country)

- Economic system

- Economics

- Economist

- History of money

- Non-market economics

- Primary sector of the economy

- Quaternary sector of the economy

- Secondary sector of the economy

- Tertiary sector of the economy

- Thermoeconomics

- world economy

Endnotes

- ↑ Dictionary.com, "economy." The American Heritage Dictionary of the English Language, Fourth Edition. Houghton Mifflin Company, 2004. 24 Oct. 2009.

- ↑ 2.0 2.1 Sheila C. Dow (2005), "Axioms and Babylonian thought: a reply", Journal of Post Keynesian Economics 27 (3), p. 385-391.

- ↑ Charles F. Horne, Ph.D. (1915). "The Code of Hammurabi : Introduction". Yale University. http://www.yale.edu/lawweb/avalon/medieval/hammint.htm. Retrieved September 14, 2007.

- ↑ Robert Reich, Supercapitalism: the Transformation of Business, Democracy and Everyday Life (New York: Alfred A. Knopf, 2007)

- ↑ International Monetary Fund, World Economic Outlook Database, October 2009: Nominal GDP list of countries. Data for the year 2008.

- ↑ 6.0 6.1 "Nominal 2008 GDP for the world and the European Union.". World economic outlook database, October 2009. International Monetary Fund. http://www.imf.org/external/pubs/ft/weo/2009/01/weodata/weorept.aspx?sy=2008&ey=2008&scsm=1&ssd=1&sort=country&ds=.&br=1&c=001%2C998&s=NGDPD&grp=1&a=1&pr.x=27&pr.y=8. Retrieved 2009-10-01.

References

- Aristotle, Politics, Book I-IIX, translated by Benjamin Jowett, Classics.mit.edu

- Barnes, Peter, Capitalism 3.0, A Guide to Reclaiming the Commons, San Francisco 2006, Whatiseconomy.com

- Dill, Alexander, Reclaiming the Hidden Assets, Towards a Global Freeware Index, Global Freeware Research Paper 01-07, 2007, Whatiseconomy.com

- Fehr Ernst, Schmidt, Klaus M., The Economics Of Fairness, Reciprocity and Altruism - experimental Evidence and new Theories, 2005, Discussion PAPER 2005-20, Munich Economics, Whatiseconomy.com

- Marx, Karl, Engels, Friedrich, 1848, The Communist Manifesto, Marxists.org

- Stiglitz, Joseph E., Global public goods and global finance: does global governance ensure that the global public interest is served? In: Advancing Public Goods, Jean-Philippe Touffut, (ed.), Paris 2006, pp. 149/164, GSB.columbia.edu

- Where is the Wealth of Nations? Measuring Capital for the 21st Century. Wealth of Nations Report 2006, Ian Johnson and Francois Bourguignon, World Bank, Washington 2006, Whatiseconomy.com

Further reading

- Friedman, Milton, Capitalism and Freedom, 1962.

- Galbraith, John Kenneth, The Affluent Society, 1958.

- Keynes, John Maynard, The General Theory of Employment, Interest and Money, 1936.

- Smith, Adam, An Inquiry into the Nature and Causes of the Wealth of Nations, 1776 .